In this article we will discuss about the Final Accounts of General Insurance Business along with solved illustrations.

Insurance other than life insurance is called general insurance. Fire insurance against loss of property due to fire and marine insurance against loss of cargo, freight and ship are examples of general insurance

Reserve for Unexpired Risks:

An insurance company issues general insurance policies throughout the accounting year. Premium is received at the time of issue of the policy. But the period for which the policy is issued may cover part of the current accounting year and a part of the next accounting year.

ADVERTISEMENTS:

It means the company may be required to pay for losses which may take place next year in respect of at least some of the policies issued in the current accounting year. It is therefore, wrong to consider the premium received in an accounting year to be income of the insurance company without taking into account a reserve for unexpired risks.

Schedule II B of the Insurance Regulatory and Development Authority (Assets, Liabilities and Solvency Margin of Insurance) Regulation 2000 lays down that the reserve for unexpired risks, shall be, in respect of:

(i) Fire business, 50 per cent,

(ii) Miscellaneous business, 50 per cent

ADVERTISEMENTS:

(iii) Marine business other than marine hull business, 50 per cent, and

(iv) Marine hull business, 100 per cent of the premium, net of reinsurances, received or receivable during the preceding twelve months.

To ascertain the amount of surplus for which a general insurance company can take credit in respect of a particular type of general insurance business, in the relevant Revenue Account, net premium earned is adjusted for Reserve for Unexpired Risks as in the beginning and as at the end of the accounting year concerned.

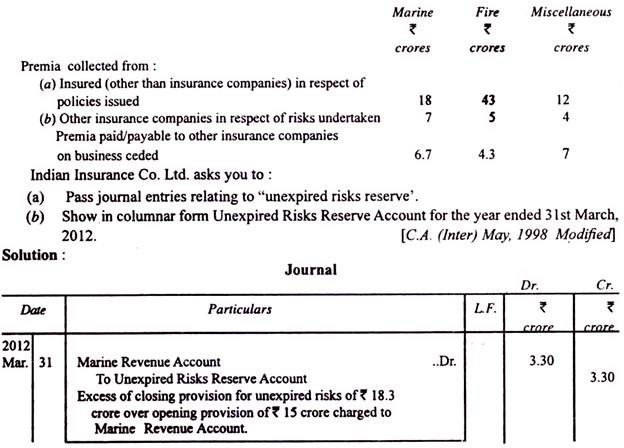

Illustration 1:

ADVERTISEMENTS:

Indian Insurance Co. Ltd. furnishes you with the following information:

(i) On 31.3.2011 it had reserve for unexpired risks to the tune of Rs 40 crore. It comprised of Rs 15 crore in respect of marine insurance business; Rs 20 crore in respect of fire insurance business and Rs 5 crore in respect of miscellaneous insurance business.

(ii) It is the practice of Indian Insurance Co. Ltd. to create reserve at 100% of net premium income in respect of marine insurance policies and at 50% of net premium income in respect of fire and miscellaneous insurance policies.

(iii) During the year ended 31st March, 2012, the following business was conducted:

Notes: to forms B-RA and B-PL

ADVERTISEMENTS:

(a) Premium income received from business concluded in and outside India shall be separately disclosed.

(b) Reinsurance premiums whether on business ceded or accepted are to be brought into account gross (i.e. before deducting commissions) under the head reinsurance premiums,

(c) Claims incurred shall comprise claims paid, specific claims settlement costs wherever applicable and change in the outstanding provision for claims at the year-end.

(d) Items of expenses and income in excess of one percent of the total premiums (less reinsurance) or Rs 5,00,000 whichever is higher, shall be shown as a separate line item.

ADVERTISEMENTS:

(e) Fees and expenses connected with claims shall be included in claims.

(f) Under the sub-head “others” shall be included items like foreign exchange gains or losses and other items.

(g) Interest dividends and rentals receivable in connection with an investment should be stated as gross amount, the amount of income tax deducted at source being included under ‘advance taxes paid and taxes deducted at source”.

ADVERTISEMENTS:

(h) Income from rent shall include only the realised rent. It shall not include any notional rent.

Notes:

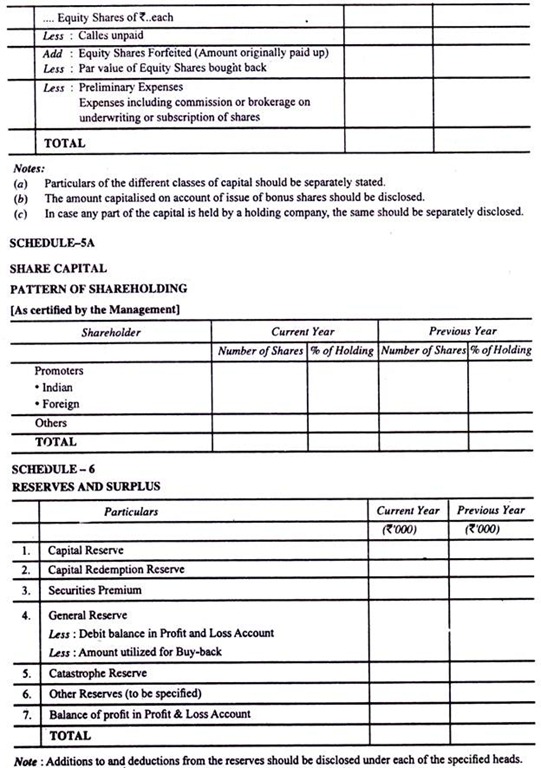

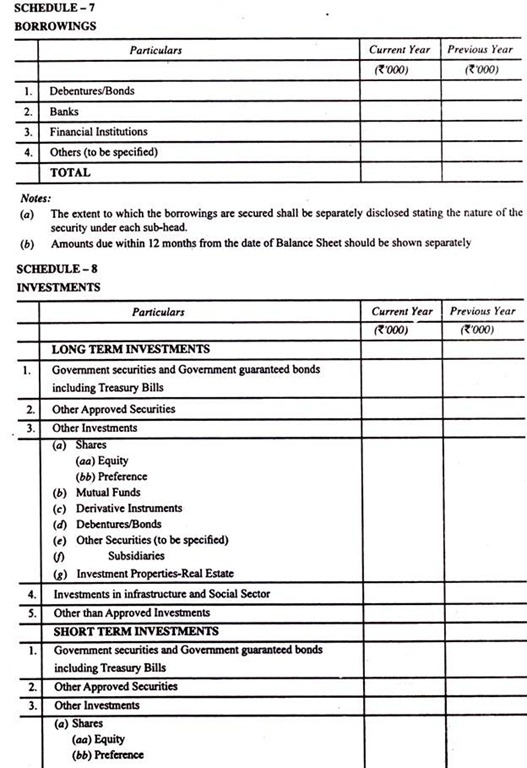

(a) Investments in subsidiary/holding companies, joint ventures and associates shall be separately disclosed, at cost.

(i) Holding company and subsidiary shall be construed as defined in the Companies Act, 1956.

(ii) Joint Venture is a contractual arrangement whereby two or more parties undertake an economic activity, which is subject to joint control.

(iii) Joint control is the contractually agreed sharing of power to govern the financial and operating policies of an economic activity to obtain benefits from it.

(iv) Associate is an enterprise in which the company has significant influence and which is neither a subsidiary nor a joint venture of the company.

(v) Significant influence (for the purpose of this schedule) means participation in the financial and operating policy decisions of a company, but not control of those policies. Significant influence may be exercised in several ways, for example, by representation on the board of directors, participation in the policy making process, material inter-company transactions, interchange of managerial personnel or dependence on technical information. Significant influence may be gained by share ownership, statute or agreement. As regards share ownership, if an investor holds, directly or indirectly through subsidiaries, 20 percent or more of the voting power of the voting power of the investee, it is presumed that the investor does have significant influence unless it can be clearly demonstrated that this is not the case. Conversely, if the investor holds, directly or indirectly through subsidiaries, less than 20 percent of the voting power of the investee, it is presumed that the investor does not have significant influence, unless such influence is clearly demonstrated. A substantial or majority ownership by another investor does not necessarily preclude an investor for having significant influence.

(b) Aggregate amount of company’s investment other than listed equity securities and derivative instruments and also the market value thereof shall be disclosed.

(c) Investments made out of Catastrophe Reserve should be shown separately.

(d) Debt securities will be considered as “held to maturity” securities and will be measured at historical cost subject to amortisation.

(e) Investment Property means a property [land or building or part of a building or both] held to earn rental income or for capital appreciation or for both, rather than for use in services or for administrative purposes.

(f) Investments maturing within twelve months from balance sheet date and investments made with the specific intention to dispose of within twelve months from balance sheet date shall be classified as short- term investments.

Illustration 2:

From the following particulars, prepare the Fire Revenue Account for 2011 – 2012:

Illustration 3:

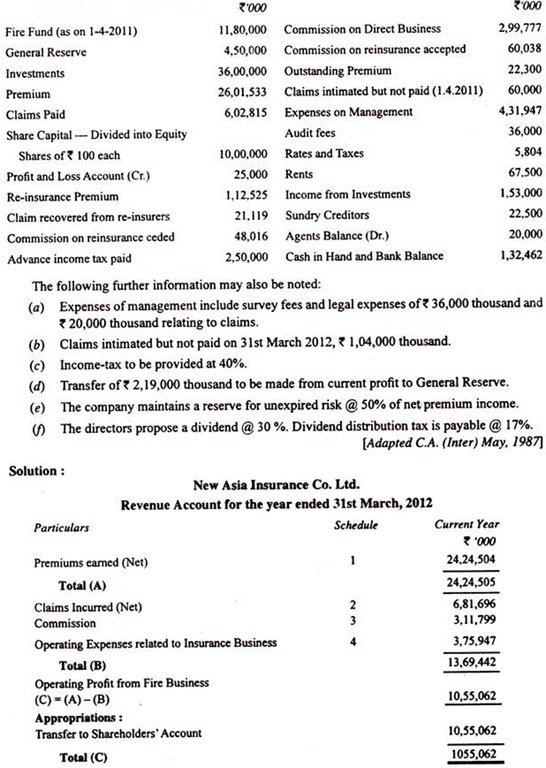

From the following figures taken from the books of New Asia Insurance Co. Ltd. doing fire underwriting business, prepare the set of final accounts for the year 2011-2012: