The following points highlight the top eleven principal accounts to be maintained in cost ledger. The principal accounts are: 1. General Ledger Adjustment Account 2. Stores Ledger Control Account 3. Wages Control Account 4. Work-in-Progress Ledger Control Account 5. Finished Goods Ledger Control Account 6. Factory Overhead Control Account 7. Administration Overhead Control Account 8. Cost of Sales Account and Others.

1. General Ledger Adjustment Account:

This is also called Cost Ledger Control Account or Financial Ledger Control Account. This account maintains a link with financial account, completes the double entry and makes the cost ledger self-balancing. So the Cost Ledger Control account is debited or credited in places of Cash A/c, Bank A/c, Debtors A/c, Creditors A/c or any other account not appearing in cost accounting.

2. Stores Ledger Control Account:

This account is debited with all purchases of materials for the stores and credited with the issues of materials from the stores. The balance of this account represents the stock value of materials lying in the store.

3. Wages Control Account:

This account is debited with gross wages (paid and accrued) and is closed by transfer of direct wages to work-in-progress control account and indirect wages to factory, administration and selling and distribution overhead control accounts.

4. Work-in-Progress Ledger Control Account:

ADVERTISEMENTS:

All direct materials, direct wages, direct expenses, special purchases and factory overheads recovered are debited to this account. The value of finished goods completed in a period and transferred to Finished Goods Control Account is credited to this account. The balance of this account represents the value of unfinished jobs.

5. Finished Goods Ledger Control Account:

This account is debited with the cost of finished goods transferred from work-in-progress control account and the amount of administration overheads absorbed. This account is credited with cost of sales by transferring to cost of sales account. The balance of this account represents the value of unsold stock at the end of the period.

6. Factory Overhead Control Account:

This account is debited with indirect material cost, indirect wages and indirect expenses and is credited with the amount of overheads absorbed which is transferred to Work-in-Progress Control Account. The balance in this account represents under- or over-absorbed overheads and is transferred to Overhead Adjustment Account or Costing Profit and Loss Account.

7. Administration Overhead Control Account:

This account is debited with administration overhead cost incurred and is credited with the amount of overheads absorbed by finished goods. The balance in this account represents under or over-absorbed overheads which is transferred to Overhead Adjustment Account or Costing Profit and Loss Account.

8. Cost of Sales Account:

ADVERTISEMENTS:

This account is debited with the cost of goods sold by transfer from finished goods ledger control account and selling and distribution overheads absorbed. It is closed by transfer to Costing Profit and Loss Account.

9. Selling and Distribution Overhead Control Account:

This account is debited with selling and distribution overhead incurred and is credited with overhead absorbed by Cost of Sales. The balance in this account represents under or over-absorbed overheads which is transferred to Overhead Adjustment Account or Costing Profit and Loss Account.

10. Overhead Adjustment Account:

This account is debited with under-absorbed overheads for factory, administration and selling and distribution overheads and is credited with over-absorbed overheads. The balance in this account represents the net amount of over- or under-absorption which is transferred to Costing Profit and Loss Account.

11. Costing Profit and Loss Account:

This account is debited with the Cost of Sales, abnormal losses and under-absorbed overheads and is credited with sales value, abnormal gains, over-absorbed overheads. The balance in this account represents costing profit or loss which is transferred to General Ledger Adjustment Account.

ADVERTISEMENTS:

Long Practical Problems and Solutions:

1. From the following details show necessary accounts in the cost ledger:

2. In the cost ledger of a firm the following balances appear:

3. The following balances are extracted from the books of Reliance Manufacturing Company:

The cost journal shows that Rs 18,226 and Rs. 2,630 were allocated to work-in-progress in respect of works overhead and office overhead respectively. You are required to show the necessary ledger accounts under non-integrated system and extract a Trial Balance as on 31st December, 2010.

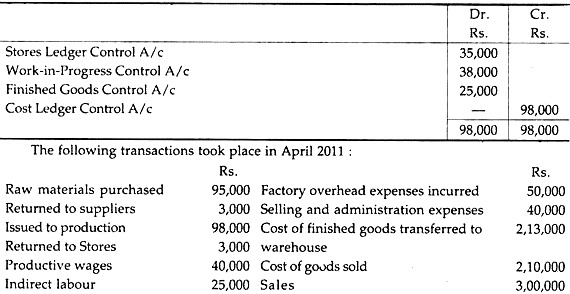

4. On 31st March 2011 the following balances were extraction from the books of the Supreme Manufacturing Company:

Factory overheads are applied to production at 150% of direct wages, any under or over-absorbed overhead being carried forward for adjustment in the subsequent months. All administrative and selling expenses are treated as period cost and charged off to the profit and Loss Account of the month in which they are incurred.

Prepare all the relevant ledger accounts in cost ledger and extract a Trial Balance as on 30th April 2011.

5. A company operates separate cost accounting and financial accounting systems. The following is the list of opening balances as on 1.04.2011 in the cost ledger:

The company’s Gross profit is 25% on Factory Cost. At the end of the quarter, WIP stocks increased by Rs. 7,500. Prepare the relevant control Accounts, Costing Profit and Loss Account and General Ledger Adjustment Account to record the above transactions for the quarter ended 30.06.2010.

Hints to Answer:

(i) Gross profit is 25% on factory cost or 20% on sales.

Hence cost of sales = Rs 2,56,000 – 20% of Rs. 2,56,000 = Rs. 2,04,800

ADVERTISEMENTS:

(ii) Cost of finished goods produced = Rs. 2,02,900

(iii) Production overhead absorbed = Rs. 1,15,900

(iv) Costing Profit Rs. 48,000

(v) Closing Balances: Stores Ledger A/C Rs. 39,175, WIP Control A/C Rs. 1,12,095

Finished Goods Control A/C Rs. 28, 880, General Ledger Adjustment A/C. Rs. 1,80,150