Public utility concerns in England were previously required to prepare their accounts under the Double Account System. The Double Account System is merely a way of presentation of final accounts. It should not be confused with the Double Entry System which is the basis of maintaining books of account.

Up to the preparation of the trial balance, there is no difference between the Double Account System and the ordinary system. Only when it comes to preparation of the Balance Sheet and the Revenue Account that there is a difference.

The chief features of the Double Account System are as follows:

1. The ordinary balance sheet is split up in two parts. One part contains fixed assets and fixed liabilities. It is called “Receipt and Expenditure on Capital Account.” On each side there are three columns for amount—one column to show figures up to the beginning of the year, the second column to show expenditure (assets) or receipts (liabilities) during the year and the third column to show total.

ADVERTISEMENTS:

The other part (called General Balance Sheet) contains other assets and liabilities and the balance of the Receipts and Expenditure on Capital Account. In case of electricity companies, however, the total of the expenditure as per Capital Account is shown on the assets side and the total of receipts is shown on the liabilities side.

2. A Revenue Account is prepared which is like the ordinary’ Profit and Loss Account. Also, a Net Revenue Account is prepared which is like the ordinary Profit and Loss Appropriation Account.

The exceptions are as follows:—

ADVERTISEMENTS:

(a)Interest in all cases is debited or credited to Net Revenue Account and not to Revenue Account. In cases of Railways, rent on leased land, etc., is also debited to Net Revenue Account.

(b)Depreciation is debited to Revenue Account and credited to Depreciation Reserve. Depreciation Reserve appears on the liability side of the General Balance Sheet.

The forms of the Receipts and Expenditure on Capital Account and the General Balance Sheet are given on page 27.33.

Illustration 1:

ADVERTISEMENTS:

Provide for the under-mentioned depreciation, and prepare a Receipts and Expenditure on Capital Account, Revenue Account, Net Revenue Account and Balance Sheet from the following Trial Balance. A call of Rs 20 per share was payable on 30th September, 2011 and arrears are subject to interest @ 15% p.a.

Depreciation to be provided for on: Building @ 5%, Machinery @ 15%, Mains @ 20%, Transformers etc., @ 10%, Meters and Electrical Instrument @ 15%.

Replacement of an Asset:

Ordinarily, the amount standing in books against an asset is written off when the asset is replaced by another. The amount spent on the new asset is capitalised. Under the Double Account System, however, the practice is different.

Firstly, the account of the asset which is replaced is not affected at all. An appropriate amount out of the new expenditure is charged to revenue or written off and the balance is capitalised. Secondly, the amount to be written off is the amount which would have been spent had the asset been acquired now.

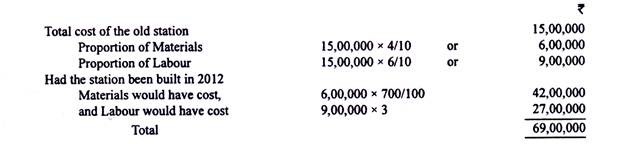

Suppose, a railway station built in 1980 at a cost of Rs 15,00,000 is replaced, in 2012, by a new station costing Rs 80,00,000. Suppose further that between 1980 and 2012, prices of materials have risen to 700%, that labour rates have trebled and that the proportion of materials and labour in the old station is 4: 6.

ADVERTISEMENTS:

The amount to be written off will be arrived at as under:

Out of Rs 80,00,000 spent in 2012, Rs 69,00,000 would be written off and Rs 11,00,000 i.e., 80,00,000—69,00,000 would be capitalised. The total amount capitalised would be Rs 26,00,000, i.e., Rs 15,00,000 + Rs 11,00,000.

The entries to be made are as follows:—

ADVERTISEMENTS:

1. Debit Replacement Account with the amount to be written off; Debit Works Account (new) with the amount to be capitalised; and Credit Bank with the amount actually spent.

2. If any old materials have been used in the new construction:

Debit Works Account

Credit Replacement Account.

ADVERTISEMENTS:

3. If any old materials have been sold:

Debit Bank

Credit Replacement Account.

The logic behind the treatment outlined above is firstly, that additional amount should be capitalised only if there is additional capacity and, secondly, that when an old asset is replaced, the amount lost is the asset’s present value rather than its historical cost.

Illustration 2:

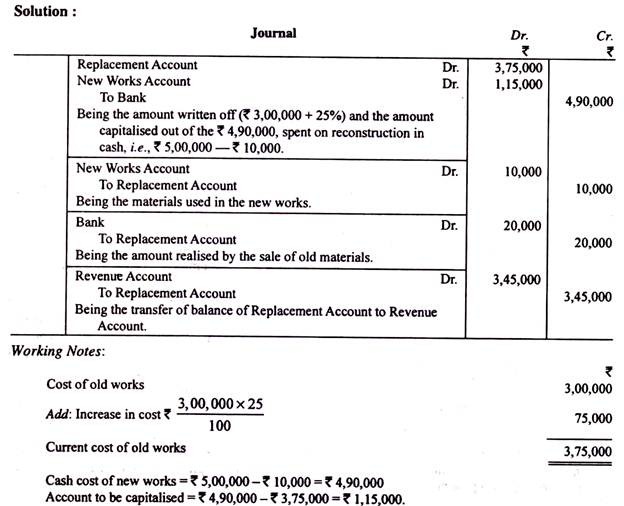

The Hindustan Gas Company rebuilt and re-equipped part of their works at a cost of Rs 5,00,000. The part of the old works thus superseded cost Rs 3,00,000. The capacity of the new works is double the capacity of the old works.

ADVERTISEMENTS:

Rs 20,000 is realised by the sale of old materials, and old materials worth Rs 10,000 are used in the construction of the new works and included in the total cost of Rs 5,00,000 mentioned above. The costs of labour and materials are 25% higher than when the old works were built.

Journalise the entries.

Illustration 3:

The Gurgaon Electricity Company Limited decides to replace one of its old plants with a modem one with a larger capacity. The plant when installed in 1985 cost the company Rs 24 lakhs, the components of materials, labour and overheads being in the ratio of 5: 3: 2. It is ascertained that the costs of materials and labour have gone up by 40% and 80% respectively.

The proportion of overheads to total costs is expected to remain the same as before.

The cost of the new plant as per improved design is Rs 60 lakhs and in addition, material recovered from the old plant of a value of Rs 2,40,000 has been used in the construction of the new plant. The old plant was scrapped and sold for Rs 7,50,000.