In this article we will discuss about the Redemption of Debentures:- 1. Introduction to Redemption of Debentures 2. Ex-interest Price and Cum-interest Price 3. Convertible Debentures 4. Sinking Fund.

Introduction to Redemption of Debentures:

Debentures are invariably redeemable. The Companies Act has not laid down any conditions for the redemption of debentures. Of course, the terms laid down for the redemption of the debentures in the prospectus at the time of issue of the debentures will have to be complied with by the company.

Debentures may be redeemed in one of the following three ways:

(i) In one lot:

ADVERTISEMENTS:

All the debentures may be redeemed in one lot at the end of a specified period of time or even before the expiry of the specified period of time by serving a notice to debenture-holders

(ii) In installments by draw of lots:

The debentures may be redeemed in installments. For example one-tenth of the total debentures may be redeemed every year for ten years by draw of lots. Lot will have to be drawn every year to determine which particular debentures have to be redeemed in that particular year.

(iii) By purchase of debentures in the open market:

ADVERTISEMENTS:

A company may reserve the right to buy its debentures in the open market. If the company cancels the debentures so purchased, it will amount to redemption of these debentures.

Cancellation of debentures may take place in one of the two ways:

(a) Immediate cancellation:

The company may cancel the debentures immediately after their purchase in the open market.

ADVERTISEMENTS:

(b) Cancellation after holding them for some time as ‘Own Debentures’:

The company may hold the debentures purchased in the open market for some time as investments in ‘Own Debentures’. It is done when the company wants to keep open its option of reselling the debentures. But after some time, it may decide to cancel the debentures held. After cancellation, the debentures stand redeemed and cannot be resold.

The company may redeem only a part of the debentures by purchase in the open market. The remaining debentures may be redeemed at the expiry of the stipulated period of time.

When a company redeems its debentures in one lot at the expiry of a specified period of time or in installments by draw of lots, the debentures may be redeemed either at par or at a premium according to the terms of issue. But if the company redeems debentures by purchase in the open market the debenture may be redeemed at a premium, at par or even at a discount.

ADVERTISEMENTS:

Debentures will be redeemed at a discount when the company is able to buy the debentures in the open market at a price lower than the face value of the debentures. Before redemption starts, there must be a balance of at least 50% of the amount of debentures issued in the Debenture Redemption Reserve.

By the terms of issue, the debentures may be redeemable at a premium and the company may, at the time of allotment of debentures, credit Premium on Redemption of Debentures Account with the amount of the premium payable at the time of debentures.

ADVERTISEMENTS:

The company may reserve the right of redeeming any of these debentures by purchase in the open market.

If the company redeems any of such debentures by purchasing them in the open market and then cancelling them, while passing entries on cancellation, Debentures Account will be debited with face value of debentures cancelled and Premium on Redemption of Debentures Account will be debited with premium agreed to be paid on redemption according to the terms of the issue.

Profit or loss on cancellation will be calculated by comparing the purchase price of debentures cancelled with this face value plus the premium payable on redemption according to the terms of the issue. Suppose, a company issues debentures of Rs 100 each redeemable at a premium of 5%. If it buys one debenture for Rs 97 and cancels it, the capital profit on cancellation is Rs 8.

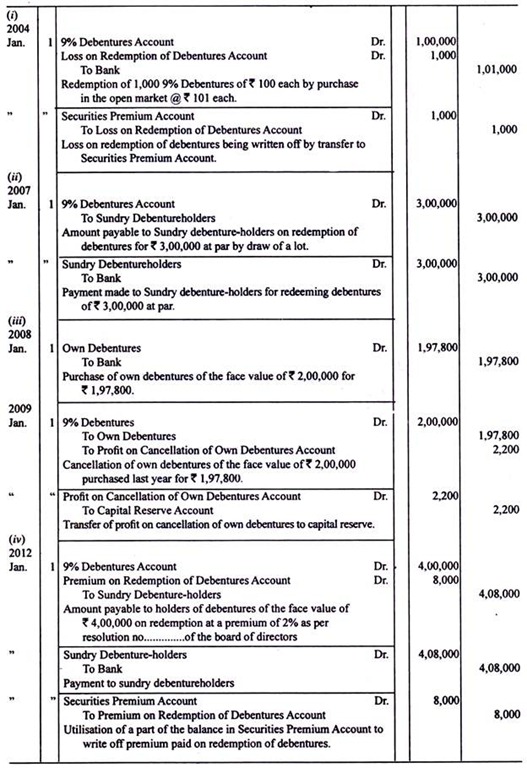

Illustration 1:

ADVERTISEMENTS:

On 1st January, 2002 New Castle Limited allotted 10,000 9% Debentures of Rs 100 each at par, the total amount having been received along with applications.

(i) On 1st January, 2004 the company purchased in the open market 1,000 of its own debentures @ Rs 101 each and cancelled them immediately.

(ii) On 1st January, 2007 the company redeemed at par debentures for Rs 3,00,000 by draw of a

(iii) On 1st January, 2008, the company purchased debentures of the face value of Rs 2,00,000 for Rs 1,97,800 in the open market, held them as investments for one year and then cancelled

ADVERTISEMENTS:

(iv) Finally as per resolution of the board of directors, the remaining debentures were redeemed at a premium of 2% on 1st January, 2012 when Securities Premium Accounting the company s ledger showed a balance of Rs. 30,000.

Pass journal entries for the abovementioned transactions ignoring debenture redemption reserve, debenture – interest and interest on own debentures.

Ex-interest Price and Cum-interest Price:

When debentures are purchased in the open market, a distinction has to be made between the capital portion and the revenue portion of the total amount paid for acquiring the debentures. The phrase ‘cum interest price’ is used to denote the total amount paid to the seller to acquire the debentures.

If the interest accrued on purchased debentures from the previous date of payment of debenture – interest to the date of the transaction is deducted from the cum-interest price, we will get ex-interest price which is the capital portion of the total amount paid, the accrued interest being the revenue portion.

Suppose on 1st April, 2011 a joint stock company allots 10,000 12% Debentures of Rs 100 each at par Interest on debentures is payable half yearly on 30th September and 31st March. On 31st May, 2012 the company buys in the open market 100 of its 12% Debentures paying a total sum of Rs 9,900 to the seller.

ADVERTISEMENTS:

Here, the total price paid per debenture is Rs 99; it is the cum-interest quotation of the debentures purchased. The previous date of payment of debenture – interest was 31st March 2012. Interest accrued on one debenture of? 100 from 31st March, 2012 to 31st May, 2012 the date of the transaction @ 12% per annum is Rs 2.

Hence, the ex-interest quotation of the debentures purchased is Rs 99 – Rs 2 = Rs 97. For 100 debentures, the ex-interest price is Rs 9,700.

Whatever may be the purpose of purchase of debentures in the open market, the accrued interest should be debited to Debentures, Interest Account. If debentures have been purchased for immediate cancellation, the ex-interest price should be compared with the face value of debentures purchased to ascertain the profit or loss on cancellation.

Illustration 2:

B Ltd. purchases for immediate cancellation 2,000 of its own 12% Debentures of Rs 100 each on 1st December, 2011, the dates of interest being 31st March and 30th September. Pass the necessary journal entries relating to the cancellation if (i) debentures are purchased at Rs 92 ex-interest. (ii) debentures are purchased at Rs 92 cum-interest.

Illustration 3:

On 31st March 2011 A Ltd.’s Balance Sheet showed 10,000 12% Debentures of Rs 100 each outstanding. Interest on debentures is payable on 30th September and 31st March every year On 1st August, 2011, the company purchased 500 of its own debentures as investment at Rs 97 ex-interest.

Pass journal entries supposing:

(i) The company cancels all its own debentures on 1st March, 2012

(ii) The company resells all its own debentures at Rs 105 cum-interest on 1st March, 2012

Illustration 4:

On 1st April, 2010, Sumitra Limited issued 25,000 12% Debentures of Rs 100 each at par. According to the terms of the issue, interest was payable half yearly on 30th September and 31st March and the company reserved the right to buy any number of debentures in the open market to be held as investments or to be cancelled at any time.

During the accounting year ended 31st March, 2011 the company purchased 200 of its debentures at Rs 102 cum- interest on 31 July, 2010 and 800 of its debentures at Rs 99 ex-interest on 28th February 2011.

On 30th June, 2011, the company sold one half of the debentures purchased on 28th February, 2011 at Rs 104 cum-interest. On 30th November, 2011, the company purchased 1,500 debentures at Rs 97.50 and on 31st December, 2011, it cancelled 600 debentures purchased in 2010-11 and still lying with it.

Pass journal entries for all the transactions relating to debentures for the accounting years 2010- 11 and 2011-2012. Also prepare important ledger accounts. Ignore creation of debenture redemption reserve.

Illustration 5:

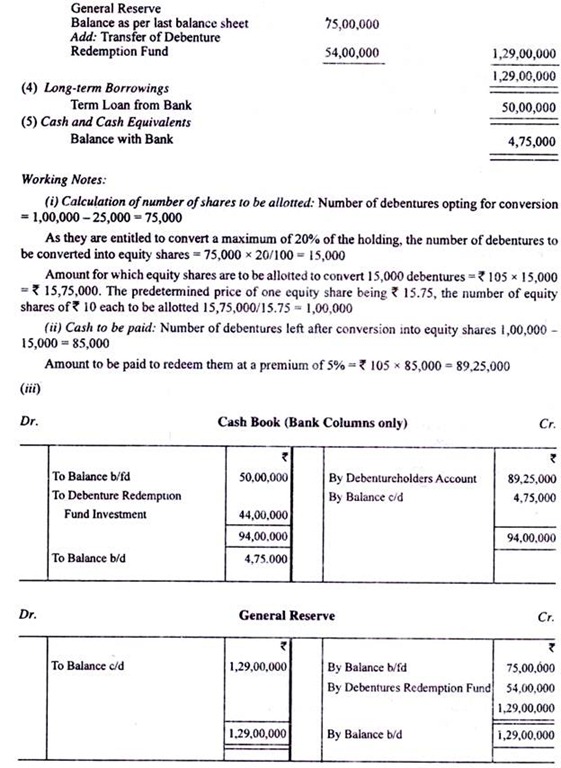

The summarised balance sheet of Convertible Limited, as on 31st March, 2012 stood as follow:

The debentures are due for redemption on 1st April, 2012. The terms of issue of debentures provided they were redeemable at a premium of 5% and also conferred option to the debenture- holders to convert 20% of their holding into equity shares at a predetermined price of Rs. 15.75 per share and receive the payment in cash for the remaining debentures.

Assuming that:-

(i) Except for 100 debenture-holders holding 25,000 debentures in all, the rest of them exercised the option for maximum conversion;

(ii) The investments realise Rs. 44 lakh on sale; and

(iii) All the transactions are put through, without any lag, on 1st April, 2012.

Redraft the balance sheet of the company as on 1st April, 2012 after giving effect to the redemption. Show your calculations in respect of the number of equity shares to be allotted and the cash payment necessary. [Adapted C.A. (Inter.) Nov. 1985]

Illustration 6:

(i) Swati Associates Ltd. has issued 10,000 12% Debentures of Rs 100 each on 1.4.2007. These debentures are redeemable at par after 3 years Interest is payable annually.

(ii) On January 1, 2009, it buys 1,500 debentures from the market at Rs 98 per debenture. These are sold away on September 30, 2009 at Rs 105 per debenture.

(iii) On April 1, 2009, it buys 1,000 debentures at Rs 104. These are cancelled on July 1, 2009.

(iv) On January 1, 2010, it buys 2,000 debentures at Rs 106. These debentures along-with other debentures are redeemed on 31st March, 2010.

Pass Journal entries and prepare the relevant ledger accounts showing the above transactions. Ignore creation of debenture redemption reserve.[C.A. (Inter) Nov. 1988, Modified]

Convertible Debentures:

Holders of convertible debentures enjoy the option of getting the debentures held by them converted into shares according to the term of the issue.

To issue convertible debentures a company requires the consent of its shareholders by special resolution and that of the Central Government so that at the time of conversion of debentures into shares, the provisions of section 81 of the Companies Act are not attracted which require that a fresh issue of shares must first be offered to the existing equity shareholders.

Debentures issued at a discount cannot be converted into fully paid shares of the same face value without undergoing the procedure for issue of shares at a discount prescribed by section 79 of the Companies Act. But it would be legal to issue shares in lieu of debentures with a paid up value equal to the amount actually received on debentures.

For example a debenture of Rs 100 issued at a discount of 10% can be converted into a share of Rs 100, Rs 90 paid up or into 9 fully paid up shares of Rs 10 each It does not involve issue of shares at a discount because in both cases the paid up value of share or shares issued in lieu of a debenture is the same as the amount actually received on a debenture.

Illustration 7:

On 1st July 2009, Ispat Limited issued 10,000 9% Mortgage Debentures of Rs 150 each at par, the interest being payable half-yearly on 1st January and 1st July.

According to the terms of the issue the debenture-holders had the option of getting the debentures converted into equity shares of Rs 100 each at a premium of Rs 50 each on 1st January, 2012. The company had the right to buy at any time its debentures in the open market for cancellation.

On 1st May 2010 the company purchased 1,000 debentures at Rs 148 cum-interest and on 1st November 2011 it purchased 1,500 debentures at Rs 146 ex-interest; the debentures being cancelled immediately in both the cases. On 1st January, 2012 holders of 4,100 debentures exercised their option getting their debentures converted into equity shares.

The company closed its books of account every year on 31st March. You are required to show journal entries for all the transactions relating to debentures during 2009-10, 2010-11 and 2011-2012. Also show the relevant portions of the ‘Liabilities’ side of the balance sheet of the company as on 31st March, 2012.

Illustration 8:

Libra Limited made a public issue in respect of which the following information is available:

(a) Number of partly convertible debentures issued 2,00,000; face value and issue price Rs 100 per debenture.

(b) Convertible portion per debenture 60%, date of conversion on expiry of 6 months from the date of allotment.

(c) Date of closure of subscription lists 1.5.2011, date of allotment 1.6.2011, rate of interest on debentures 12% payable from the date of allotment, value of equity share for the purpose of conversion Rs 60 (Face value, Rs 10).

(d) Underwriting commission @ 2% on the amount devolving on the underwriters and @ 1% on the amount subscribed for by the public.

(e) Number of debentures applied for 1,50,000.

(f) Interest payable on debentures halt-yearly on 30th September and 31st March.

Write relevant journal entries for all transactions arising out of the above during the year ended 31st March, 2012 (including cash and bank entries). [C.A. (Inter.) May, 1995 Modified]

Sinking Fund for Redemption of Debentures:

A sinking fund may be created to collect funds for redemption of debentures after their specified life. It enables the company to redeem the debentures without upsetting its working capital. With the help of Sinking Fund Tables, an amount to be set aside every year out of the profits of the company is ascertained.

The annual installment is invested in some safe securities. The interest received on investments is also invested. When debentures are to be redeemed, the investments are sold out to provide cash for redemption.

Entries in the case of a sinking fund for redemption of debentures are as follows:- At the end of the first year:

In the above mentioned scheme of entries, Debenture Redemption Fund Account, Debenture Redemption Fund Investments Account and Interest on Debenture Redemption Fund Investments Account may be named Sinking Fund Account, Sinking Fund Investments Account and Interest on Sinking Fund Investments Account respectively.

Then, the scheme may be used to collect funds to repay any liability. The scheme is similar to the Depreciation Fund which is a sinking fund to replace a wasting asset.

Special points regarding sinking fund for redemption of debentures:

The following points should be kept in mind while operating a sinking fund for redemption of debentures:

(i) If the terms of the issue of debentures lay down that the debentures will be redeemed at a premium, the amount to be collected by means of sinking fund must include the amount of the premium payable on redemption.

(ii) If investments are made in bonds, debentures or other securities available at a certain price, it may not be possible to invest exactly the same amount as is the balance of Sinking Fund because securities can be purchased only in whole numbers.

In such a case, there may be over-investment or under-investment. But such a number of securities must be purchased as to keep the balance of Sinking Fund Investments Account as near as possible to the balance of Sinking Fund.

(iii) The face value and market price of securities may differ. In such a case, it must be remembered that interest on securities will be received on the face value and not on the market value.

(iv) If debentures are redeemed in installments, as and when debentures are redeemed, the face value of debentures redeemed (plus premium payable, if any, on redemption according to the terms of the issue) should be transferred from Sinking Fund to General Reserve. When all the debentures have been redeemed, the balance of Sinking Fund should be transferred to General Reserve.

Illustration 9:

On 1st April, 2006, Old Guards Limited issued 12% Debentures for Rs 5,00,000 at par redeemable at a premium of 2% after four years on 31st March, 2010.

To collect funds for redemption, the company decided to establish a Sinking Fund; investments which were to be made to the nearest rupee were to earn interest @ 10% per annum. Sinking Fund Tables show that Rs 0.2155 invested every year for four years @ 10% per annum will accumulate Rs 1.

On 31st March, 2010 the investments were sold at a loss of 1% and the debentures were duly redeemed.

Give journal entries and ledger accounts for the four accounting years ended 31st March, 2010. Entries relating to interest on debentures and for writing off Loss on Issue of Debentures Account need not be presented. All calculations may be made to the nearest, rupee.

Illustration 10:

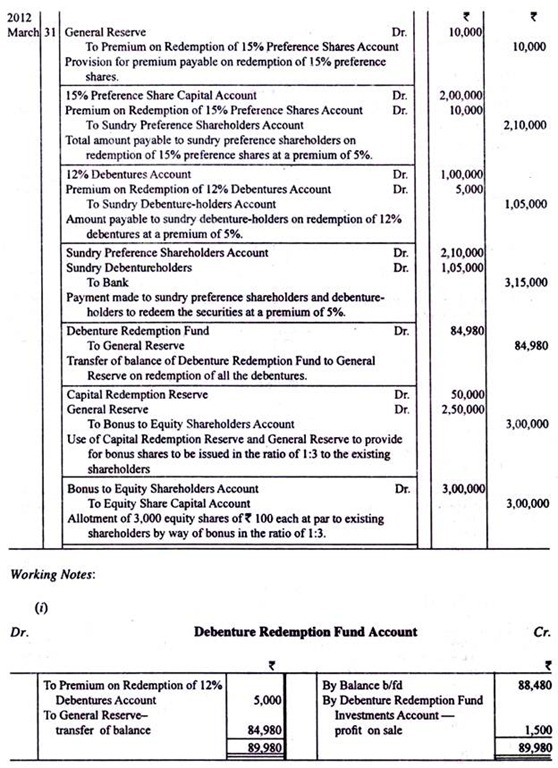

The following was the balance sheet of Brite Ltd. as on 31st March, 2012:

Illustration 11:

L.B. Ltd. had 12% Debentures of Rs 2,00,000 outstanding in its books as on 1.4.2011. It also had a balance of Rs 80,000 in Sinking Fund Account represented by 10% investments (Face value, Rs 1,00,000) On 31.12.2011 it sold investments of the face value of Rs 20,000 @ Rs 90 cum-interest and with the proceeds purchased own debentures of the face value of Rs 20,000 for immediate cancellation.

The interest dates for both debentures and investments were 30th September and 31st March. Annual appropriations to Sinking Fund came to Rs 21,000. Pass journal entries and prepare the necessary ledger accounts for the year ended 31st March, 2012. [Adapted C.W.A. (Final) June 1985].

Illustration 12:

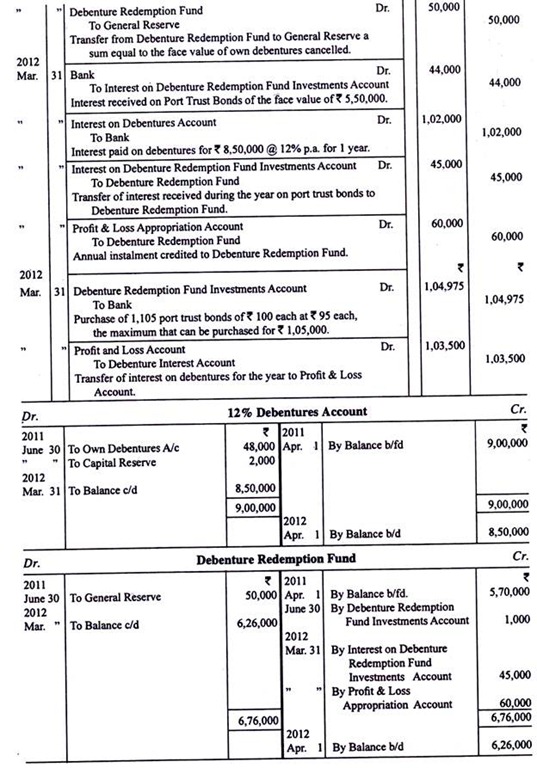

On 1st April, 2011, the books of Atul Limited showed that 9,000 12% Debentures of Rs 100 each were outstanding. On this date, the Debenture Redemption Fund showed a balance of Rs 5,70,000 represented by 8% Port Trust Bonds of the face value of Rs 6,00,000. The date of interest both for debentures and bonds was 31st March.

On 30th June, 2011, 500 Debentures were purchased in the market @ Rs 96 and cancelled immediately, the amount required being raised by selling Port Trust Bonds of the nominal value of Rs 50,000.

On 31st March, 2012, the annual installment of Rs 60,000 plus the interest received during the year on Debenture Redemption Fund Investments were invested in 8% Port Trust Bonds of Rs 100 each available at Rs 95 each to the maximum possible extent.

Give journal entries for all the above mentioned transactions. Also show important ledger accounts for the year ended 31st March, 2012.

Illustration 13:

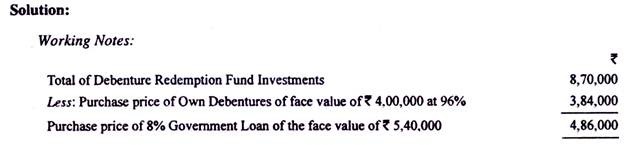

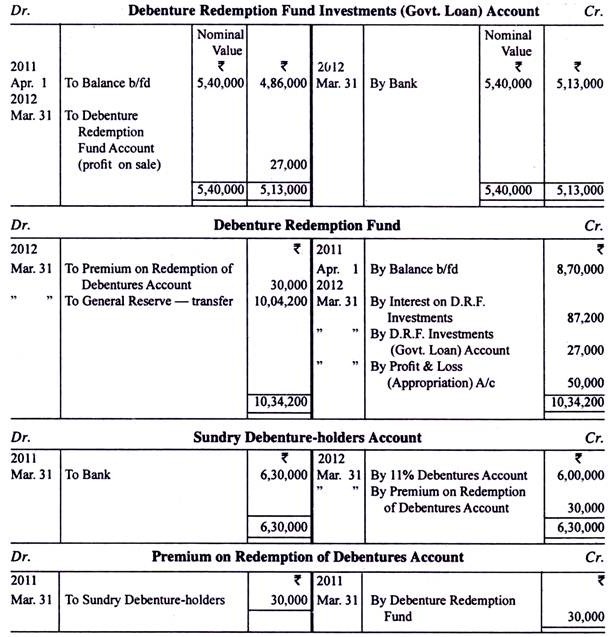

X Ltd. had Rs 10,00,000 11% debentures outstanding on 1st April, 2011. On that date, Debenture Redemption Fund was Rs 8,70,000 represented by Rs 4,00,000 Own Debentures purchased at 96% on the average and Rs 5,40,000 8% Government Loan. The annual installment for Debenture Redemption Fund was Rs 50,000.

On 31st March, 2012, the investments in Government Loan were sold at 95% and all debentures were redeemed or cancelled as necessary at a premium of 5%. The dates of interest for debentures as well as Government Loan were 30th September and 31st March.

Prepare ledger accounts relating to the abovementioned matters for the year ended 31st March, 2012.

Illustration 14:

On 31st March, 2011, the following balances were extracted from the books of X Ltd.: