In this article we will discuss about the conversion of accrual basis income to cash basis income.

The profit and loss account focuses on net income determination from operating activities. However, it does not show cash inflow and outflow relating to operating activities because the profit and loss account is prepared on accrual basis. In preparing profit and loss account, revenues are recorded even though cash for them has not been received. Similarly, expenses are recorded even though they may not have been paid.

Therefore, to find cash flows from operations, one need to convert accrual basis income statement figures to cash basis by making adjustments.

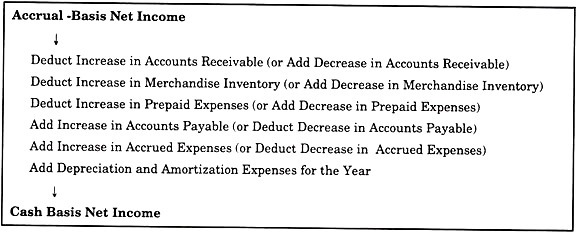

By way of adjustments, earned revenues will be converted into cash received from sales or customers and incurred expenses will be converted into cash expended, i.e., expenses actually paid in cash. The conversion of accrual basis income statement to cash basis income statement along with required adjustments has been shown in Exhibit 16.7.

ADVERTISEMENTS:

The conversion process displayed in Exhibit 16.7 can be described as follows, using a shortcut calculation:

While making conversion, one should know the relationship between income statement accounts and balance sheet changes. Each individual item on the income statement should be viewed as it relates to a balance sheet account. On the accrual basis of accounting, the explanation for the difference between the amount of sales revenue and the receipts from those sales is found in the changes in accounts receivable and debtors account.

Similarly, the difference between the amount of an expense and the amount of payments for that expense is found in the changes of its associated asset or liability, such as prepaid rent or rent payable.

ADVERTISEMENTS:

If there is no associated balance sheet account for an item on the income statement, it is presumed that the amount shown on the income statement resulted in a cash flow exactly equal to that revenue or expense. Exhibit 16.8 shows relationship between some income statement accounts and balance sheet accounts.