The below mentioned article provides an overview on the Valuation of Goodwill:- 1. Meaning of Goodwill 2. Need for Valuation of Goodwill 3. Components of Goodwill 4. General Factors Affecting the Value of Goodwill 5. Profitability on Valuation of Goodwill 6. Expected Developments 7. Yield Expected by Investors from Valuation of Goodwill 8. Capital Employed for Valuation of Goodwill.

Contents:

- Meaning of Goodwill

- Need for Valuation of Goodwill

- Components of Goodwill

- General Factors Affecting the Value of Goodwill

- Profitability on Valuation of Goodwill

- Expected Developments

- Yield Expected by Investors from Valuation of Goodwill

- Capital Employed for Valuation of Goodwill

1. Meaning of Goodwill:

Goodwill is an intangible asset but not fictitious. Sometimes a tangible asset is less valuable than goodwill. A tramway company may have spent lakhs of rupees on laying the track and is justified in treating the expenditure as an asset. Yet, the realisable value of the track will only be a small function of the amounts spent unless the tram ways are profitable and unless the track is being sold as part of a going concern.

ADVERTISEMENTS:

It is so also with goodwill. Goodwill is a valuable asset if the concern is profitable; it is valueless if the concern is a losing concern. Goodwill is the value of the reputation of the firm judged in respect of its capacity to bring in, unaided, profits.

Prof. Dicksee says, “When a man pays for goodwill he pays for something which places him in the position of being able to earn more money than he would be able to do by his own unaided efforts”.

Another authority says, “Thus given a business, the goodwill of which is for disposal, there would be no valuable goodwill if anyone could do just as well by establishing a business de novo.” Goodwill may be defined as the value of the reputation of a business house in respect of profits expected in future over and above the normal level of profits earned by undertakings belonging to the same class of business.

A firm may enjoy better profits or even profitability than other firms in the industry because of numerous factors, some of which are stated below:—

ADVERTISEMENTS:

(i) Favourable location in respect of source of raw materials or of markets or of both, enabling the firm to enjoy substantial economies through saving in freight or through facility in sales.

(ii) Favourable long-term contracts as regards supply of raw materials or components or as regards sales.

(iii) Exclusive use of patents or trade marks on the basis of which competition from similar products is avoided.

(iv) Know-how, i.e., knowledge about the peculiar problems facing the industry (both in respect of production and marketing) and about how to overcome them. Often this knowledge is acquired through collaboration with foreign firms but it is also acquired through experience, well pondered, and through systematic research,

ADVERTISEMENTS:

(v) Active, intelligent, dynamic and forward looking management. Factors (i) to (iii) are rather temporary; factors (iv) and (v) are enduring in nature. Strictly speaking, enduring goodwill should be in respect of know-how and management only—it comes about through the quality and calibre of the human resources at the disposal of the undertaking.

Here goodwill will be used in its wide meaning as including the value of future profits arising from whatever source or reason such as technical knowledge and experience (know-how), near- monopoly position, etc. It is, of course, possible to put a value on each major factor separately. In that case, the term goodwill will have a narrow meaning—value of the reputation only of the firm including that of its management.

2. Need for Valuation of Goodwill:

Goodwill is realisable only if the business is disposed of No one would consider selling the goodwill, i.e., the firm’s name and its special advantages while still trying to run the old business and no one will probably buy goodwill on the condition that the previous firm will continue to exist. Therefore, a question may arise as to the necessity of valuation of goodwill.

ADVERTISEMENTS:

In case of a joint stock company, the need for evaluating goodwill may arise in the following cases:—

(a) When the company has previously written off goodwill and wants to write it back in order to wipe off or reduce the debit balance in the Profit and Loss Account.

(b) When the business of the company is to be sold to another company or when the company is to be amalgamated with another company,

(c) When, stock exchange quotations not being available, shares have to be valued for taxation purposes.

ADVERTISEMENTS:

(d) When a large block of shares, such as to enable the holder to exercise control over the company concerned, has to be bought or sold.

(e) When one class of shares is to be converted into another.

3. Components of Goodwill:

Conceptually, it is possible to analyse the super profits earned by a firm by the factors involved.

ADVERTISEMENTS:

Goodwill may therefore be broken up into various parts, related to:

(i) Know-how possessed by the firm;

(ii) Advantage enjoyed by it because of certain patents available to it:

(iii) Special locational advantage;

ADVERTISEMENTS:

(iv) Special commercial advantages such as a long-term contract for supply of raw materials at a low price or for sale of finished goods at remunerative prices;

(v) Advantage because of prior entry specially if later entry is made difficult through a system of licensing that may be in force or some such other factor; and

(vi) Managerial superiority.

If it is possible to analyse profits in the manner mentioned above, the goodwill attaching each of the factors can be separately calculated. However, generally such an attempt is not made since it is difficult to disentangle the various forces leading to business results. Sometimes, however, such calculation becomes unavoidable — for example when compensation has to be paid for forcing a business firm to give up its present location.

4. General Factors Affecting the Value of Goodwill:

The main factors affecting goodwill are the following:—

ADVERTISEMENTS:

(a) Profits expected to be earned by the firm or company including those arising from its special advantages.

One must realise at the very outset that when one acquires a firm and its goodwill, one is hoping to earn good profits in the future. If, for any reason, it is evident that profits in the future will be low, one will not pay much for goodwill—perhaps one will decline to acquire the firm itself Good past profits are not relevant except to the extent they point to the possibility of earning good profits in the future also.

(b) The yield expected by investors in the industry to which the firm or the company belongs.

(c) The amount of capital employed to earn the profit mentioned in (a) above.

(d) Special factors relevant to a particular situation, for instance those to be considered when the Government acquires control over a company by executive order.

5. Profitability on Valuation of Goodwill:

It is not well recognised that profitability of a concern is the chief factor in the valuation of goodwill. Investors invest money only to earn an income and the size of the income determines what they will pay for the asset concerned. The cost of the asset to the previous proprietor does not matter at all. The market value of a house does not depend on its cost but on the rent fetched by it.

Suppose a business is for sale and proprietor demands Rs 10,00,000 for the tangible assets and another Rs 4,00,000 for goodwill, the profit earned in that business being Rs 1,00,000 per year; no one will pay anything for goodwill if a new, similar, business started with Rs 10,00,000 will also yield Rs 1,00,000 profit.

Goodwill is paid only for the extra profits. If, in the above example, the actual profits were Rs 1,40,000 whereas a new business would earn with the same capital only Rs 1,00,000, goodwill will arise in respect of the extra Rs 40,000 profits.

One who pays for goodwill can look only to the future profits. Hence, the business will be thoroughly examined to see what special advantages it is in possession of and which of them are likely to continue with the change in ownership and passage of time. The attempt is to establish the future maintainable profits.

The following are the important factors that have a bearing on future profits, and therefore, the value of goodwill:—

(a) Personal Skill in Management:

Reputation is built up by the skill displayed in management. Admittedly, in certain cases skill in management is much more important than in others. For example, a firm of architects, solicitors or chartered accountants depends much more on the skill possessed and reputation enjoyed by the proprietors for success than does a textile mill.

If the success of the firm whose goodwill is being valued depends on senior officials, continued service of such official is a point to remember. If they are unwilling to serve under new ownership, the value of goodwill cannot be much. For instance, if a newspaper has been built up by the editor and if the editor is unwilling to serve the new masters, the newspaper will suffer by the resignation and the continued success of the paper will not be assured.

(b) Nature of Business:

This covers many things. If it is difficult to enter an industry existing firms will enjoy a measure of goodwill by the mere fact of existence. Difficulties may arise, for proposed new entrants, due to the market having reached its saturation point or due to unduly heavy expenditure on fixed assets or due to legal difficulties. It is very difficult, due to exchange regulations and Import Control, for a new firm to enter import business. Existing firms therefore will command goodwill which in ordinary times they would not. If a firm enjoys monopoly or near monopoly conditions, it also enjoys goodwill but not if the monopoly is due to case.

(c) Favourable Location or Site:

It is well-known that certain cities or places are most suitable for particular industries and that in a city certain localities offer the most advantageous positions for particular trades. For example, in Delhi, Nai Sarak has acquired a reputation for being centre of the text-book trade.

Existing shops, therefore, have an advantage which can be converted into cash by selling the goodwill. If ample space were available for newcomers, there would be no goodwill on account of location. Goodwill arises only because the newcomers find it hard to rent premises.

(d) Access to Supplies:

In these times of raw material shortages, a firm enjoying a favourable position regarding supplies of materials will possess goodwill. A firm holding large quotas for import of goods will be able to realise good money for goodwill as long as import restrictions continue. Favourable contracts with monopolist suppliers will have the same effect unless the contract is due to expire and is not likely to be renewed.

(e) Patents and Trade Mark Protection:

In most industries ownership of patents is necessary in order to carry on production. A firm enjoying the right to use the most valuable patents will have a valuable goodwill.

If a firm has built up good reputation for its products by means of a trade mark, its possession will bring good profits and, therefore, goodwill will be worth a large sum of money. Similarly, a firm of publishers having good copyrights will enjoy goodwill but not if the copyrights are due to expire or if the book does not sell much.

(f) Exceptional Contracts:

Exceptionally favourable contracts for supply of goods or services to the customers will also raise the value of goodwill. If, however, the exceptional contracts were obtained only due to the personal skill and influence of the previous owner, and it is unlikely that such contracts will be obtained in future, the value of goodwill will not be influenced by such existing contracts.

Pending contracts of recurring nature and likely to result in substantial profits will enhance the value of goodwill.

(g) Capital Requirements and Arrangement of Capital:

The amount of capital required will have much influence on the value of goodwill. If the capital required is large, considering the profits likely to be available, the value of goodwill will be small. If the business is highly profitable and the capital invested is relatively small, a high value may be placed on goodwill.

In this connection, the sources of funds may have influence on profits available for equity shareholders. Suppose, there are two companies, A and B, both making a profit of, say Rs 2,00,000 a year and both requiring Rs 10,00,000 to produce the profit.

Suppose further, that A’s capital consists only of equity shares, whereas B has raised Rs 2,00,000 by issuing 12% debentures, Rs 3,00,000 by issuing 14% preference shares and Rs 5,00,000 by issuing equity shares.

The profits available for equity shareholders (who have the real stake in the profits of the companies) are as follows:

Obviously, those who own equity shares in company B are favourably placed compared to the equity shareholders in company A. In other words, the existence of fixed interest or dividend bearing capital is advantageous to the equity shareholders if the profits are large.

This advantage may have to be considered for valuation of the goodwill if the purchasing company continues to have advantage of the fixed interest or dividend bearing capital. But if the profits are small, the existence of such capital will have a depressing effect on the value of goodwill.

If the profit is large, but if the debentures or preference shares have to be redeemed on transfer of ownership, there is no advantage left for the purchasing company and hence the value of goodwill will be correspondingly less.

The logic behind the argument is that one can acquire control over the whole company by purchasing the majority of equity shares and that profit, after debenture interest and preference dividend have been paid, all belong to equity shareholders. Equity shareholders are, therefore, the main beneficiaries of any special advantage that a company enjoys.

It may be seen that a company may not be specially profitable (for example, company B in the example given above) and, therefore, not entitled to any goodwill as such. But, if, due to capital gearing arrangements, equity shareholders get a dividend higher than in other companies they will have a valuable right to be valued in terms of goodwill.

Note:

It may be argued that in an industry a particular proportion of total funds required is likely to be raised by way of preference shares or debentures. Therefore, there may be no advantage to a company in this respect. In fact, a company which departs from the norms prevailing in the industry concerned is not looked upon with favour by investors.

Further, even if a company does have an advantage in the form of trading on equity, it is likely to be temporary. Therefore, it would be better not to attach too much weight to this point.

It would be proper to consider the profitability of the company, considering profit earned (before interest and dividends but after tax) and total capital employed. However, the opinion so far is to exclude loans and debentures from capital employed and consider profits after interest.

The approach in this book will be to treat capital employed as equivalent to shareholders’ funds, preference or equity, and consider profits available to shareholders. The influence of all the factors discussed above works out in the figure of profits.

These figures should be carefully examined to see how much of the profits are likely to be realised in future also, since (to repeat) the purchaser pays for goodwill on the expectation of earning good profits in the future.

If in the past good profits have been earned due to:

(a) The personality of the previous owner,

(b) The particularly favourable situation which is likely to be lost,

(c) Short-lived monopoly conditions, or

(d) A temporary craze or fashion, there will be no value attached to goodwill.

Future Maintainable Profit:

It has been stated above that it is the future profits, likely to be earned, that are relevant for valuing goodwill. This is quite correct but the estimate for future profits will obviously be made on the basis of past profits.

While estimating the future profits on the basis of past profits the points to be remembered are as under:

(i) All usual working expenses including interest to debenture-holders and depreciation of the assets of the company should be provided for. If the fixed assets have to be revalued, depreciation should be based on the values arrived at as a result of the revaluation,

(ii) All necessary provisions for liabilities for, say, taxation or otherwise should be made. But transfer to general reserves, dividend equalization fund, or sinking fund for redemption of liabilities should not be taken note of, as such transfers merely transfer profits from one account to another, and the availability of profits is not affected,

(iii) In case non-trading assets have been excluded from the capital employed, the income derived from such assets should be excluded,

(iv) Profits for the past four or five years (during which conditions have remained normal) should be averaged since the average is more reliable than a single year’s profit.

(v) Developments which have already taken place but whose results are likely to come in the future should be taken into account.

The whole idea is to arrive at a figure of profits which can be expected to be maintained in future.

Illustration 1:

Calculate Future Maintainable Profit for the year ending March 31, 2012 and the additional information:

Weighted average is = Rs 8,35,000 thousand/15 = Rs 55,667 thousand

One should not follow the practice suggested above, if there is a marked and continuous decline of profits. In that case, profits for the future should be estimated on the basis of the trend—they will be lower than the profits for the latest year.

6. Expected Developments:

Results of development that have taken root, but are likely to bear fruit in future should be estimated and the past profits should be adjusted for this factor in order to arrive at the future maintainable profit. Suppose, as a result of research and development work in the past, a new product will soon be launched.

The investment on this project should be added to capital employed and the expected profit to the estimate for future maintainable profit otherwise arrived at.

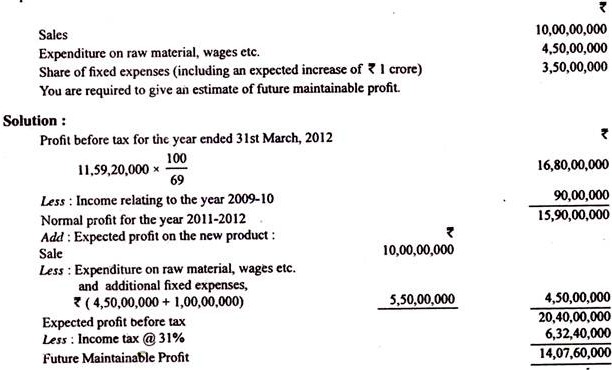

Illustration 2:

For the year ended 31st March 2012, a company reported a profit of Rs 11,59,20,000 after paying income tax @ 31%. It was found that the year’s income included Rs 90 lakh for a claim lodged in 2009-10 for which no entry had been passed then. As far as trading conditions are concerned 2011-2012 was a normal year.

The company expects to launch a new product and estimates in this respect are as follows:—

Illustration 3:

Why Ltd. Shows the following summarised investment in its operations:

The nature of the industry is such that the plant, being of a sturdy nature, gives uniform service from year to year. The company makes a sale of Rs 1,00,000 normally per annum and earns a profit of Rs 20,00,000 before tax, the fixed expenses being 25% of the total cost.

Tax is paid @ 30%. Finding the sales to be good and the market expending, the company installs new plant costing Rs 30 lakhs, 1/6 of the cost being due to price increases since the installation of the old plant. Increase in fixed expenses due to the new plant will be 16,00,000. Prepare an estimate of the future maintainable profit.

7. Yield Expected by Investors from Valuation of Goodwill:

In valuation of goodwill, the expectation of investors plays an important role since it is this expectation that determines the normal level of profits. It is also called the average rate of return or the “normal rate of return”.

It means that return which will satisfy an ordinary investor (not very reluctant or eager to invest) in the industry concerned. Such a rate of return differs from one class of investment and business to another.

An investor in government securities may feel satisfied with 10% yield on his outlay; he may expect, say, 20% if he invests in equity shares of a new company but, in case the company is old and well established, he may be content with only 18%.

Stock exchange quotations usually give a good indication of expectations of investors. If a share on which a dividend of Rs 25 is paid and is expected to be paid sells for Rs 125 the investors expect an yield of 20%, i.e., 25/125 x 100.

Such a rate will be relevant to only the usual transactions on the stock exchange. It will have to be modified in view of the fact that valuation of goodwill envisages the transfer of a whole business or the majority of equity shares. Power itself being an advantage, the purchaser will have to pay for it by accepting a lower rate of return.

The yield expected by investors consists of three components:

(i) The pure interest — the interest which one can earn by parting with his funds without in any way incurring any risk, e.g., by buying government securities;

(ii) The business risk — a margin to cover to ordinary risks attendant in business; and

(iii) The financial risk—a margin to cover risks connected with the finances of the firm concerned.

If the pure interest is 12%, an investor in the shares of a company may want to add, say, 5% for ordinary business risks and 3% for the risks special to the company concerned — say, 20% in all.

The factors that affect the normal rate of return are the following:—

(i) The degree of risk attending investment—the risk may be because of the nature of the industry or of the situation in the company such as too much dependence on loans or debentures;

(ii) The period for which investment is to be made — longer the period, higher the expected rate of return;

(iii) The bank rate — any increase in the bank rate will lead to an all-round increase in expectation of investors; and

(iv) General economic and political situation—in case confidence is shaken there will be a sharp rise in the rate of return expected by investors. A boom, however, also may have the same effect because of a desire to share in the prosperity.

8. Capital Employed for Valuation of Goodwill:

This is the third most important factor in valuation of goodwill, since the size of profits is significant only in relation to the capital used to earn it. Capital employed is now recognised to mean fixed assets (less depreciation written off) plus net working capital (that is, current assets minus current liabilities).

This may also be expressed as aggregate of share capital, reserves and long-term loans. Non-trading assets, that is, assets acquired because of spare funds such as government securities, are excluded. Assets that must be acquired even if they are in the nature of shares, debentures, etc., cannot be treated as non-trading.

The above mentioned idea of capital employed, however, is not suitable for the purpose of valuing goodwill of individual companies where it is essentially the advantage accruing to the shareholders which has to be evaluated.

For this purpose, the amount of debentures or loans should also be excluded from capital. (Of course, the profit considered for valuation of goodwill will also be after interest on debentures and loans obviously goodwill is also excluded.)

An important point to note is the change in the value of fixed assets if these were acquired some years ago. Since profits are expressed in terms of current prices, it is proper that fixed assets should also be valued at current prices.

A refinement is that the figure of capital employed should be the average for the year concerned since the figure changes at least because of the profit or loss during the year.

Illustration 4:

The following is the balance sheet of Kajaria Ltd. as at 31st March, 2012:—

Except for fresh capital, capital employed increases over a year mainly due to profits earned. If the capital employed in the beginning is Rs 15,00,000 and the figure increases to Rs 17,00,000 by the end of the year, the reasonable presumption is that during the year a profit of Rs 2,00,000 has been earned.

In this example, the average capital employed is Rs. 16,00,000, which figure can also be obtained by deducting from Rs 17,00,000 half of the profit, viz., Rs 1,00,000 (or adding Rs 1,00,000 to the capital in the beginning).

Thus if the capital employed in the beginning of the year is not given, average capital employed can be ascertained by deducting half the profits of the year from the capital employed at the end of the year.

The assumption is that profits have been earned evenly over the year—that by the middle of the year half the profits were earned and thus used in business and that the profits have not yet been distributed. “Proposed Dividend” out of current year’s profits, if it appears in balance sheet, should be treated as part of profits for this purpose.