In England the holding company is required to present, in addition to its normal balance sheet, a consolidated balance sheet covering the holding company and its subsidiaries and a consolidated profit and loss account.

In India, the law does not insist on consolidated accounts but there is no doubt that for a clear picture, it is desirable to present one single balance sheet of the holding and subsidiary companies and a single profit and loss account. Before the rules for consolidation are discussed, it is necessary to see how dividend received from the subsidiary is treated in the books of the holding company.

Treatment of Dividend:

It has been pointed out above that the profits already earned and accumulated by the subsidiary company, up to the date of acquisition of the shares by the holding company, are capital profits. If shares are acquired during the course of a year, the profit should be treated as accruing from day to day (in the absence of any other indication) and, therefore, should be apportioned on the time basis.

ADVERTISEMENTS:

Take the following example:

Rs 15,000, that is, three months’ profits (after 1st January, 2012) will be revenue profit; all trading profits earned after 1st January, 2012 will be revenue profits.

The distinction between capital profits and revenue profits is most important from the point of view of the holding company. Dividends received out of capital profits must be credited to “Investment Account” since the cash received is against the price of shares paid at the time of the acquisition.

ADVERTISEMENTS:

Only dividends received out of revenue profits can be treated as income and credited to the Profit and Loss Account. Study the following example:

On 1 St November, 2011, H Ltd. acquired 30,000 equity shares of Rs. 10 each (at a cost of Rs 15 per share) in S Ltd. whose total share capital consisted of 50,000 equity shares of Rs 10 each, fully paid.

The balance in the Profit and Loss Account of S Ltd. on 31st March, 2012 was Rs 4,40,000 made up as:

Since H Ltd. holds 30,000 shares out of 50,000, three-fifths of the profits belong to H Ltd. Hence, capital profit, as far as H Ltd. is concerned, is three-fifths of Rs 3,15,000 or Rs 1,89,000; Revenue Profit, as far as H Ltd. is concerned, is Rs 75,000. Total dividend received by H Ltd. is 40% on Rs 3,00,000 or Rs 1,20,000. The question now arises : which profit has been utilised first to pay the dividend?

ADVERTISEMENTS:

There are four possibilities:—

1. The dividend has been paid first out of latest profits and then out of the previous profits.

2. The profits of the current year as a whole have been used first to pay the dividend.

ADVERTISEMENTS:

3. The dividend has been paid first out of previous profits and then out of current profits.

4. The two profits have been utilised proportionately. The journal entries to be made in each of the cases are:

There will be no entries in the books of H Ltd. for the receipt of bonus shares, since no extra payment has been made and the possibility of a gain is uncertain.

ADVERTISEMENTS:

Note: In the absence of information, one should assume that the dividend is out of the profits for the year for which the dividend is being paid.

A Ltd. purchased 16,000 shares in B Ltd. on 1st April, 2011, and another 2000 shares on 30th November, 2011. The share capital of B Ltd. is Rs 2,00,000 divided into shares of Rs 10 each.

The company had Rs 1,20,000 to the credit of Profit and Loss Account on April 1,2011, and earned a profit of Rs 75,000 during the 2011-2012 out of which in March, 2012 it paid a dividend of 15%. How should A Ltd. treat the dividend received and what is its share of capital profits?

ADVERTISEMENTS:

The dividend received by A Ltd. will be Rs 27,000 – Rs 24,000 for 16,000 shares bought on April 1, 2011 and Rs 3,000 for 2000 shares bought on November 30, 2011. Out of the latter amount, eight months’ dividend, Rs 2,000, is capital receipt and hence should be credited to Investments Account. The remaining amount of Rs 25,000 is revenue income to be credited to the Profit and Loss Account.

The capital profit as regards A Ltd. is Rs 1,20,000 the balance on 1st April, 2011. Since 90% shares are held by A Ltd., Rs 1,08,000 is the share of A Ltd. Further, out of the profits earned in 2011-2012, Rs 45,000 remains after dividend. Out of this eight months’ profit in respect of2000 shares purchased on 30.11.2011 is also capital profit; the amount is Rs 3,000. Hence, total capital profit for A Ltd. is Rs 1,11,000.

Debiting the Subsidiary with Profits, etc.:

If the holding company holds the entire share capital in the subsidiary company, it would be possible to treat the subsidiary as a debtor for profits earned by it; to do so, it should debit the “Subsidiary Company (Profits) Account” and credit “Profits and Losses of Subsidiaries Account” or “Subsidiary Companies’ Revenue Account”. The entry in case of a loss is just the reverse of it.

ADVERTISEMENTS:

The “Subsidiary Company (Profits) Account” is in the nature of a personal account. This account is opened to distinguish it from the usual account with the subsidiary. When dividend is received, cash is debited and the “Subsidiary Company (Profits) Account” is credited.

The balance in the account will represent what the subsidiary company owes to the holding company in respect of profits earned by it. “The Profits and Losses of Subsidiaries Account” is closed by transfer to the holding company’s profit and loss account.

The law does’ not require a holding company to follow the practice outlined above. And the practice is also not desirable from the accountancy point of view. But it would be quite proper for the holding company to make a provision in its books for its share of the loss suffered by its subsidiary ‘or subsidiaries.

Illustration 1:

H Ltd. holds the entire share capital of S Ltd. which made a loss of Rs 50,000 in its first year and a profit of Rs 1,10,000 in its second year. In the second year S Ltd. paid a dividend of Rs 40,000. Show journal entries in the books of the holding company assuming that the latter company brings into account all the losses and profits of the subsidiary company.

Preparation of Consolidated Balance Sheet:

ADVERTISEMENTS:

The basic point to understand in the preparation of consolidated balance sheet is that the shares in the subsidiary company held by the holding company represent the assets and liabilities of the subsidiary company. Shares are ownership securities.

Suppose H Ltd. owns 100% shares of S Ltd. we may as well say that H Ltd. owns 100% of the net assets i.e., the assets and liabilities of S Ltd. The consolidated balance sheet shows, instead of the shares of the subsidiary company, the net assets of the subsidiary company in addition to those of holding company.

Illustration 2:

H Ltd. acquires all the shares of S Ltd. on 31st March, 2012 on which date the balance sheets of the two companies are as under:

Solution:

100% shares in S Ltd. represent assets of Rs 2,60,000 minus the liabilities of Rs 60,000. Hence, while preparing the consolidated balance sheet of H Ltd. and S Ltd. the assets and liabilities of both the companies will be added; the share capital of S Ltd. being cancelled against ‘Shares in S Ltd.’ shown as an asset by H Ltd. The consolidated balance sheet will appear as under:

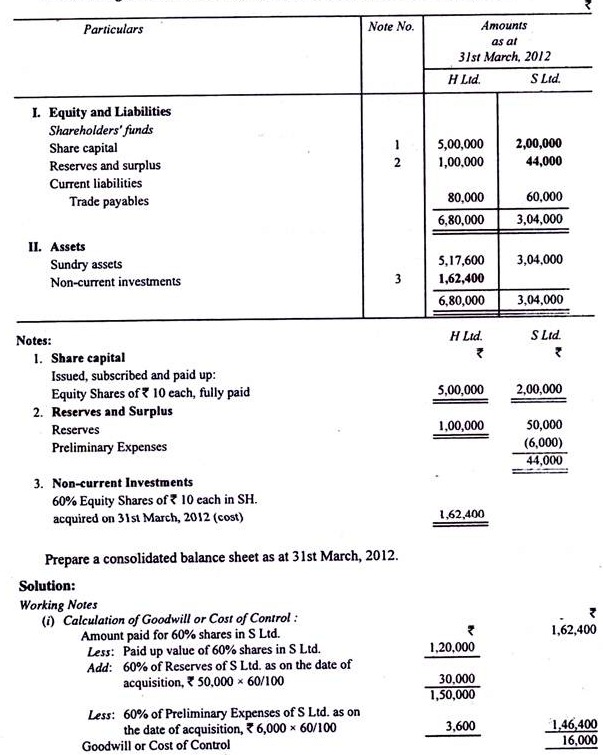

Cost of Control/Capital Reserve:

In the abovementioned example, the shares held by H Ltd. represent S Ltd.’s net assets of Rs 2,00,000 and H Ltd. acquires the shares for exactly Rs 2,00,000. But H Ltd. may pay for the shares an amount which either is more or is less than Rs 2,00,000. If it pays more, the excess amount paid is considered the payment for goodwill or cost of control.

On the other hand if H Ltd. pays less than Rs 2,00,000 the excess of S Ltd.’s net assets (excluding Goodwill) out the cost of shares to H Ltd. is a capital profit and is shown as Capital Reserve in the consolidated balance sheet.

Illustration 3:

The following are the balance sheets of H Ltd. and S Ltd. as at 31st March, 2012:

Illustration 4:

The following are the balance sheets of H Ltd. and S Ltd. as at 31st March, 2012:

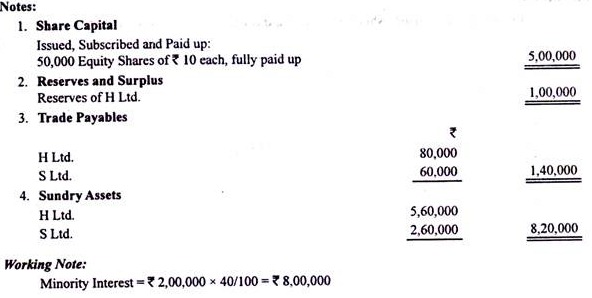

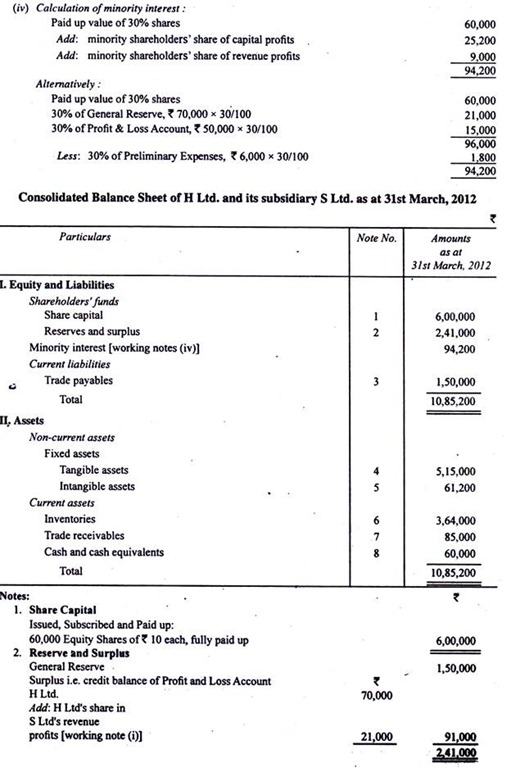

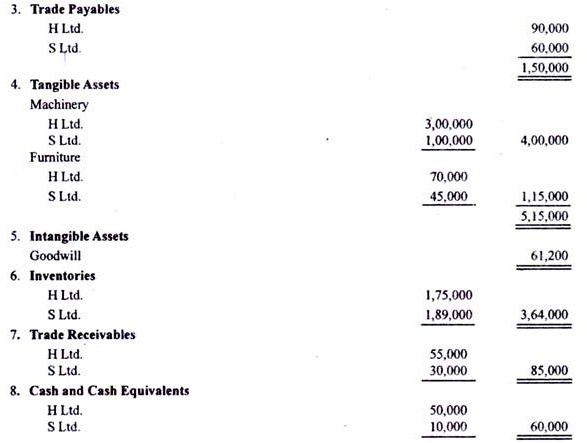

Minority Interest:

The holding company may not hold 100% shares of the subsidiary company. In other words, the subsidiary company may not be wholly owned by the holding company.

Suppose H Ltd. purchases only 70% of the shares in S Ltd. the remaining 30% shares continuing to be held by outsiders S Ltd. thus becomes a partly owned as opposed to wholly owned subsidiary with a minority interest of 30%. In the consolidated balance sheet, the fact that H Ltd. owns S Ltd. partly has to be reflected.

In theory two possible approaches could be:

(1) To include 70% of the respective items i.e. inventories, trade receivables, cash balances, trade payables etc. relating to S Ltd., or

(2) To include 100% of all such items and show 30% outside ownership on the liabilities side as a compensating adjustment.

In actual practice, the second approach is adopted. Thus even when the subsidiary company is only partly owned, the method of consolidation is to include in the consolidated balance sheet, the whole of the assets and liabilities of the holding and subsidiary companies i.e. both the proportion owned by the holding company and the proportion attributable to the shareholders other than the holding company who are known as minority shareholders.

The interest of the minority shareholders in the net assets of the subsidiary company is registered and shown as ‘Minority Interest’ on the liabilities side of the consolidated balance sheet.

Illustration 5:

The following are the balance sheets of H Ltd. and S Ltd. as at 31st March, 2012:

Illustration 6:

The following are the balance sheets of H Ltd. and S Ltd. as at 31st March, 2012:

Illustration 7:

The following are the balance sheets of H Ltd. and S Ltd. as at 31st March, 2012:

Illustration 8:

The following are the balance sheets of H Ltd. and S Ltd. as at 31st March, 2012:

Illustration 9:

The following are the balance sheets of H Ltd. and S Ltd. as at 31st March, 2012:

Illustration 10:

The following are the balance sheets of H Ltd. and S Ltd. as at 31st March, 2012:

The minority shareholders are also entitled to their proportionate share of the profit and reserves of the subsidiary company and have to bear their share of losses suffered by the subsidiary company. Thus the minority interest is increased by the profits and decreased by the losses of the subsidiary company.

Illustration 11:

The following are the balance sheets of H Ltd. and S Ltd. as at 31st March, 2012:

Illustration 12:

The following are the balance sheets of H Ltd. and S Ltd. as at 31st March, 2012:

Capital Profits and Revenue Profits:

So far profits and losses of the subsidiary company pertaining to pre-acquisition period only have been dealt with; they are capital profits and losses for purposes of preparation of consolidated balance sheets. It must be understood that the term ‘capital profit’ in this context, apart from the generic meaning of the term, connotes profit earned by the subsidiary company till the date of acquisition.

As a result, profits which may be of revenue nature for the subsidiary company may be capital profits so far as the holding company is concerned. Profit arising out of appreciation of fixed assets on their revaluation even in the post-acquisition period is also a capital profit and is treated like profits pertaining to reacquisition period.

The profits earned and losses incurred by the subsidiary in the post-acquisition period are treated as revenue profits and revenue losses respectively. Holding company’s share of such profits and losses are shown in the consolidated balance sheet as increase or decrease as the case may be in Profit and Loss Account.

Minority shareholders’ share of post-acquisition profits increases the minority interest and their share of post-acquisition loss decreases the minority interest.

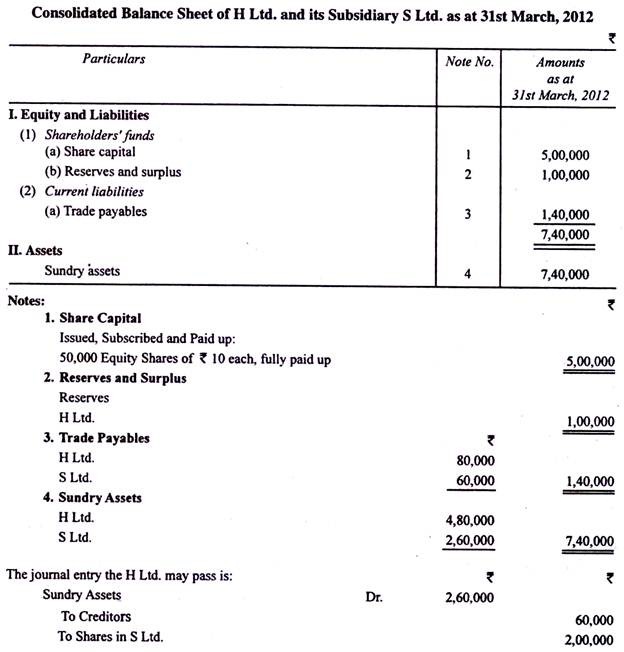

Illustration 13:

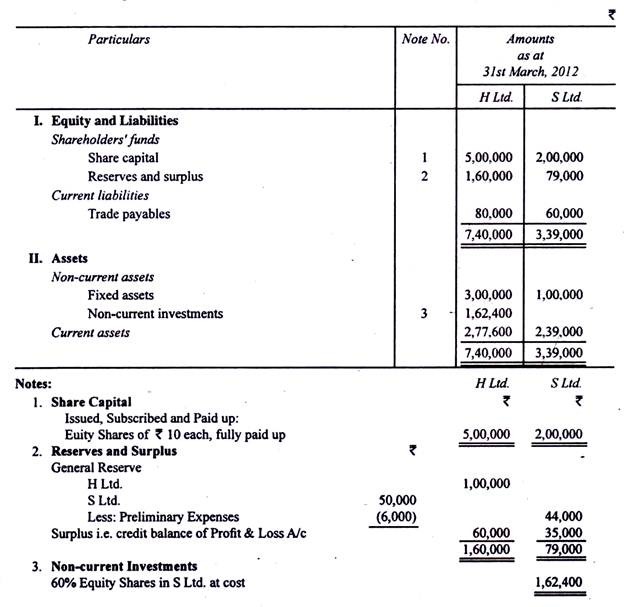

The following are the balance sheets of H Ltd and S Ltd. as at 31st March, 2012:—

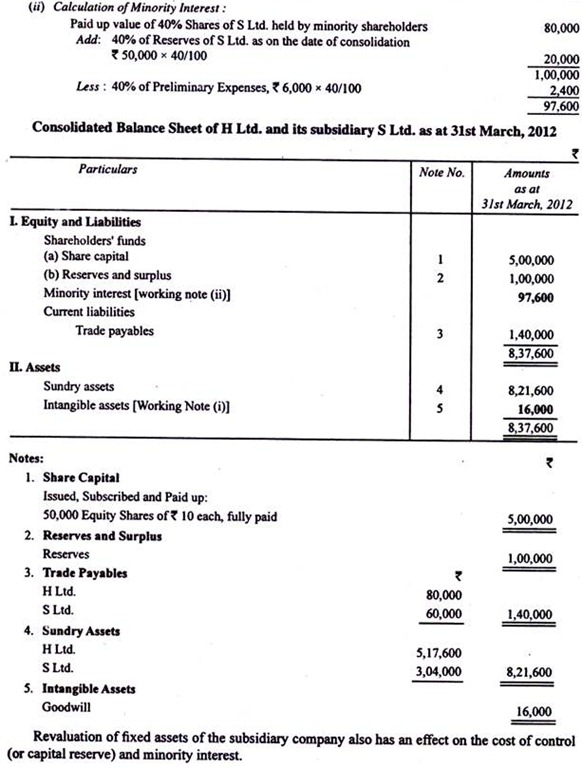

H Ltd. acquired the shares on 1st April, 2011 on which date General Reserve and Profit and Loss Account of S Ltd. showed balances of Rs 40,000 and Rs 8,000 respectively. No part of Preliminary Expenses was written off during the year ending 31st March, 2012.

Prepare the consolidated balance sheet of H Ltd. and its subsidiary S Ltd. as at 31st March, 2012.

Illustration 14:

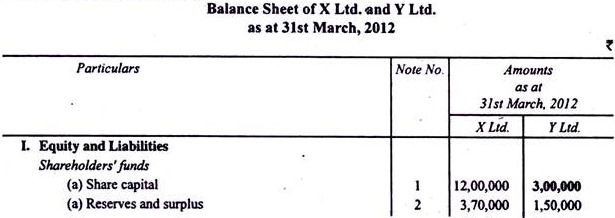

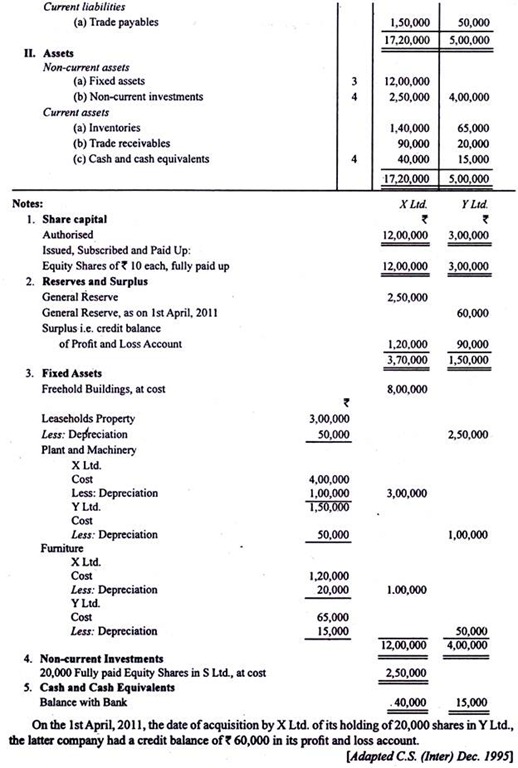

From the balance sheets given below, prepare a consolidated balance sheet of X Ltd. and its subsidiary Y Ltd. The interest of minority shareholders in Y Ltd. is to be shown as a separate item in the consolidated balance sheet.

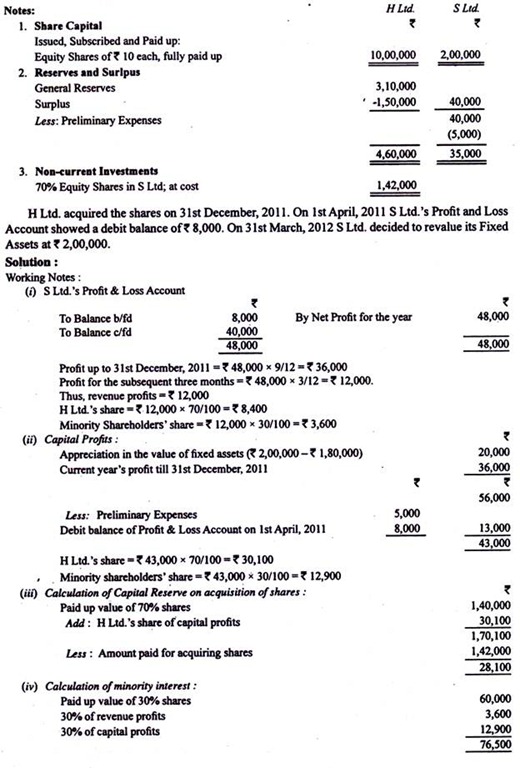

Controlling Interest Acquired During the Course of the Year:

Holding Company may not acquire shares of the subsidiary company on a date on which the subsidiary company prepares its final accounts.

It may acquire shares in the course of a financial year; in such a case all reserves and the profit and loss account balance up to the beginning of the year will naturally be capital profits, but, in addition, current year’s profit up to the date of acquisition will also be treated as capital profits.

In the absence of any indication to the contrary, profits should be treated as accruing from day to day, that is to say, the apportionment should be made on time basis.

Illustration 15:

The following are the balance sheets of H Ltd. and its subsidiary S Ltd. as at 31st March, 2012:

Illustration 16:

From the following balance sheets of H Ltd. and its subsidiary S Ltd. as at 31st March, 2012 and the additional information provided thereafter, prepare a Consolidated Balance Sheets of the two companies as at that date: