In this article we will discuss about the final accounts of general insurance companies, explained with the help an illustration.

General insurance business means business other than life insurance business. General insurance companies operating in India were nationalised on 13th May, 1971 by the Ordinance of the President of India. The accounts of the General Insurance Companies were maintained according to the provisions of Insurance act 1938. Under the previous law, separate Revenue Account had to be prepared for each type of business-fire, marine, accident, etc.

The following accounts were used to be prepared in the case of General Insurance Companies:-

(a) Revenue Account:

ADVERTISEMENTS:

A separate revenue account is prepared for each type of business. Incomes and expenses of a particular business are recorded separately and profit or loss arising there from is transferred to Profit and Loss Account.

(b) Profit and Loss Account:

General incomes and expenses not belonging to a particular business are recorded in it and balance of profit or loss is transferred to Profit and Loss Appropriation Account.

(c) Profit and Loss Appropriation Account:

ADVERTISEMENTS:

Appropriations of profit for various purposes are shown in it and it’s balance is transferred to balance sheet.

(d) Balance Sheet:

It shows various assets and liabilities of general insurance companies. Performa of Balance Sheet is same for general and life insurance companies.

Before the incorporation of IRDA Act, 2000 which allowed private players, general insurance business was conducted by General Insurance Corporation of India and its four subsidiaries.

ADVERTISEMENTS:

But now, Final account of general insurance business are required to be prepared as per IRDA Regulations, 2002 which consist of:

(a) Revenue Account (as per Form B-RA);

(b) Profit and Loss Account (Form B-PL);

(c) Balance Sheet (Form B-BS).

ADVERTISEMENTS:

The summaries of these accounts are as follows:

1. Revenue Account:

A separate Revenue Account (Form B-RA) is prepared for each type of business e.g., fire, marine etc. It records the incomes and expenses of a particular business and profit/loss is transferred to Profit and Loss Account.

2. Profit and Loss Account:

ADVERTISEMENTS:

(Form B-PL) Besides, profit/loss of different business, it records incomes and expenses of general nature and it shows how the profit has been appropriated. Its balance is shown in the Balance Sheet.

3. Balance Sheet:

(Form B-BS) It records various assets and liabilities of the General Insurance Companies.

ADVERTISEMENTS:

It must be observed that difference in revenue account does reveal profit or loss of business. The revenue account is closed by transfer to respective fund account viz., fire fund, marine fund etc. Ascertainment of profit under General Insurance Business. General insurance policies are normally issued for short terms renewable every year.

It is quite possible that on the accounting date, some of the contracts are still alive and hence represent unexpired risk. A suitable provision is made for that unexpired risk on a generalized basis as it is impractical to create it for specific policies. Sometimes an additional provision is also created. The total of reserve for unexpired risk and additional risk is collectively termed as ‘Respective Fund’ which may be fire fund, marine fund, motor vehicle fund, etc.

The revenue account starts and ends with respective value of the fund besides recording normal revenue and expenditure. The difference of the account is called profits or loss and is transferred to Profit and Loss Account.

Reserve for Unexpired Insurance:

ADVERTISEMENTS:

According to the provisions of Insurance Act, 1938, provision for unexpired risks in case of fire, marine, cargo and miscellaneous business is to be created-@ 40% of the net premiums received and 100% in case for marine Hull. However, income determination of general insurance business is done as per section 44 of Income-tax Act, 1961 and Rule 6 E of the Income-tax Rules.

They provide for reserve for unexpired risk allowed as deduction up to 50% of net premium income in case of fire insurance and miscellaneous insurance and 100% of net premium in case of marine insurance.

As such, reserve is to be made at 50% of the net premium income in case of fire and other insurance businesses and at 100% of the net premium income in case of marine insurance business. A prudent insurance company may make additional reserve in case of fire and miscellaneous insurance business, if it considers it necessary.

Commission to Agents:

Commission on policies effected through insurance agents cannot exceed 5% of the premium in respect of fire and marine business and 10% in case of miscellaneous business. In case of policies effected through principal agents the maximum limits are 20% for fire and marine policies and 15% in the case of miscellaneous insurance less any commission payable to an insurance agent with respect to the policy concerned. Certain concessions are available in this respect to principal agents having a foreign domicile.

Claims:

ADVERTISEMENTS:

Claims paid must include all expenses directly incurred in settling claims such as legal expenses, medical expenses, surveyor’s expenses etc.

No claim of Rs. 20,000 or more can be paid, except as the Controller of Insurance may otherwise direct, unless there is a report in respect thereof from an approved surveyor or loss assessor (licensed under the Insurance Act).

Regulations Given by Insurance Regulatory and Development Authority:

An insurer carrying on general insurance business, after the commencement of Regulations given by the Insurance Regulatory and Development Authority on 30th March, 2002, shall comply with the requirements of Schedule B for the preparation of financial statements, management report and auditor’s report.

Schedule B as given by IRDA is reproduced below:

General Instructions for Preparation of Financial Statements:

1. The corresponding amount for the immediately preceding financial year for all items shown in the Balance Sheet, Revenue Account, and Profit and Loss Account shall be given.

2. The figures in the financial statements may be rounded off to the nearest thousands.

3. Interest, dividends and rentals receivable in connection with an investment should be stated at gross value; the amount of income tax deducted at source being included under ‘advance taxes paid’.

4. Income from rent shall not include any notional rent.

5. (I) For the purposes of financial statements, unless the context otherwise requires:

(a) The expression ‘provision’ shall, subject to note (II) below mean any amount written off or retained by way of providing for depreciation, renewals or diminution in value of assets, of retained by way of providing for any known liability or loss of which the amount cannot be determined with substantial accuracy.

(b)The expression ‘reserve’ shall not, subject to as aforesaid, include any amount written off or retained by way of providing for depreciation, renewals or diminution in value of assets or retained by way of providing for any known liability.

(c) The expression ‘capital reserve’ shall not include any amount regarded as free for distribution through the profit and loss account; and the expression ‘revenue reserve’ shall mean any reserve other than a capital reserve.

(d) The expression “liability” shall include all liabilities in respect of expenditure contracted for and all disputed or contingent liabilities.

(II) Where:

(a)Any amount written off or retained by way of providing for depreciation, renewals or diminution in value of assets, or

(b)Any amount retained by way of providing for any known liability is in excess of the amount which in the opinion of the directors is reasonably necessary for the purpose, the excess shall be treated for the purpose of these accounts as a reserve and not provision.

6. The company should make provision for damages under law suits where the management is of the opinion that the award may go against the insurer.

7. Extent of risk retained and reinsured shall be separately disclosed.

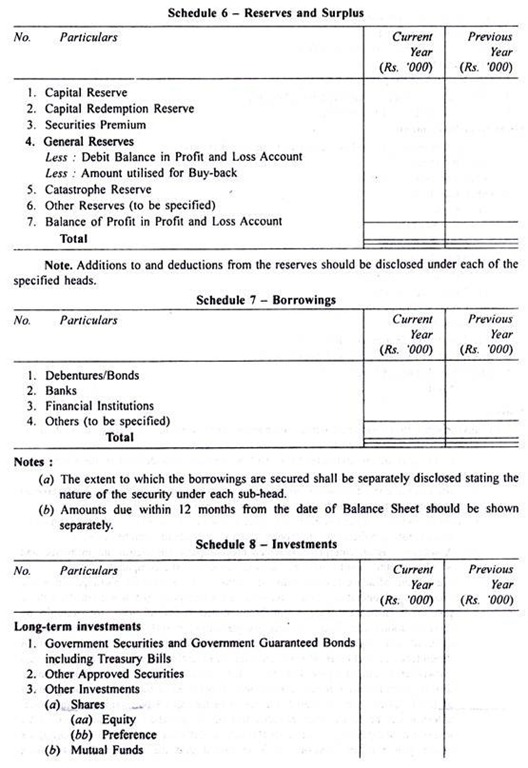

8. Any debit balance of the Profit and Loss Account shall be shown as deduction from uncommitted reserves and the balance, if any, shall be shown separately:

1. An insurer shall prepare the Revenue Account, Profit and Loss Account [Shareholders’ Account] and the Balance Sheet in Form B-RA, Form B-PL and Form B-BS, or as near thereto as the circumstances permit.

Provided that an insurer shall prepare Revenue Account and Balance Sheet for fire, marine and miscellaneous insurance business and separate schedules shall be prepared for Marine Cargo, Marine-other than Marine Cargo and the following classes of miscellaneous insurance business under miscellaneous insurance and accordingly application of AS-17 (Segment Reporting) shall stand modified.

(i) Motor

(ii) Workmen’s Compensation/Employers’ Liability

(iii) Public/Product Liability

(iv) Engineering

(v) Aviation

(vi) Personal Accident

(vii) Health Insurance

(viii) Others

2. An insurer shall prepare separate Receipts and Payments Account in accordance with the Direct Method prescribed in AS-3 “Cash Flow Statement” issued by the ICAI.

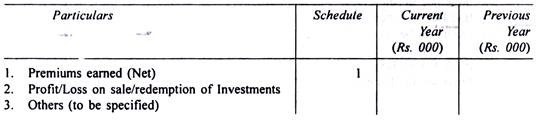

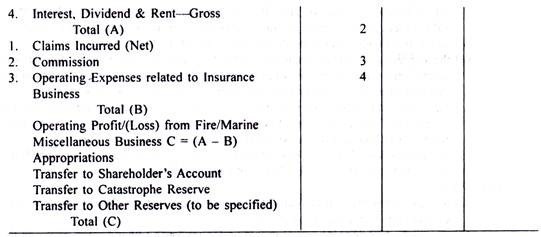

Form B-RA

Name of the Insurer:

Registration No. and Date of Registration with the IRDA

Revenue Account for The Year Ended 31st March, 20…

Policyholders’ Account (Technical Account)

Note:

See Notes appended at the end of Form B-PL:

Form B-PL

Name of the Insurer:

Registration No. and Date of Registration with the IRDA

Profit and Loss Account for The Year Ended 31st March, 20…

Shareholders’ Account (Non-technical Account)

Notes:

To Form B-RA and B-PL:

(a) Premium income received from business concluded in and outside India shall be separately disclosed.

(b) Reinsurance premiums whether on business ceded or accepted are to be brought into account gross (i.e., before deducting commissions) under the head reinsurance premiums.

(c) Claims incurred shall comprise claims paid, specific claims settlement costs wherever applicable and change in the outstanding provisions for claims at the year-end.

(d) Items of expenses and income in excess of one per cent of the total premiums (less reinsurance) or Rs. 5, 00,000 whichever is higher, shall be shown as a separate line item.

(e) Fees and expenses connected with claims shall be included in claims.

(f) Under the sub-head “Others” shall be included items like foreign exchange gains or losses and other items.

(g) Interest, dividends and rentals receivable in connection with an investment, should be stated at gross amount, the amount of income tax deducted at source being included under “advance taxes paid taxes deducted at source”.

(h) Income from rent shall include only the realised rent. It shall not include any notional rent.

From B BS

Name of the Insurer:

Registration No. and Date of Registration with the IRDA

Balance Sheet as at 31st March, 2006

Notes:

(a) Investments in subsidiary/holding companies, joint ventures and associates shall be separately disclosed, at cost:

(i) Holding company and subsidiary shall be construed as defined in the Companies Act. 1956.

(ii) Joint Venture is a contractual arrangement whereby two or more parties undertake an economic activity, which is subject to joint control.

(iii) Joint control – is the contractually agreed sharing of power to govern the financial and operating policies of an economic activity to obtain benefits from it.

(iv) Associate – is an enterprise in which the company has significant influence and which is neither a subsidiary nor a joint venture of the company,

(v) Significant influence (for the purpose of this schedule)-means participation in the financial and operating policy decisions of a company, but not control of those policies. Significant influence may be exercised in several ways, for example, by representation on the board of directors, participation in the policy making process, material inter-company transactions, interchange of managerial personnel or dependence on technical information. Significant influence may be gained by share ownership, statute or agreement.

As regards share ownership, if an investor holds, directly or indirectly through subsidiaries, 20 per cent or more of the voting power of the investee, it is presumed that the investor does have significant influence, unless it can be clearly demonstrated that this is not the case. Conversely, if the investor holds, directly or indirectly through subsidiaries less than 20 per cent of the voting power of the investee, it is presumed that the investor does not have significant influence, unless such influence is clearly demonstrated. A substantial or majority ownership by another investor does not necessarily preclude an investor from having significant influence.

(b) Aggregate amount of company’s investments other than listed equity securities and derivative instruments and also the market value thereof shall be disclosed.

(c) Investment made out of Catastrophe reserve should be shown separately.

(d) Debt securities will be considered as “held to maturity” securities and will be measured at historical costs subject to amortisation.

(e) Investment property means a property [land or building or part of a building or both] held to earn rental income or for capital appreciation or for both, rather than for use in services or for administrative purposes.

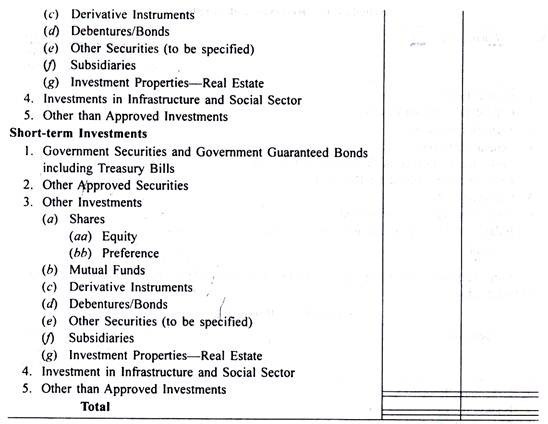

(f) Investments maturing within twelve months from balance sheet date and investments made with the specific intention to dispose of within twelve months from balance sheet date shall be classified as short-term investments.

Notes:

(a) Short-term loans shall include those, which are repayable within 12 months from the date of balance short. Long-term loans shall be the loans other than short-term loans.

(b) Provisions against non-performing loans shall be shown separately.

(c) The nature of the security in case of all long-term secured loans shall be specified in each case. Secured loans for the purposes of this schedule, means loans secured wholly or partly against an asset of the company.

(d) Loans considered doubtful and the amount of provision created against such loans shall be disclosed.

Notes:

(a) No item shall be included under the head “Miscellaneous Expenditure” and carried forward unless:

(i) Some benefit from the expenditure can reasonably be expected to be received in future, and

(ii) The amount of such benefit in reasonably determinable.

(b) The amount to be carried forward in respect of any item included under the head “Miscellaneous Expenditure” shall not exceed the expected future revenue/other benefits related to the expenditure.

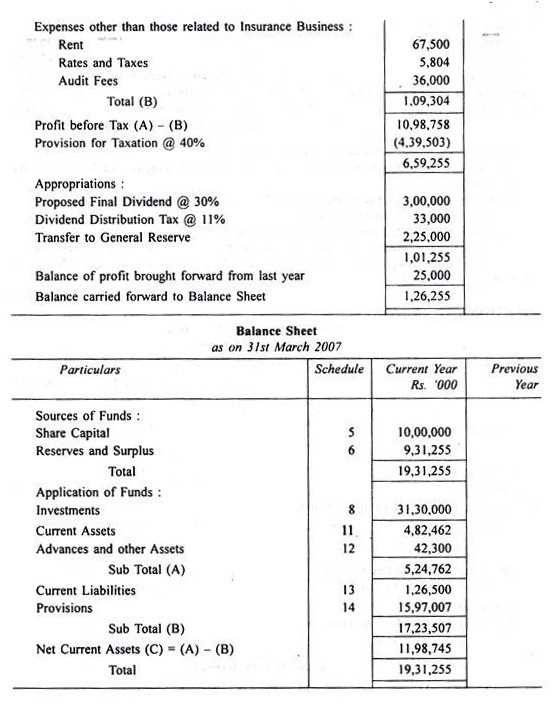

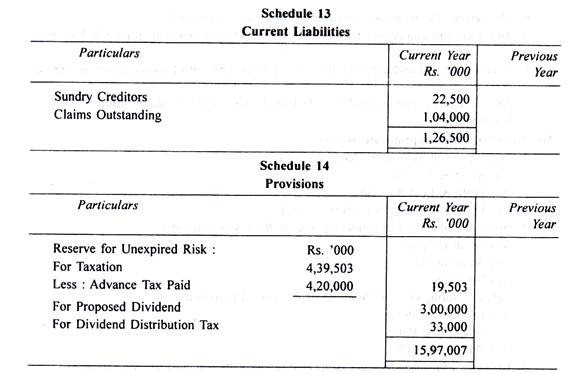

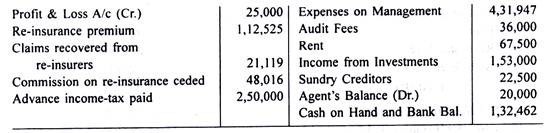

Illustration (Fire Insurance Revenue Account and Final Accounts):

From the following figures taken from the books of New Asia Insurance Company Ltd. doing fire underwriting business.

Prepare the set of final accounts for the year 2006-2007:

The following further information may also be noted:

(a) Expenses of management include survey fees and legal expenses of Rs. 36,000 and Rs. 20,000 relating to claims;

(b) Claims intimated but not paid on 31st March 2006—Rs. 1, 04,000;

(c) Income-tax to be provided at 40%;

(d) Transfer of Rs. 2, 25,000 to be made from Current Profits to General Reserve.

(e) The company maintains a reserve for unexpired risk @ 50% of net premium income.

(f) The directors propose a dividend @ 30%. Dividend distribution tax is payable @ 11% which includes surcharge (CA Inter)