The below mentioned article provides an overview on activity based costing.

The Cost Accounting includes collecting, classifying, processing, analyzing and reporting of information to managers in their planning and control of activities and information system to be developed to help in decision making within the firm. Traditional accounting focused on product costing by tracing direct costs to the product and indirect costs are allocated through cost centres.

The direct costs will be in proportion to the volume of production and the indirect costs like production, administration, marketing and distribution overheads etc., are apportioned depending upon the method used and absorbed to the individual product.

The basis of apportionment of overheads may be based on machine hours, labour hours, direct costs, input, output, etc. These normal methods of apportionment have some bottlenecks which tend to misinterpret regarding proration of common costs of different functions added to the product cost.

ADVERTISEMENTS:

The conventional cost systems use direct labour consumption as the primary means of apportioning overhead. This proved adequate when the overhead costs of indirect activities was a small percentage compared to direct labour consumption in actual making of products.

The increased technology and automation has reduced the direct labour substantially, leaving indirect activities as a far more significant cost factor. Therefore, using direct labour as a primary apportioning device can cause significant costing distortions and poor strategic planning. The cost information is normally reported too late to support improvement efforts and it is not reported by activity.

The incorrect cost information can lead to face the following dangers:

(a) Emphasizing and focusing on wrong products, wrong customers, wrong markets.

ADVERTISEMENTS:

(b) Neglecting and missing profitable opportunities.

(c) Design of products that unnecessarily raise costs.

(d) Moving of production to other places, which will increase cost instead of decrease in costs.

(e) Customer orientation is neglected.

ADVERTISEMENTS:

(f) Acquisition of wrong type of equipment.

(g) Centralization of cost control activities and adoption of cost cutting programs.

Inadequacies of Traditional Cost Systems:

The cost of product under traditional cost system is not accurate due to following reasons:

ADVERTISEMENTS:

(a) The conventional costing system has developed convenient overhead recovery basis and blanket overhead recovery are acceptable when valuing stocks for financial reporting, but they are inappropriate when used for decision making and typical product strategy decisions. Such decisions have implications over 3-5 years and over this period many fixed costs become variable.

(b) The traditional fixed verses variable cost split is often unrealistic since, as business grows they often become more complex.

(c) In case of companies manufacturing and selling multiple products usually make decisions on pricing, product mix, process technology etc., based on distorted cost information due to difficulties in traditional costing system in collection, classification, allocation and recovery of overheads to individual products.

(d) The cost structure is changing especially when making direct labour component to small proportion.

ADVERTISEMENTS:

(e) Traditional accounting was confined merely to furnishing information at product level. The new manufacturing technology demands the feedback of performance while production is still in progress rather than history.

(f) There is also an urgent need to integrate the activity measurement and financial measurement.

Therefore, in order to overcome the inadequacies of traditional methods of absorption of indirect costs and short-term biasing of marginal costing, activity based costing (ABC) has been researched.

The new global competitive environment has caused to redesign the traditional manufacturing systems into world-class company by adopting new ways of conducting business, new ways of measuring performance and striving for improvement in all aspects of a company’s business. The goal of a world-class company is to profitably meet the needs of its customers.

ADVERTISEMENTS:

Therefore, the cost system in a world-class company should enable:

(1) Customer orientation of cost information.

(2) Reveal the profitability of customers and products.

(3) The reasonableness of costs to be incurred for generating cost information.

ADVERTISEMENTS:

(4) Identifies the opportunities for improvement.

(5) Enable to meet customers’ expectations profitably.

(6) Encourages the continuous improvement

Meaning and Objectives of ABC:

Definition and Meaning:

CIMA Official Terminology defines Activity Based Costing (ABC) as “cost attribution to cost units on the basis of benefit received from indirect activities e.g., ordering, setting-up, assuring quality”. ABC has been defined as “the collection of financial and operational performance information tracing the significant activities of the firm to product costs”.

Professors Kaplan and Cooper of Harward University has pioneered the ABC concept. ABC is an attempt to ascertain more accurate product cost by redesigning the allocative system of support overheads like inspection, despatch, production planning, setup, tooling and similar costs. ABC is a recent development in Cost Accounting which attempts to absorb overheads into product costs on a more realistic basis.

ADVERTISEMENTS:

Supporters of the technique argue that many costs are unnecessarily treated as common costs and are arbitrarily absorbed using a basis such as direct labour hours, machine hours, etc. Many organizations have now adopted Advanced Manufacturing Technology (AMT) with the result that overheads are increasing and labour costs are becoming a smaller portion of total costs.

Costing systems which absorb overheads on a direct labour basis are therefore, not relevant in an AMT environment. The basic idea of ABC is that costs are grouped according to what drives them or causes them to be incurred. The cost drivers are then used as an absorption base.

ABC is the method of cost attribution to cost units on the basis of benefits received from indirect activities i.e., ordering, setting-up, assuring quality etc. It emphasizes links between performance of particular activities and the demands that these activities make on the resources of the organization. Methodology in allocation of overhead is different in ABC system.

Under ABC, cost pools are created for each activity and such activities are related with each type of product to determine the cost of such product i.e. cost of only those activities are charged to the product which go in the making of the product.

The technique of ABC involves identification of production path, identification of activities that go into making a product, selection of suitable drivers, creation of cost pools, calculating the overhead application rate and allocation of the costs based on the application rate.

ABC is a method of measuring the cost and performance of activities and cost objects, assigns cost to activities based on their use of resources and assigns cost to cost objects based on their use of activities. ABC recognizes the causal relationship of cost drivers to activities. ABC is a method of measuring the cost and performance of activities, products and customers.

In product costing applications, ABC allows costs to be apportioned to products by the actual activities and resources consumed in producing marketing, selling, delivering and servicing the product. The ABC system aims to overcome the drawbacks by cutting across conventional departmental boundaries. Costs are grouped into ‘pools’ according to the activities which drive them.

The activity cost driver rates are identified as a means of tracing the cost of each activity to the product cost. ABC lays importance on different costs for different purposes and the identification of those costs which are relevant to a particular decision. The product costing using ABC is shown in figure 10.3.

Objectives of ABC:

The primary objectives of ABC systems are as follows:

(1) To improve the accuracy of product costs by carefully changing the type and number of factors used to assign costs, and

(2) To use this information to improve product mix and pricing decisions.

The other important objectives of ABC systems are summarized below:

(a) To identify value-added activities in transactions.

(b) To chalk out ways to eliminate non-value added activities.

(c) To attach costs in response to the price resistance demonstrated by customers.

(d) To distribute overheads on the basis of activities.

(e) To validate the success of the quality drive with ABC.

(f) To ensure accurate product costing for decision-making process.

(g) To provide high quality information about activities, customers, non-manufacturing activities.

(h) To focus the high-cost activities.

(i) To identify the opportunities for improvement and reduction of costs.

(j) To recognize the opportunities for profitably shifting the focus toward more profitable products, services and customers.

Steps in ABC System:

The activity based cost system is summarized in the following steps:

Step 1: Process Specification:

This involves identification of different stages of the production process, the commitment of resources to each processing times and bottlenecks. This will provide a list of transactions, which may, or may not, be defined as ‘activities’ at a subsequent stage.

Step 2: Identify Main Activities:

The next step in ABC system is to identify the main activities in the organization. An aggregate of closely related tasks is called an ‘activity’. For example, customer processing activity involves a series of acts like receiving orders from customers, interacting with production regarding capacity to produce, giving commitment to the customer regarding delivery time etc.

Thus any activity can comprise of one or more of tasks which are associated with one another to accomplish a goal or objective. Examples include: materials handling, store keeping, purchasing, inspection, dispatch, assembly, setup, maintenance and so on. This ensures aggregation or grouping of common activities and elimination of immaterial activities. Activities are categorized into primary activities and support activities.

Step 3: Identify Non-Value Adding Activity:

There are a large number of activities which continue to be carried out particularly in certain old factories, which do not contribute to the value of a product. The identification of non-value adding activities in the production process will help in focusing the attention for elimination.

Step 4: Identification of Activity Cost Pools:

CIMA official terminology defines Cost Pool as ‘the point of focus for the costs relating to a particular activity in an activity based costing system!. Under ABC, costs are grouped into pools, according to the activities which drive them e.g. a cost pool may be of procurement of goods, in this all costs associated with ordering, inspection, storing etc. would be included in this cost pool.

Cost pools are similar to cost centres in traditional cost systems. Costs are pooled or collected on the basis of activity that drives the costs regardless of conventional departmental boundaries. The activity cost pool is the total cost assigned to an activity. It is the sum of all the cost elements assigned to an activity.

Step 5: Selection of Activity Cost Drivers:

CIMA official terminology defines a Cost Driver as ‘any factor which causes a change in the cost of an activity e.g., the quality of parts received by an activity is a determining factor in the work required by that activity and therefore affects the resources required. An activity may have multiple cost drivers associated with it’.

The next step in ABC system is to identify the factors which determine the costs of an activity. These are called as ‘cost drivers’. Cost drivers are used to trace costs to products by using a measure of resources consumed by each activity. Cost drivers can be defined as those activities or transactions that are significant determinants of cost.

Cost driver is a factor that determines the work load and effort required of an activity and the resources needed. An activity may have multiple cost drivers associated with it.

Cost driver explains why an activity is performed and how much effort is extended to carry-out the work. Cost drivers are useful because they reveal opportunities for improvement. Working to reduce the negative effects of cost drivers can yield important gains in efficiency.

The following are examples of cost drivers:

(a) The number of purchase orders drives cost of the purchasing activity.

(b) The number of goods received notes drives the costs of material receiving activity.

(c) The number of items in stock drives the costs of warehousing.

(d) The number of sales invoices drives the costs of the sales, dispatch and sales ledger activities.

A cost driver is an activity which generates cost. ABC system is based on the belief that activities cause costs and that a link should therefore be made between activities and products by assigning cost of activities to products based on an individual products demand for each activity.

A single representative activity driver can be used to assign costs from the activity cost pools to cost objects. Such linking of total costs to cost objects is generally based on the activity driver rate.

Step 6: Tracing of Costs with Cost Objects:

Cost object is the final point to which costs are traced. The cost objects are linked to the objective of the organization. Cost object is the reason for performing an activity. Cost objects include products, services, customers, projects and contracts. The cost object enables to identify the activities required to produce products etc. Direct costs like materials and labour are easily assigned directly to cost objects.

The indirect costs are indirectly assigned to the cost object via cost pools and cost drivers. It involves the tracing of cost of activities to products according to a product’s demand for each activity. It requires to establish the demands made by a particular product on activities, using the cost drivers as a measure of demand. ABC is the process of tracing costs first from resources to activities and then from activities to specific products.

Step 7: Staff Training:

The cooperation of the work force is critical to the successful implementation of ABC. Staff training should be oriented to create an awareness of the purpose of ABC. The need for staff cooperation in the concerned team effort for mutual benefit must be emphasized throughout the training activity.

Step 8: Review and Follow-up:

The actual operation of the ABC system should be closely monitored. Periodic review and follow- up action is necessary for successful implementation of the system.

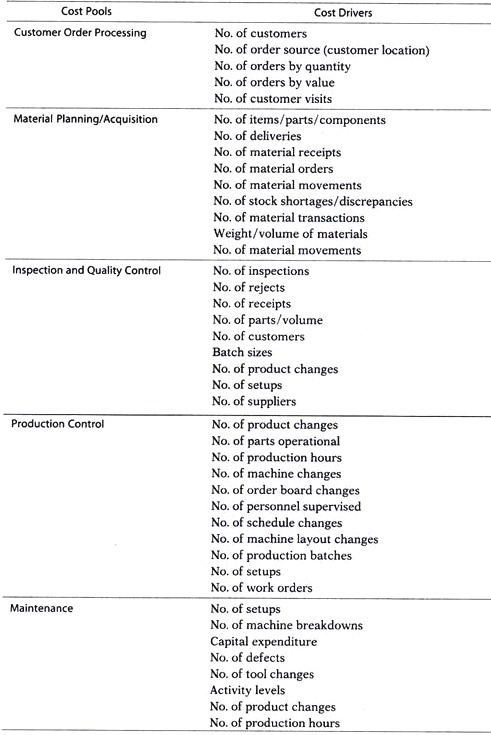

Different Categories of Cost Pools and its Cost Drivers:

The important Cost pools and its Cost drivers are given below:

Levels of Activity in ABC:

While implementing ABC, it is necessary to categorize the activities of the organization into:

(a) Unit level activities,

(b) Batch level activities,

(c) Product level activities, and

(d) Facility level activities.

(a) Unit level activities:

Some costs are incurred primarily in relation to production process and relationship can be established with the number of units produced.

Examples of such costs are:

1. Quality control costs

2. Cost of indirect materials

3.Cost of consumables

(b) Batch level activities:

Some costs are incurred at production level for the whole of the batch rather than for individual products.

Examples are:

1. Inspection of batch quality,

2. Machine setup costs, and

3. Material requisition for batch production.

(c) Product level activities:

Some costs are incurred for the introduction of new product line and its maintenance.

Examples are:

1. Product designing,

2. Manufacture of special parts, and

3. Advertisement cost for individual products.

(d) Facility level activities:

Some costs are incurred for the whole of the production facility which cannot be identified for any product line.

Examples are:

1. Factory building repairs and maintenance,

2. Security of the factory, and

3. Advertisement campaign for establishing company’s name.

Advantages and Limitations of ABC:

The reasons for support of ABC concept and criticism levelled against is summarized below:

Advantages:

(a) By adopting ABC, it is possible to ascertain most accurate and realistic product cost.

(b) The application of advanced manufacturing technologies and its resultant increase in support overhead can be easily traced with different products.

(c) It cuts across the traditional allocation, apportionment of overheads to different cost centres or departments. ABC emphasizes the identification of different activities and products are charged with portion of support overhead based on the consumption of activities.

(d) ABC helps in ascertainment of product cost based on both financial and non-financial information.

(e) ABC incorporates the concept of long-run variable product cost which is relevant to strategic decision making.

(f) ABC recognizes the cost behaviour and identifies the value added and non-value added activities.

(g) ABC is the most suitable method in tracing the costs of different product lines, customers, responsibility centres, locations etc.

(h) Management information system is strengthened with better and accurate information.

(i) It provides insight into elements of cost. Redundant costs can, therefore, be identified and remedial measures taken.

(j) Valuation of inventory requires assessment of cost rates. By the process of ABC, accurate cost rates can be determined. Accurate assessment of cost rate is a prerequisite for proper valuation of inventory and specially in the case of work-in-process.

(k) It helps managers in fixing of competitive selling prices.

(l) Information regarding capacity utilization is available for decision making.

(m) It helps in identifying and elimination of bottlenecks in the production for maximizing use of resources.

(n) It identifies non-value added activities, for effective control and maximizing margin.

Limitations:

(a) ABC is criticized for the following reasons.

(b) ABC is a complex system which consists of various cost pools and cost driver rates.

(c) ABC is beneficial to the complex and large organizations. For small organizations, traditional system is more economical and simple.

(d) Sometimes, the use of multiple cost drivers is necessary.

(e) Often it is difficult to attribute costs to single activities, some costs support several activities.

(f) ABC is based on the assumption that there is a direct and linear relationship between the usage of activities and application of cost driver rates.

(g) ABC system requires total commitment and support from top level management.

(h) It requires positive attitude and employees support for successful implementation.

(i) Substantial amount of money and time is necessary for implementation of ABC.

(j) Trained professionals, who are limited in number, are required for implementation of ABC system.

Other Concepts in ABC:

1. Activity Based Information and Decision Making:

ABC may not be appropriate for all companies, particularly those where overheads are relatively small and which do not produce a wide range of products. But many of the benefits of ABC can still be obtained by implementing a partial system which focuses only on the most important activities.

Traditional methods can be used for to produce monthly profit statements, leaving ABC to support strategic decision making, profitability analysis and the control of manufacturing costs.

ABC supports decision making in many ways such as:

(a) ABC system can effectively support the management by furnishing data, at the operational level and strategic level. Accurate product costing will help the management to compare the profits that various customers, product lines, brands or regions generate and to decide on pricing strategy, dropping unprofitable products, lines etc.

(b) Information generated by ABC system can also encourage management to redesign the products.

(c) ABC system can change the method of evaluation of new process technologies, to reduce setup times, rationalization of plant layout in order to reduce or lower material handling cost, improve quality etc.

(d) ABC system will report on the resource spending vis-a-vis resource consumption, and reduced demand in organizational resources lead to increase in profits.

(e) ABC analysis helps managers focus their attention and energy on improving activities and the actions allow the insights from ABC to be translated into increased profits.

(f) The cost driver rates established by the system can be used to measure activity performance and efficiency and provide a more suitable basis for budgeting.

(g) The accurate feedback can be provided to cost centre managers on their performance based on their consumption of resources during a period rather than the allocations of cost over which they have no control.

(h) The provision of accurate information on product costs enables better decisions to be made on pricing, marketing, product design and product mix.

2. Activity Based Budgeting:

Activity based budgeting (ABB), sometimes termed ‘activity cost management’, is a planning and control system which seeks to support the objective of continuous improvement.

It is a development of conventional budgeting system based on activity analysis. ABB requires the identification of the activities of the organization, establishing the factors which cause costs, the cost drivers, and then collecting the costs of the activities in cost pools.

ABB recognizes that:

(a) It is activities which drive costs and the aim is to control the causes (drivers) of costs directly rather than the costs themselves. In the long-run, costs will be managed and better understood and controlled.

(b) Not all activities add value, so it is essential to differentiate and examine activities for their value-adding potential.

(c) The majority of activities in a department are driven by demands and decisions beyond the immediate control of the budget holder. Conventional budgets, expressed in financial terms against established cost headings, ignore this casual relationship.

(d) More immediate and relevant performance measures are required than are found in conventional budgeting systems.

ABB provides stronger links between an organization’s strategic objectives and the objectives of the individual activities within a business for which departmental managers are responsible. Additionally, important strength of ABB is its ability to tackle cross-organizational issues by a participative approach and activity analysis techniques, all of which promote continuous improvement.

The key features of ABB can be summarized thus:

(a) A clear link between strategic objectives and planning and the tactical planning of the ABB process.

(b) The use of activity analysis to relate costs to activities.

(c) The identification of cost improvement opportunities.

(d) A focused, participative approach by all levels to guide and sustain continuous improvement.

3. Activity Based Management:

The focus in an activity based management (ABM) system is not only to calculate cost, but also to facilitate management of the organization via an understanding of the activities and processes of which they form a part. Cost can, to a certain extent, be managed by managing the causes of cost or the activity levels.

ABM refers to the management philosophy that focuses on the planning, execution and measurement of activities as the key to competitive advantage. The ABM is a much broader concept than ABC. Its aim is to use information generated by ABC, for effective business processes and profitability.

4. Activity Based Accounting:

Activity Based Accounting (ABA), is an extension of activity based costing concept, which involves in “collection, recording, analysis, controlling and reporting of activity related costs rather than departmental or cost centre related costs”. Activity based accounting deals with collection of financial and operational performance information about significant activities, and identifying the causal factors or activity cost drivers.

Activity based accounting includes the following:

(a) Activity based costing for costing of products and services.

(b) Activity based budgeting.

(c) Activity cost management used for planning and control.

(d) Activity performance measurement for performance monitoring through financial and non- financial indicators.

(e) Reducing the number of vendors reduces purchasing activities related qualifying vendors, negotiating contracts, and the like.

(f) Reducing the number of parts in a product reduces assembly activity.

(g) Reducing the number of engineering change orders reduces the amount of rework activity, and

(h) Reducing setup time reduces machine setup activity.

A major benefit of activity accounting is that managers are forced to view operations as the management of activities, not cost.