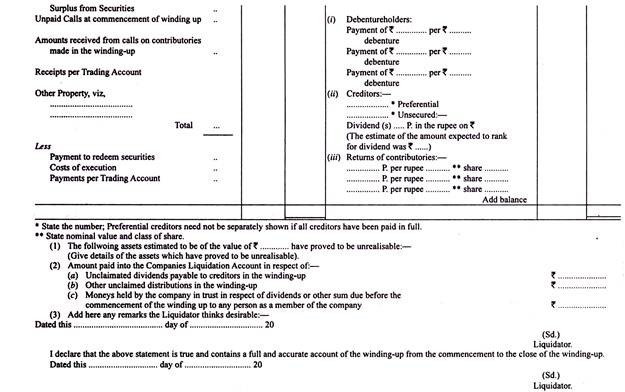

The liquidator’s task is to realise the assets and disburse the amounts among those who have a rightful claim to it; in every case the liquidator has to prepare a statement showing how much he realised and how the amount was distributed.

The following is the order in which disbursements will be made by the liquidator:—

(a) Secured creditors up to their claim or up to the amount realised by sale of securities held by them, whichever is less. The creditors themselves may sell the securities; they will pay to the liquidator any surplus after meeting their claims. Only the surplus is shown as a receipt; the payment to secured creditors is not shown in the liquidator’s final statement of account.

The balance left unsatisfied—that is when the claims of the creditors are more than the amount realised by sale of securities—will be added to unsecured creditors. Workmen’s dues will rank pari passu with the secured creditors. These are called overriding preferential payments.

ADVERTISEMENTS:

(b) Legal charges.

(c) Remuneration to the liquidator.

(d) Costs of winding up.

(e) Preferential creditors.

ADVERTISEMENTS:

(f) Debenture holders or other creditors having a floating charge on the assets of the company. (While preparing the Liquidator’s Statement of Account, payment to preferential creditors is shown, however, after the payment to debenture holders having a floating charge.)

(g) Unsecured creditors. (This may include liability in respect of dividend or amounts due to shareholders on account of profits. In this case, the amount in respect of dividends, etc., shall be paid only after the outsiders are satisfied.)

(h) Preference shareholders,

(i) Equity shareholders. Unless the articles contain provisions to the effect that preference shareholders are entitled to participate in the surplus left after meeting the claims of the equity shareholders in full, the whole of the amount left after payment to preference shareholders will go to the equity shareholders.

ADVERTISEMENTS:

The various claims have priority in the order mentioned above. Hence, if the amount available is exhausted after paying, say, the preferential creditors, payment cannot be made to unsecured creditors or anybody else coming after the preferential creditors. The form prescribed by the Supreme Court is given later.

While preparing the Liquidator’s Statement of Account, it should be remembered that there is no double entry involved. It is only a statement although presented in the form of an account. (It is really a summary of the Cash Book after the start of liquidation).

Some Special Points:

Liquidator’s Remuneration. In case of compulsory winding up, the remuneration is fixed by the Court and the amount is payable to the Court since the official liquidator is a salaried employee of the Government. In case of voluntary winding up, the remuneration is fixed by the meeting which appoints the liquidator. The remuneration once fixed cannot be increased.

ADVERTISEMENTS:

Usually, the remuneration consists of a commission on assets realised plus a commission on the amount paid to unsecured creditors. Unsecured creditors include preferential creditors unless otherwise stated. The commission on unsecured creditors is on the amount paid and hence care should be exercised in calculating the commission.

If the commission is 2% on amount paid to unsecured creditors, a payment of Rs 100 to the unsecured creditors will entail a commission of Rs 2 to the liquidator, thus absorbing Rs 102. Hence, if the amount available is insufficient to pay the unsecured creditors fully, the commission due to the liquidator will be 2/102 of the amount available; the balance will be paid to the unsecured creditors.

Suppose, the amount realised by sale of assets is Rs. 3,00,000, and the amount due is Rs. 3,40,000 including Rs. 10,000 as preferential creditors. Then, if the liquidator is entitled to a commission of 3% on amounts realised and 2% on amounts distributed among the unsecured creditors, his remuneration will be calculated as follows :—

Illustration 1:

ADVERTISEMENTS:

The Ultra Optimist Ltd. went into liquidation. Its assets realised Rs 3,50,000 excluding amount realised by sale of securities held by the secured creditors.

The following was the position:

Illustration 2:

ADVERTISEMENTS:

A company wen into liquidation on 31st March, 2012 when the following balance sheet was prepared:

Debenture Interest:

Debenture interest should be paid to the date of payment if the company is solvent. If the company is insolvent, interest should be paid only up to the date of winding up; the same applies to interest payable to other creditors. A company is solvent if it can pay all its creditors.

Preference Dividend:

ADVERTISEMENTS:

The position regarding arrears of dividend on preference share capital may be summarised as follows:—

(i) The question of arrears does not arise in case of non-cumulative preference shares. But if the shares are not specifically stated as non-cumulative, they should be treated as cumulative.

(ii) No dividend is payable for any period falling after the commencement of winding up.

(iii) As regards arrears of dividend up to the date of winding-up, the provisions of the Articles of Association will apply. As a rule, a dividend becomes payable only when declared by the shareholders in general meeting. If dividend on preference shares was declared, it is to be paid as a debt and not as an arrear of dividend.

It is settled law that in the case of cumulative preference shares, the arrears of dividend are payable on winding up, subject, of course, to settlement of all claims of outsiders. Thus, if need be and possible, a call should be made on equity shareholders to pay arrears of dividend on cumulative preference shares.

Equity Shareholders are paid last of all, if funds are available. In case the equity shares are partly paid and the amount available is not sufficient to satisfy the claims of preference shareholders in full, the equity shareholders should be called upon to pay a suitable amount.

Example:

1. The amount available after paying all creditors is Rs 75,000. The company’s share capital consists of 10,000 Preference Shares of Rs 10 each, and 10,000 Equity Shares of Rs 10 each, Rs 6 paid. In this case the equity shareholders will have to pay Rs 2.50 per share so that their contribution (Rs 2.50, x 10,000) together with the amount already available will enable the preference shareholders to be paid off.

2. But suppose, in the above example, the amount available after paying all creditors is Rs 20,000, other facts being the same as above. In that case, the equity shareholders will pay Rs 4 per share because that is the maximum they can be called upon to pay. They will contribute Rs 40,000 thus making the total amount available to be Rs 60,000. This will be paid to the preference shareholders.

If the equity shareholders have paid different amounts on their shares, the loss suffered by each equity shareholder should be equal. While distributing cash among them or while calling upon them to pay, care should be taken to see that all equity shareholders suffer equally.

Examples:

1. The amount available after paying creditors and preference shareholders is Rs 80,000. The company’s equity share capital consists of 10,000 shares of Rs 10 each, Rs 8 paid up and 5,000 shares of Rs 10 each, Rs 6 paid up. In this case, first Rs 2 must be returned on those shares on which Rs 8 has been paid up. This will make all shares Rs 6 paid. This will absorb Rs 20,000; the remaining Rs 60,000 will be distributed on 15,000 shares, i.e., Rs 4 per share. The loss suffered by equity shareholders will be Rs 2 per share.

2. The amount available after paying creditors is Rs 60,000.

The company’s share capital consists of:—

(a) 10,000 14% Preference Shares of Rs 10 each.

(b) 40,000 Equity Shares of Rs 10 each, Rs 9.50 paid.

(c) 60,000 Equity Shares of Rs 10 each, Rs 9 paid.

In this case, the additional amount required for paying the preference shareholders is Rs 40,000, i.e., 1,00,000 — 60,000. This amount should be raised by first of all calling up 50 paise on 60,000 equity shares (which will raise Rs 30,000 and which will make all equity shares Rs 9.50 paid up). The remaining amount of Rs 10,000 should be raised by calling up a further 10 paise on all equity shares. Thus holders of 40,000 equity shares will pay 10 paise per share and those holding 60,000 equity shares will pay 60 paise per share.

Illustration 3:

The following information to you:

Illustration 4:

Miniature Ltd. went into voluntary liquidation on 31st March, 2012. The balances in its books on that day were:

The Bank called upon the Directors to implement their guarantee. The preference dividend had been paid up to 30th September, 2009. There were no arrears of debenture interest. The amount owing to the Government for income-tax was in respect of assessment years 2010-2011 and 2011-2012 of Rs 3,250, Rs 14,300 respectively. The company closes its accounts on 31st March each year.

The Liquidator admitted an amount of Rs 2,730 for salaries in lieu of notice. The rent was paid up to 31st March, 2012. The premises were held under a lease with annual tenancy. The landlord agreed to waive his right to notice on the Liquidator undertaking to pay him two months’ rent, i.e., Rs 650 and to vacate the premises by 31st May, 2012 which he did.

One of the creditors for Rs 13,000 was under a contract to deliver certain goods to the Company in March, 2012 and the Company had contracted to supply the same goods to Basic Ltd., who were included in Sundry Debtors at Rs 6,500.

The creditor refused to make delivery but admitted a claim made by the Liquidator for damages at Rs 1,625. Basic Ltd. made a claim for loss against the Company for Rs 975 which was admitted by the Liquidator.

Furniture was sold for Rs 7,800. Investments were found to be valueless. Sums owing by Debtors were all collected and the Insurance Policy was surrendered for Rs 15,600 after the Liquidator had paid a premium of Rs 585. A shareholder holding 2,600 equity shares failed to pay the call made by the Liquidator Legal costs came to Rs 780 and liquidator’s remuneration to Rs 6,500.

Prepare Liquidator’s Final Statement of Account. (Adapted C.A., Final)

Receiver for Debenture-holders:

A receiver is generally appointed by the Court to take possession of certain property for protective purposes or for receiving income and profits from the property and for applying it as directed. Sometimes, a mortgagee is also given the power to appoint a receiver in certain circumstances. The debenture-holders may have the power under the Debenture Deed.

The Receiver will have the duty of duly accounting for the sums received by him. In case the company is being wound up, the Receiver (if appointed) will have to observe the rule regarding preferential payments and after paying the mortgagee by whom he is appointed (or paying those persons for whose protection he is appointed by the Court) he will have to hand over the surplus to the Liquidator.

There will thus be two accounts: (1) the Receiver’s Statement of Account and (2) Liquidator’s Final Statement of Account. The Receiver is entitled to recover his expenses and remuneration from sums collected by him.

Illustration 5:

The following is the Balance Sheet of Overconfident Ltd. as on 31st March, 2012.

The mortgage was secured on the buildings and the debentures were secured by a floating charge on all the assets of the company. The debenture-holders appointed a Receiver. A Liquidator was also appointed, the company being voluntarily wound up.

The Receiver was entrusted with the task of realising the Buildings which fetched Rs 40,000. The Receiver took charge of “Sundry Assets” amounting to Rs 4,00,000 and sold them for Rs 3,70,000. The Bank was secured by a personal guarantee of the directors who discharged their obligations in full.

The balance of the assets realised Rs 1,20,000. The costs of the Receiver amounted to Rs 1,000 and his remuneration to Rs 1,250. The expenses of liquidation was Rs 2,000 and the remuneration of the liquidator was Rs 750. Preference dividend was in arrear for 3 years. According to the Articles, the arrears were payable if there was a surplus on winding up.

Prepare the accounts to be submitted by the Receiver and the Liquidator.

Illustration 6:

X-ray Ltd. is a private company, the members’ holding being:

Dividends on Preference shares were paid up to 30th September, 2011. Under the Articles, arrears of preference dividend were automatically payable in the event of the company being wound up. Also holders of preference shares are entitled to participate equally with equity shareholders in surplus assets up to Rs 2 per share.

On 1st October, 2012 it was decided to take the company into liquidation; R, A and Y decided to form a partnership to carry on the business previously carried on by the company. They agreed that the partnership capital should be Rs 4,50,000 to be provided in the same ratio as that of equity shares held by them.

They also agreed that they would bring into the firm, as loan, any cash received by them. X agreed to lend to the firm the amount which he would receive by way of capital on his preference shares.

The liquidator was given power to distribute assets in specie; R, A and Y agreed to take the assets so distributed, bringing them into the firm at the values placed on them by the liquidator.

The liquidation was completed on 31st January, 2013; the liquidator dealt with the assets as follows:

(i) Freehold property sold for Rs 4,15,000.

(ii) Plant distributed at Rs 92,500.

(iii) Furniture distributed at a valuation of Rs 1,80,000

(iv) One motor sold for Rs 7,500; the other distributed at Rs 25,000.

(v) Quoted investments sold for Rs 81,000.

(vi) Trade Investments distributed at Rs 55,000.

(vii) Inventories distributed at book values; and

(viii) Trade Receivables realised in full subject to bad debts of Rs 3,500. The creditors were repaid subject to a discount of Rs 1,000; other liabilities were paid off on 31st January, 2013.

The liquidator’s remuneration was agreed at 1% on the assets converted into cash and, in addition, 2% on the total return of capital to contributories. Liquidation expenses totalled Rs 2,000.

Prepare the Liquidator’s Statement of Account and show the distribution among R, A and Y.

(Adapted from C.A. Eng., PEL)

Illustration 7:

The following is the Balance Sheet of Y Limited as at 31st March, 2012:

“B” List of Contributories:

Those persons who ceased to be shareholders (other than by death) within a year of the date of winding up of the company are liable to pay up the amount unpaid on the shares held by them, if the amount due to various persons, while such former members were shareholders, remains unpaid at the time of winding up.

Such former members are not liable to contribute for debts incurred after they ceased to be members. They will not also be liable, if all the creditors can be paid out of the moneys realised from sale of assets or from the shareholders who are members at the time of winding up (“A” List). Also, there will be no liability to pay anything if the present shareholders pay or have paid the amount due on the shares.

Suppose, A held 1,000 shares of Rs 10 each, Rs 7.50 paid up. He transferred his shares on 31st October, 2011 to B. The company goes into liquidation on 31st March, 2012. A debt existing on, 31st October, 2011 remains unpaid. A can be called upon to pay the debt subject to the maximum limit of Rs 2,500 because his total liability, when he transferred his shares, was Rs 2.50 per share.

Had A transferred the shares on, say, the 15th March, 2011, there would have been no liability upon him. Also, if B has paid the amount due on the shares, A has no liability, if there are more than one member who ceased to be such within one year of the date of winding up, each would be liable to pay proportionately subject to the maximum due on the shares.

Suppose (1) a company goes into liquidation on 31st October, 2010 leaving a debt of Rs 2,400 unpaid; (2) it is found that A who held 1,000 shares and B who held 500 shares of Rs 10 each, Rs 7 paid up, had transferred the shares on 15th November, 2010; and (3) the debt had been incurred sometime before 15th November, 2010.

In this case, A and B will contribute proportionately, that is in the ratio of 2 to 1. A will pay Rs 1,600 and B will pay Rs 800.

Illustration 8:

In liquidation which commenced on 1st April, 2012 certain creditors could not receive payment out of the realisation of the assets and out of contribution from “A” list contributories. The following are the details of certain transfers which took place after 1st April, 2011:—

Solution:

The amount of Rs 6,000 outstanding on 1st May, 2011 will have to be contributed by all the four persons in the ratio of number of shares held by them, i.e., in the ratio of 10:15:3:2.

Thus A will have to contribute Rs 2,000. B, Rs 3,000; C, Rs 600 and D. 1400. Similarly, the further debts incurred between 1st May, 2011 and 1st July, 2011 viz., Rs 1,500 (for which A is not liable) will be contributed by B, C, and D in the ratio of 15:3:2. B will have to contribute Rs 1,125, C will have to contribute Rs 225 and D will have to contribute Rs 150.

The further increase from Rs 7,500 to Rs 8,000; viz., Rs 500 occurring between 1st July, 2011 and 1st November, 2011 will be shared by C and D who will be liable for Rs 300 and Rs 200 respectively. The increase between 1st November, 2011 and 1st February, 2012 is solely the responsibility of D.

The following statement makes the position clear.

Illustration 9:

Pessimist Ltd. has gone into liquidation on 10th May, 2012. The details of members, who have ceased to be members within one year (‘B’ contributories) are given below. The debts that could not be paid out of realisation of assets and contribution from present members (‘A’ contributories) are also given with their date-wise break up. Shares are of Rs 10 each, Rs 6 per share paid up.

You are to determine the amount realisable from each person.

Illustration 10:

In a winding up of a company certain creditors remained unpaid. The following persons had transferred their holding sometimes before winding up: