In this article we will discuss about the Forfeiture and Reissue of Shares:- 1. Introduction to Forfeiture and Reissue of Shares 2. Journal Entries on Forfeiture (or Surrender) and Reissue of Shares 3. Solved Illustrations.

Introduction to Forfeiture and Reissue of Shares:

If a shareholder fails to pay allotment money or a call or a part thereof by the last date fixed for payment, the Board of Directors, if Articles of Association of the company empower it to do so, proceed to forfeit the shares on which allotment money or call has become in arrear.

The Articles of Association lay down the procedure. A notice has to be served on the defaulter requiring him to pay the unpaid amount together with interest accrued by a certain date.

The notice also must state that in the event of non-payment on or before the date so named, the shares in respect of which the notice has been served will be liable to be forfeited. When shares are forfeited, the shareholder’s name is removed from the register of members and the amount already paid by him on shares is forfeited to the company.

ADVERTISEMENTS:

It is a capital gain and is credited to Forfeited Shares Account. A forfeited share may be reissued even at a loss. But the loss on reissue cannot exceed the gain on forfeiture of the share reissued.

As in the absence of any provisions to the contrary, provisions of Table A apply, it is necessary to note the following provisions of Table A relating to forfeiture and reissue of shares:-

1. If a member fails to pay any call or installment of a call on or before the day appointed for payment thereof, the Board may, at any time thereafter during such time as any part of the call or installment remains unpaid, serve a notice on him requiring payment of so much of call or installment as is unpaid, together with any interest which may have accrued.

2. The notice aforesaid shall:

ADVERTISEMENTS:

(a) Name a further day (not being earlier than the expiry of fourteen days from the date of the service of the notice) on or before which the payment required by the notice is to be made; and

(b) State that, in the event of non-payment on or before the day so named, the shares in respect of which the call was made will be liable to be forfeited.

3. If the requirements of any such notice as aforesaid are not complied with, any shares in respect of which the notice has been given may, at any time, thereafter, before the payment required by the notice has been made, be forfeited by a resolution of the Board to that effect.

4. (a) A forfeited share may be sold or otherwise disposed of on such terms and in such manner as the Board thinks fit.

ADVERTISEMENTS:

(b) At any time before a sale or disposal as aforesaid, the Board may cancel the forfeiture on such terms as it thinks fit.

Forfeiture of Shares:

Sometimes, when a shareholder finds that he is unable to pay the calls made on him, he may voluntarily surrender shares to the company. The effect of surrender of shares is the same as that of forfeiture. The difference is that in case of surrender, the shareholder himself takes the initiative and the company is saved from the formalities of serving a notice and waiting till the period of the notice is over.

Journal Entries on Forfeiture (or Surrender) and Reissue of Shares:

When Shares have been Issued at Par:

ADVERTISEMENTS:

When shares which have been issued at par are forfeited, first find out the amount with which Share Capital Account has been credited in respect of forfeited shares; debit Share Capital Account with this amount. Now, this amount can be split in two parts; the amount which has been received and the amount which has not been received and because of which the shares have been forfeited.

The amount which has been received is a capital gain to the company and is credited to Forfeited Shares Account (or Share Forfeiture Account or Shares Forfeited Account). The amount which has not been received may be lying in Calls in Arrear Account or if the company has not opened Calls in Arrear Account, in Share Allotment Account or different call accounts.

Credit Calls in Arrear Account or Share Allotment Account and various call accounts as may be appropriate in the particular case with the amount not received. Suppose, a company issues equity shares of Rs 10 each at par.

Further assume that the application and allotment moneys @ Rs 2,50 and @ Rs 2.50 per share respectively are received in respect of all the shares, but the first call and the second call @ Rs 3 and @ Rs 2 per share respectively are not received in respect of 500 shares which are therefore forfeited.

ADVERTISEMENTS:

The following will be the entry on forfeiture of these shares if Calls in Arrear Account has not been opened:—

Equity Share Capital Account Dr. 5,000

To Equity Share First Call Account 1,500

To Equity Share Second Call Account 1,000

ADVERTISEMENTS:

To Forfeited Shares Account 2,500

Forfeiture of 500 equity shares, on which amount @ Rs 5 per share has been received as application and allotment moneys for non-payment of the first call @ Rs 3 per share and the second and final call @ Rs 2 per share.

If the amounts not received on the two calls have been transferred to Calls in Arrear Account, Equity Share First Call Account and Equity Share Second Call Account will stand closed and will be represented by Calls in Arrear Account.

In this case, the entry on forfeiture of shares will be as follows:

ADVERTISEMENTS:

Equity Share Capital Account Dr. 5,000

To Calls in Arrear Account 2,500

To Forfeited Shares Account 2,500

Narration of the entry will be the same as stated in the earlier case.

Alternatively, the total called up amount in respect of forfeited shares is debited to Share Capital Account and credited to Forfeited Shares Account.

Then, Forfeited Shares Account is debited and Share Allotment Account and various call accounts (or Calls in Arrear Account) are credited with the amount not received in respect of forfeited shares; it leaves a balance in Forfeited Shares Account which is equal to amount received in respect of forfeited shares.

ADVERTISEMENTS:

Thus, in this second method of passing entries on forfeiture of shares, the final effect is the same as in the first method.

Entries for the above mentioned illustration under this method will be as follows:-

1. Equity Share Capital Account Dr. 5,000

To Forfeited Shares Account 5,000

Transfer of called up amount in respect of 500 forfeited equity shares from Equity Share Capital Account to Forfeited Shares Account.

2. Either

Forfeited Shares Account Dr. 2,500

To Equity Share First Call Account 1,500

To Equity Share Second Call Account 1,000

or

Forfeited Shares Account Dr. 2,500

To Calls in Arrear Account 2,500

Transfer of amount not received in respect of forfeited shares to Forfeited Shares Account. Forfeited shares can be reissued. They can be reissued even at a price lower than the paid up value of the reissued shares at the time of reissue. But the loss on reissue of a share cannot be more than the gain on forfeiture of that share credited to Forfeited Shares Account at the time of forfeiture.

If a share is reissued at a loss, on reissue Bank is debited with cash received, Forfeited Shares Account is debited with loss suffered (or discount allowed) and Share Capital Account is credited will the total of the two amounts which is the paid up value of reissued shares.

If the loss on reissue is less than the gain on forfeiture of a share, there is a net capital gain to the company which is transferred from Forfeited Shares Account to Capital Reserve; as such, Forfeited Shares Account is debited and Capital Reserve is credited.

If forfeited shares are reissued at a premium, the amount of such a premium will be credited to Securities Premium Account. If shares are reissued at par or at a premium, the amount of gain credited to Forfeited Shares Account at the time of forfeiture of these reissued shares will be transferred from Forfeited Shares Account to Capital Reserve.

If all the forfeited shares have not been reissued, Forfeited Shares Account will show a credit balance equal to gain on forfeiture of the shares not yet reissued.

Solved Illustrations on Forfeiture and Reissue of Shares:

Illustration 1:

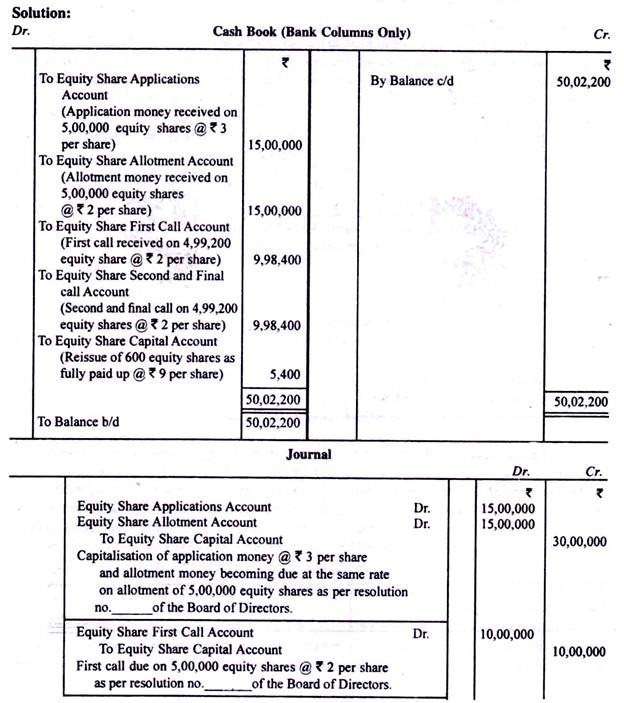

Amber Ltd. with an authorized capital of Rs 1,00,00,000 offered to public 5,00,000 equity shares of Rs 10 each payable as to Rs 3 with application, Rs 3 on allotment and the balance in two equal calls of Rs 2 each. The company got the applications for all the shares offered.

All the applications were accepted. One shareholder holding 800 shares did not pay the first call. After completing the legal formalities, the Board of Directors forfeited these shares. Consequently, the second call was made on 4,99,200 shares only which was duly received in full. Then, the Board of Directors reissued three-fourths of the forfeited shares as fully paid up @ Rs 9 per share.

Record the abovementioned transactions in the Cash Book, the Journal and the Ledger. Also, prepare the Balance Sheet as it would appear after all the above mentioned transactions have been recorded.

Illustration 2:

(a) X Ltd. forfeits 100 12% preference shares of Rs. 25 each, fully called up on which Rs 1,500 have been received and reissues them as fully paid up to one of the directors upon payment of Rs 2,300. Give the necessary journal entries.

(b) Y Ltd. forfeits 200 equity shares of Rs 10 each issued at par for non-payment of the first call @ Rs 2 per share and the second and final call @ Rs 3 per share. The shares are reissued as fully paid up to one of the directors @ Rs 9 per share. No entries are made on forfeiture but when the shares are reissued, the cash received is credited to Equity Share Capital Account. Give the rectifying entry.

Thus, Bank has been correctly debited. Equity Share Capital Account has received an unwanted credit while Equity Share First Call Account, Equity Share Second & Final Call Account and Capital Reserve have not received the due credit.

Hence, the following rectifying entry will be passed:—

When shares have been Issued at a Premium.

If shares issued at a premium are forfeited, find out whether the premium on forfeited shares has been realised or not. If premium on forfeited shares has been received, Securities Premium Account must not be debited on forfeiture of shares. It is obligatory because of legal restrictions placed by section 78 of the Companies Act on the uses of securities premium received.

It means that securities premium once received is not to be written back even if shares are forfeited subsequently. Entry on forfeiture will therefore be passed as if the shares had been issued at par and no premium had been received.

However, if the premium on forfeited shares has not been received but it has been credited to Securities Premium Account and debited to Share Allotment Account (or a Call Account) at the time of the premium becoming due; on forfeiture, Securities Premium Account will be debited and Share Allotment Account (or Call Account) will be credited with the premium not received.

If the company credits Securities Premium Account only when the premium has been received, then the question of debiting Securities Premium Account on forfeiture will not arise.

On reissue, Securities Premium Account will not be credited if the premium had been received in respect of the shares before forfeiture. Of course if the reissue price exceeds the paid up value of reissued shares, Securities Premium Account will have to be credited with such an excess.

If shares on which securities premium had not been received till forfeiture are reissued, Securities Premium Account will be credited with the amount of securities premium in respect of reissued shares and the amount to be debited to Forfeited Shares Account will be calculated after taking this credit into consideration.

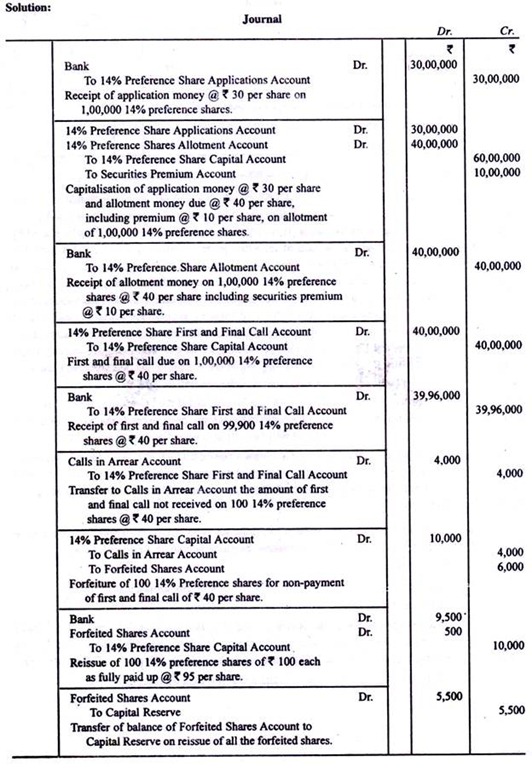

Illustration 3:

Poonam Co. Ltd. offered to public for subscription 1,00,000 14% preference shares of Rs 100 each at a premium of Rs 10 per share. Payment was to be made as follows.

On application Rs 30

On allotment Rs 40 (including premium)

On first and final call Rs 40

Applications were received for all the shares offered and allotment was duly made. All moneys were duly received except the money on call on 100 shares which were forfeited after the requisite notices had been served. Later, all the forfeited shares were reissued as fully paid up @ Rs 95 per share.

Journalise all the above mentioned transactions including cash transactions.

Illustration 3:

Neelam Co. Ltd. issues 5,00,000 equity shares of Rs 10 each at a premium of 25%, Rs 4 per share being payable along with application and the balance including premium being payable on allotment. Applications total 4,80,000 shares.

All the applications are fully accepted. Allotment money on 200 shares is not received. After due notices have been served, these shares are forfeited. Later, all these shares are reissued as fully paid up @ Rs 9 per share.

Pass journal entries for the above mentioned transactions crediting Securities Premium Account:

(a) Only when the amount of the premium has been received,

(b) As soon as the amount of the premium becomes due.

Illustration 4:

Kay Ltd. with an authorized capital of Rs 30,00,000 offered to public 2,00,000 equity shares of Rs 10 each at a premium of Rs 1 each.

The payment was to be made as follows:—

With application Rs 3

On allotment Rs 5 (including premium)

On first and final call Rs 3

Applications totalled 4,00,000 shares; Shares were allotted on a pro rata basis. Arun who had applied for 400 shares and to whom 200 shares had been allotted failed to pay the balance of allotment money due from him.

His shares were forfeited and then reissued to Tarun as Rs 8 (including premium of Rs 1) per share paid up @ Rs 6 per share. Ramesh, another shareholder, failed to pay the call money on 100 shares held by him. His shares were also forfeited. Later, these shares were reissued as fully paid up to Suresh @ Rs 12 per share.

Expenses of the issue came to Rs 12,000.

Prepare the Journal, the Cash Book, the Ledger and the Balance Sheet on the basis of the information given above.

Forfeiture (or Surrender) and Reissue:

When shares have been issued at a discount: If shares which have been issued at a discount are forfeited shares and the discount in respect of forfeited shares has been debited to Discount on Issue of Shares Account, on forfeiture while passing the entry for forfeiture, the amount of such discount is credited to Discount on Issue of Shares Account.

On reissue of these shares, Discount on Issue of Shares Account is once again debited with the amount of the discount originally allowed on the shares reissued provided the amount received on reissue of these shares is less than the paid up value of these shares by at least the amount of such discount.

Illustration 5: (19)

A Ltd. invited applications for 1,00,000 shares of Rs 100 each at a discount of 6% payable as follows:

On Application Rs 25

On Allotment Rs 34

On First and Final Call Rs 35

The applications received were for 99,000 shares and all of these were accepted. All moneys due were received except the first and final call on 100 shares which were forfeited. 50 shares were re-issued @ Rs 90 as fully paid.

Assuming that all requirements of the law were complied with, pass entries in the Cash Book and Journal of the company. Also show how these transactions will be reflected in the company’s balance sheet. [C.S. (Inter) June, 1998 Modified]

Illustration 6:

Zed Ltd. issued 5,00,000 equity shares of Rs 10 each at a discount of 10% payable as to Rs 2.50 per share along with application, Rs 2.50 per share on allotment and the balance on the first and the final call to be made six months after allotment. The issue was fully subscribed for.

Call on 300 shares was not received. These shares were forfeited. Half of these shares were reissued as fully paid up @ Rs 8 per share. Two months later, the remaining forfeited shares were reissued as fully paid up @ Rs 11 per share.

Pass journal entries for the above mentioned transactions.