Read this essay to learn about:- 1. Meaning of Dividend 2. Dividend Versus Market Price 3. Dividend Versus Capital Gains 4. Clientele Effect and Dividend Policy 5. Dividend Irrelevance Theory 6. Residual Dividend Model.

Essay # 1. Meaning of Dividend:

Dividend is return to the shareholders. Preference shareholders get fixed dividend. So there is a policy decision involved in it. But dividend paid to the equity shareholders depends on the level of cash profit earned by the company and many other factors.

Important factors for deciding dividend policy of a company are:

(i) Funds need of a company:

ADVERTISEMENTS:

A company needs funds for growth and expansion, modernization of the existing business line. Although it can borrow for capital to finance additional fund requirement, but equity expansion becomes necessary to maintain a balance in debt – equity ratio.

(ii) Availability of cash profit:

Dividend payment involves cash outflows. In case cash profit is less although there is accounting profit, a company may not be in position to pay high dividend. This happens when profit of a company remains blocked in inventories and debtors or level of trade credits shrink.

(iii) Ability to borrow:

ADVERTISEMENTS:

Although a company may pursue a debt – equity policy (financing mix) for long term funding of growth and modernization, in times there may not exist favourable borrowing situation. It may be required to temporarily put off the borrowing and pump in more equity to maintain the flow of funds for long term investments.

(iv) Requirement of the shareholders:

Shareholding pattern of the company is an important factor for deciding dividend policy which technically termed as “clientele effect”. In case the shareholders of the company depends on it for regular income, then its dividend policy has to reflect the shareholders need. On the other hand, if the shareholders want to achieve growth, they would like better reinvestment of profit by the company in new projects and lower dividend payout.

ADVERTISEMENTS:

(v) Restriction on payment dividend:

The company may have to legally pay all arrear and current interest on loans/debentures, all arrear and current dividend to preference shareholders and charge depreciation on depreciable assets before payment of dividend.

Sections 205-207 of the Companies Act, 1956 regulate the dividend payment policy and procedures:

Illustration 1:

ADVERTISEMENTS:

Given below is the draft Balance Sheet of X Ltd. as on 31-3-2004:

Of the profit and loss account balance current profit is Rs.290 million. Now the company wants to declare dividend @ 200% of the current profit, i.e. Rs.200 million.

ADVERTISEMENTS:

The Finance Director indicates that the company has undertaken a new project which would require Rs.600 million. At the current level (before including the profit earned during the current year), its equity was Rs.710 million comprising of Equity Share Capital Rs.100 million, General Reserves Rs.600 million and Profit and Loss Account balance Rs.10 million, i.e. 71% of the borrowed capital. In case the same ratio is to be maintained, then so much dividend cannot be paid.

Find out the amount of dividend which the company should pay if it wants to finance the growth projects maintaining debt equity ratio at the level of the previous financial year. What legal requirements it should take care?

Solution:

Funds required for project financing: Rs.600 million

ADVERTISEMENTS:

Debt = Rs.600 million/171%: Rs.350.88 million

Equity financing = Rs.600 million – Rs.350.88 million = Rs.249.12 million

Balance of profit and loss account: Rs.300 million

Dividend: Rs.300 million – Rs.249.12 million = Rs.50.88 million.

ADVERTISEMENTS:

The company should take care of:

(i) Restriction on higher transfer to reserves and

(ii) Dividend tax.

It needs to maintain average rate of dividend of last three years. It has to pay dividend tax @ 12.5% plus 5% surcharge. So actual dividend payment may be of lower amount.

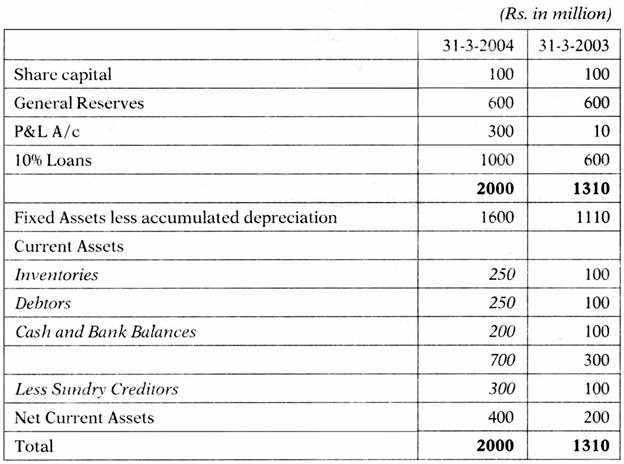

Illustration 2:

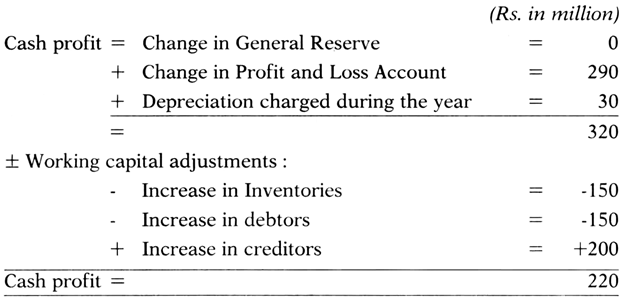

Y Ltd. has prepared the draft balance sheet as on 31-3-2004 and provided you with final balance sheet as on 31-3-2003. It wants to declare 200% dividend as it has earned a profit of Rs.290 million as appeared from the difference in the profit and loss account balance. But the finance director pleads that there is no supporting cash. In other words, cash profit of the company is not sufficient to support that much high dividend payment. Would you agree?

The company charged Rs.30 million depreciation during the year and Rs.30 million during the last year. Assume distribution tax of 12.5% and surcharge 5%. To maintain operational liquidity the company needs at least Rs.50 million. The company plans to organize annual general meeting by the end of April, 2004.

Solution:

To declare a dividend of Rs.220 million dividend tax is 12.5% of Rs.220 million plus 5% surcharge. This amounts to Rs.26.25 million.

[Also the company has to transfer to reserves 10% of the current profit, Le. 29 million. Of course, this transfer to reserve does not involve any cash.]

Therefore, total cash payout for 200% dividend is Rs.226.25 million as against cash profit of Rs.220 million. In addition, it is to be kept in mind that cash and bank balance of the company is even lower than Rs.220 million which implies that cash profit has already been utilized to fund long term investments like purchase of fixed assets.

Of course, payment of dividend does not depend on the cash and bank balance as on the balance sheet date. In case the company wants to declare dividend by the end of April 2004, then it is to be paid out by the end of May 2004. So future operational cash inflows of the next two months can also be utilized.

In case the company earns cash profit at the same average rate (Rs.220 million/12) of Rs.18.33 million, then future cash flow may cover up to Rs.36.67 million whereas the company is presently short of cash by Rs.76.25 million. Therefore, declaration of 200% dividend is not justified.

Illustration 3:

Consider the draft balance sheet as on 31-3-2004 given in Illustration 2 once more which is reproduced below:

In the past the company paid dividend as follows: 2000-01 80%, 2001-02 60% and 2002-03 100%. Now during the current year the company wants to transfer Rs.220 million to reserve out of current profit of Rs.290 million. And to declare dividend Rs.60 million. The company proposes that it would cost another Rs.7.875 million by way of dividend tax. Is it justified to make such a high transfer to general reserve?

Solution:

![]()

This requires that the current profit and loss account balance should be Rs.80 million plus dividend tax of Rs.10.5 million, Le. Rs.90.5 million. Out of Rs.300 million balance of profit, the company can then transfer at best Rs.209.5 [Rs.300 million – Rs.90.5 million].

Illustration 4:

Z Ltd. has prepared the draft balance sheet as on 31 -3-2004 and provided you with final balance sheet as on 31 -3-2003. The company has suffered loss during the year. It wants to pay dividend out of reserves. In the last year it paid dividend @ 40%. The Board thinks that the setback is of temporary by nature and the moral of the shareholders should be kept upbeat. So it should maintain dividend paid last year.

To pay 40% dividend it needs to draw just Rs. 40 million out of Rs.600 million. Guide the board taking into account the legal requirements.

Solution:

(i) To pay dividend out of reserve, it is necessary to set off the loss first out of draw down from reserves.

(ii) Rate of dividend cannot exceed 10% of paid up capital.

(iii) Maximum withdrawal from reserve for this purpose is 10% of paid up capital and free reserve, i.e. Rs.70 million.

If the company draws Rs.70 million from reserves, it cannot even offset the loss balance. Therefore, the company cannot pay dividend out of reserves in this case.

Illustration 4(a):

Z Ltd. has prepared the draft balance sheet as on 31 -3-2004 and provided you with final balance sheet as on 31 -3-2003. The company has suffered loss during the year. It wants to pay dividend out of reserves. In the last year it paid dividend @ 40%. The Board thinks that the setback is of temporary by nature and the moral of the shareholders should be kept upbeat. So it should maintain dividend paid last year.

To pay 40% dividend it needs to draw just Rs.40 million out of Rs.600 million. Guide the board taking into account the legal requirements.

Solution:

The company can pay only 10% dividend drawing from reserves. This will costs the company Rs.10 million plus dividend tax of Rs.1.3125 million, ie. Rs.11.3125 million. Any amount drawn from reserve should be utilised to set off the current loss balance. Therefore, it should draw Rs.31.3125 million from reserves.

Essay # 2. Dividend Versus Market Price:

There are two popular dividend models used for valuation equity shares:

(i) Constant dividend model; and

(ii) Dividend growth model.

As per the constant dividend model,

![]()

P0 = D0+ Ke

P0 = Current price of equity shares, D0 = Current dividend which is constant dividend as well, and Ke = Cost of equity.

This means current market price of the equity shares is affected by the rate of dividend.

Illustration 5:

A company has 100 million equity shares, each Rs.10 paid up. It pays 40% dividend. Cost of equity has been determined applying CAPM approach is 14%. What should be the market price per share? Will it be different if the company pays dividend @ 30%.

Solution:

Current market price per share for 40% dividend = Rs.4/.14 = Rs.28.57

Current market price per share for 30% dividend = Rs.3/.14 = Rs.21.43

Illustration 6:

A company has 100 million equity shares, each Rs.10 paid up. Cost of equity has been determined applying CAPM approach is 14%. Find out the market price per share of the company within dividend range of 10% -100% at an interval of 10%. Do you agree that as per constant dividend model market price per share is the linear function of dividend payout?

Solution:

As per constant dividend model market price per share is the linear function of dividend payout. See Figure 16.1.

As per dividend growth model:

![]()

![]()

P0 = Current price of equity shares,

D0 = Current dividend which is constant dividend as well, and

Ke= Cost of equity,

g = rate of growth, g < Ke

This means current market price of the equity shares is affected by the rate of dividend.

Illustration 7:

A company has 100 million equity shares, each Rs.10 paid up. It pays 40% dividend. Cost of equity has been determined applying CAPM approach is 14%. What should be the market price per share? Will it be different if the company pays dividend @ 30%. Rate of growth of dividend is 5% p.a.

Solution:

Current market price per share for 40% dividend = (Rs.4 × 1.05)/(.14 -.05) = Rs.46.67

Current market price per share for 30% dividend = (Rs.3 × 1.05)/(.14 -.05) = Rs.35.00

Dividend growth model supplements that market price per share gets a boaster when there is growth in dividend.

Does the market price depends on dividend? Probably not. Even if the company does not pay dividend but is having a future growth prospect, the investors like that share in the expectation of capital gains.

Illustration 8:

A company has 100 million equity shares, each Rs.10 paid up. Cost of equity has been determined applying CAPM approach is 14%. Find out the market price per share of the company within dividend range of 10% -100% at an interval of 10%. Expected dividend growth rate is 5%. Do you agree that as per constant dividend model market price per share is the linear function of dividend payout?

Solution:

As per dividend growth model market price per share is the linear function of dividend payout. See Figure 16.2. Now study the comparative position of market price per share under constant dividend model and dividend growth model given in Figure 16.3.

Legend:

MP 1 = Market price as per constant dividend model

MP2 = Market price as per dividend growth model

Growth prospect pushes up the market price.

Essay # 3. Dividend Versus Capital Gains:

While deciding the dividend policy, it is always a balancing between the current market price and the future market price. Higher retention in a growth company may generate better market value than it could be achieved by higher pay out.

Illustration 9:

For the sake of simplicity let us take an equity financed company with cost of equity 12%. Its present equity comprises of Rs.100 million Equity Share capital and Rs.400 million Reserves & Surplus. In addition, its current profit is Rs.100 million. It presently earns @ 20% on capital employed which is expected to be @ 25% on new investments. Cost of equity is 14%.

Three proposals are there:

(i) The company should pay out the entire current profit of Rs.100 million;

(ii) The company should pay out 50% of the current profit, i.e. Rs.50 million;

(iii) The company shouldn’t pay any dividend.

Ignore dividend tax. Current market price (before dividend information) is Rs.50.

What should be the appropriate dividend policy of the company? Investors expect to get 14% average market return.

Solution:

(i) If the company declares 100% dividend, i.e. the entire amount of current profit its cum dividend share price is expected to be Rs.71.43 (Rs.10/.14).

(ii) If the company declared 50% dividend, i.e. 50% of the current profit, its cum dividend share price is expected to be Rs.35.71 (Rs.5/.14).

Expected future earning after one year will be Rs.100 million plus Rs.12.5 million = Rs.112.25 million. Value of equity after one year is expected to be Rs.112.25/.14 = Rs.801.79 million, i.e. market price per share Rs.80.18.

(iii) If the company reinvests the entire current profit, expected future earning after one year will be Rs. 100 million plus Rs. 25 million = Rs. 125 million. Value of equity after one year is expected to be Rs. 125/.14 = Rs.892.16 million, i.e. market price per share Rs.89.16.

Case 1: Shareholders earn normal market return of 14%

Case 2: Shareholders earn 60.36%, [Rs.80.18/50 -1] × 100

Case 3: Shareholders earn 78.57%, [Rs.89.16/50 -1] × 100

So as the future growth prospect gives better return, the shareholders may opt for higher retention policy in case there is no urgent need for cash in general. But generally, to cater the need of various categories of shareholders, companies may wish to maintain a balance between growth and pay out. Thus Case 2 may be suitable for companies which wish to take a middle path.

Essay # 4. Clientele Effect and Dividend Policy:

Different groups of investors, or clienteles, prefer different dividend policies. Firm’s past dividend policy determines its current clientele of investors. Shareholders like senior citizens require cash flow out of their investments whereas young professionals may prefer growth rather than current dividend. A company needs to balance the different requirements of the different group of shareholders. Alternatively, the shareholders decide about the investments looking into the dividend policy of the company.

Clientele effects affect the dividend policy. Taxes & brokerage costs hurt investors who have to switch companies.

1. Individual investors do have definite dividend preferences because of their needs for more or less current income.

2. Retirees living on fixed income would prefer a steady income compensated by purchasing power. They would like cash dividend.

3. On the other hand, young professionals would prefer capital appreciation.

4. Each company develops a clientele of investors whose needs match its dividend paying characteristics, hence the term clientele effect.

While deciding dividend policy, a company should pay proper attention to the clientele effect.

1. Signaling Effect of Dividend Retention Policy:

When a company wants to retain the profit cutting dividend, it gives a growth signal to the investors. However, another approach is that when a company increases dividend, it implies that it would be able to sustain the high dividend in future. Thus contrary to traditional retention policy theory, high payout is a signal of growth.

Signalling hypothesis implies that:

i. Managers hate to cut dividend, so won’t raise dividends unless they think dividend rise is sustainable. So, investors view dividend increase as signals of management’s view of the future.

ii. Therefore, a stock price increases at the time of a dividend increase could reflect higher expectations for future EPS, not a desire for dividend.

iii. Cash dividend signals management’s confidence in the future.

iv. An increase in the dividend gives stronger message of growth. An increase in dividend accompanied by increase in earning gives message that growth is permanent.

In a year earning may be down, but management desires to maintain dividend. For this purpose many companies maintain Dividend Equalization Reserve. The message to the shareholders is, “Low EPS during the current year is not there to stay, don’t worry about it. Things will be fine. In the long run we expect to have plenty of money, so here’s your regular dividend.”

v. Similarly, decrease in dividend coupled with dividend cut signifies a terrible news.

In this context we should now study the “Dividend Irrelevance” theory of Modigliani and Miller and try to appreciate the concept of dividend irrelevance.

2. Clientele Effect of Dividend Retention Policy:

Different groups of investors, or clienteles, prefer different dividend policies. Firm’s past dividend policy determines its current clientele of investors. Shareholders like senior citizens require cash flow out of their investments whereas young professionals may prefer growth rather than current dividend. A company needs to balance the different requirements of the different group of shareholders. Alternatively, the shareholders decide about the investments looking into the dividend policy of the company.

Clientele effects affect the dividend policy. Taxes & brokerage costs hurt investors who have to switch companies.

1. Individual investors do have definite dividend preferences because of their needs for more or less current income.

2. Retirees living on fixed income would prefer a steady income compensated by purchasing power. They would like cash dividend.

3. On the other hand, young professionals would prefer capital appreciation.

4. Each company develops a clientele of investors whose needs match its dividend paying characteristics, hence the term clientele effect.

While deciding dividend policy, a company should pay proper attention to the clientele effect.

Essay # 5. Dividend Irrelevance Theory:

Modigliani and Miller have propagated dividend irrelevance theory.

We are presenting here restrictive assumptions of the MM proposition in the language of Brigham (Financial management: Theory and Practice, Brigham & Ehrhardt, 10th edition):

i. It is possible in the Land of Ez, where the environment is quite simple. First, the king being kind soul does not impose any tax.

ii. Second, investors can buy and sell securities without paying any sales commission.

iii. Third, there is no floatation cost of securities.

iv. Fourth, the Land of Ez is completely computerized, so that all information about firms is instantaneously available to the public at no cost.

v. Fifth, all investors believe that value of a company is a function of its investment opportunities and financing decisions.

vi. Sixth, all firms are owned and managed by same parties so there is no agency cost.

Within the framework of their assumption, Modigliani and Miller argued that dividend policy is irrelevant. This theory argues that dividend policy has no effect on either the price of a firm’s stock or its cost of capital. Firm value, they contended, is determined by basic earning power and business risk. Therefore, a firm’s value is based only on fundamental factors, and dividend policy is irrelevant.

On the contrary, Myron J. Gordon and John Linter argued that dividend theory is relevant and there exists a direct relationship between dividend rate and market value of the firm, which is termed as “Bird in the Hand” approach.

Finally, there is a residual theory of dividend which proposes that dividend payout is decided by available cash after meeting the reinvestment plan.

Essay # 6. Residual Dividend Model:

The following steps are followed for finding out dividend payout ratio under this model:

1. Find the retained earnings needed for the capital budget.

2. Pay out any leftover earnings (the residual) as dividends.

3. This policy minimizes flotation and equity signalling costs, hence minimizes the WACC.

Dividend = Net Income – Target Ratio × Total Capital Budget

Illustration 10:

Capital budget of a company is: Rs.800, 000.

Given target capital structure: 40% debt, 60% equity.

Forecasted net income: Rs.600, 000.

How much of the Rs.600,000 should we pay out as dividend?

How would a drop in Net Income to Rs.400, 000 affect the dividend? A rise to Rs.800, 000?

Solution:

Of the Rs.800,000 capital budget, 0.6 (Rs.800,000) = Rs.480,000 must be equity to keep at target capital structure. [0.4(Rs.800,000) = Rs.320,000 will be debt.]

With Rs.600,000 of net income, the residual is Rs.600,000 – Rs.480,000 = Rs.120,000 = dividend paid.

Payout ratio = Rs.120,000/Rs.600,000

= 0.20 = 20%.

NI = Rs.400, 000: Need Rs.480, 000 of equity, so the company should retain the whole earning Rs.400, 000. Dividend = 0.

NI = Rs.800,000: Dividend = Rs.800,000 – Rs.480,000 = Rs.3,20,000. Payout = Rs.3,20,000/Rs.800,000 = 40%.