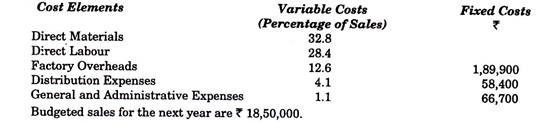

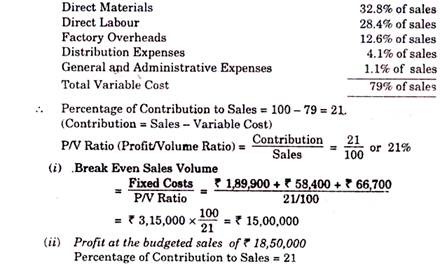

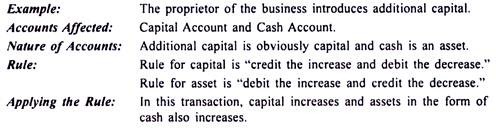

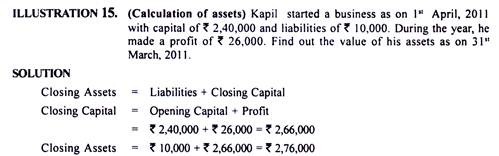

Are you looking for problems and solutions on liquidation of companies? You are in the right place! In this article we have compiled top ten problems on liquidation of companies along with its relevant solutions.

Contents:

- Preparation of Statement of Affairs to the Meeting of Creditors

- Preparation of Statement of Affairs to the Meeting of Creditors

- Preparation of Statement of Affairs and the Deficiency Account

- Preparation of Liquidators Final Statement of Account

- Preparation of Liquidator’s Final Statement of Account

- Preparation of Liquidator’s Final Statement of Account

- Preparation of Liquidators Final Statement of Accounts

- Preparation of Liquidator’s Final Statement of Account

- Preparation of Liquidator’s Final Statement of Receipts and Payments

- Preparation of Accounts to be Submitted by the Receiver and the Liquidator

Problems on Liquidation of Companies

1. Preparation of Statement of Affairs to the Meeting of Creditors:

Sri Gobinda Chandra Sadhukhan is appointed liquidator of Sun Co. Ltd in voluntary liquidation on 1st July 1993.

ADVERTISEMENTS:

Following balances are extracted from the books on that date:

You are required to prepare a Statement of Affairs to the meeting of Creditors.

ADVERTISEMENTS:

The following assets are valued as under:

Bad Debts are Rs. 3,000 and the doubtful debts are Rs. 6,000 which are estimated to realise Rs. 3,000. The Bank Overdraft secured by deposit of title deeds of Leasehold Properties. Preferential Creditors are Rs. 1,500. Telephone rent outstanding is Rs. 120.

2. Preparation of Statement of Affairs to the Meeting of Creditors:

M. Co. Ltd. went into voluntary liquidation on 1.3.1991.

The following are extracted from its books on that date:

Plant and Machinery and Building are valued at Rs. 1,50,000, and Rs. 1,20,000, respectively. On realisation, losses of Rs. 15,000 are expected on Stock. Book-Debts will realise Rs. 70,000. Calls-in- arrear are expected to realise 90%. Bank Overdraft is secured against Buildings. Preferential Creditors for taxes and wages are Rs. 6,000 and Miscellaneous expenses outstanding Rs. 2,000.

ADVERTISEMENTS:

Prepare a Statement of Affairs to be submitted to the meeting of creditors.

3. Preparation of Statement of Affairs and the Deficiency Account:

The following information is extracted from the books of Unlucky Ltd. on 31st July 1983, on which date a winding-up order was made:

In 1979 the company earned a profit of Rs. 45,000 but thereafter it suffered trading losses totalling Rs. 58,400. The Company also suffered a speculation loss of Rs. 5,000 during 1980. Excise authorities imposed penalty of Rs. 35,000 in 1981 for evasion of tax which was paid in 1982.

From the foregoing information, prepare the Statement of Affairs and the Deficiency Account.

4. Preparation of Liquidators Final Statement of Account:

The summarised Balance Sheet of Mathew Ltd. as on 31.3.1998, being the date of voluntary winding up is as under:

Preference Dividend is in arrears for two years. By 31.3.1999, the assets realised were as follows:

Expenses of liquidation is Rs. 54,000. The remuneration of the liquidator is 3% of the realisation. Income-Tax payable on liquidation is Rs. 44,500. Assuming that the final payments are made on 31.3.1999, prepare the Liquidator’s Final Statement of Account.

5. Preparation of Liquidator’s Final Statement of Account:

Prakash Processors went into voluntary liquidation on 31st Dec. 1999, when their Balance Sheet read as follows:

Preference Dividends were in arrears for 2 years and the creditors included preferential creditors of Rs. 38,000.

ADVERTISEMENTS:

The assets realised as follows:

Land and Building Rs. 3,00,000; Machinery and Plant Rs. 5,00,000; Patents Rs. 75,000; Stock Rs. 1,50,000; Sundry Debtors Rs. 2,00,000

The expenses of liquidation amounted to Rs. 27,250.

The liquidator is entitled to a commission of 3% on assets realised except cash. Assuming the final payments including those on Debentures is made on 30th June 2000, show the Liquidator’s Final Statement of Account.

6. Preparation of Liquidator’s Final Statement of Account:

Break Ltd. went into voluntary liquidation on 31.3.1991.

The balances in its books on that date were:

The liquidator is entitled to a remuneration of 5% on all assets realised except cash and 1% on the amount distributed to unsecured creditors other than preferential creditors.

Bank overdraft is secured by deposit of title deed of land and building which realised Rs. 3,00,000.

Other assets realised the following sums:

Expenses of liquidation amounted to Rs. 27,250.

Prepare Liquidator’s Final Statement of Account.

Liquidator realised all assets on 1.4.1991 and discharged his obligation on the same date. Dividend on preference shares were in arrears for two years.

7. Preparation of Liquidators Final Statement of Accounts:

The Balance Sheet of Asco Ltd. as on 31st March 1993:

The liquidators are entitled to a commission at 2% on amount paid to unsecured creditors. Calls on partly paid shares were made but the amount due on 200 shares were found to be irrecoverable.

Prepare liquidator’s Statement of Account.

8. Preparation of Liquidator’s Final Statement of Account:

T. Ltd. was placed in voluntary liquidation on 31.12.2002, when its Balance Sheet was as follows:

The Preference dividends are in arrear from 1999 onwards.

The Company’s. Articles provide that, on liquidation, out of the surplus assets remaining after payment of liquidation costs and outside liabilities, there shall be paid, firstly, all arrears of Preference dividend, secondly, the amount paid up on the Preference shares together with a premium thereon of Rs. 10 per share, thirdly, any balance then remaining shall be paid to the Equity shareholders.

The Bank overdraft was guaranteed by the Directors who were called upon by the Bank to discharge their liability under the guarantee. The Directors paid the amount to the Bank.

The liquidator realised the assets as follows:

Creditors were paid less discount of 5%. The Debentures and accrued interest were repaid on 31st March 2003.

Liquidation costs were Rs. 3,820 and the liquidator’s remuneration was 2% on the amounts realised.

Prepare the Liquidator’s Statement of Account.

1. As the company is solvent the debenture-holders are credited to interest up to the date of repayment (i.e., Rs. 2,500 as per Balance Sheet and Rs. 1,250 for 3 months). Needless to mention that if the company is insolvent interest should be paid only up to the date of winding up. A company is considered as solvent only when it can pay all of its outside liabilities.

2. If the articles of the company provides that preference shareholders are to be given equal rank both as regards payments of dividends and capital in priority to equity shares, arrear pref. dividend is also payable even it not declared in priority to any return of capital to the equity shareholders (Re. Watter Symons Ltd.) and arrear is payable up to the date of winding up only.

9. Preparation of Liquidator’s Final Statement of Receipts and Payments:

The following is the Balance Sheet of Poddar Ltd. which is in the hands of the liquidator:

The assets realised the following amounts (after all costs of realisation and liquidator’s commission amounting to Rs. 5,000 paid out of cash in hand Rs. 40,000 as per Balance Sheet):

Calls on partly paid shares were made but the amounts due on 200 shares were found to be irrecoverable.

Prepare Liquidator’s Final Statement of Receipts and Payments.

10. Preparation of Accounts to be Submitted by the Receiver and the Liquidator:

The following is the Balance Sheet of Confidence Builders Ltd., as at 30th Sept 1990 :

Mortgage loan was secured against land and buildings. Debentures were secured by a floating charge on all the other assets. The company was unable to meet the payments and therefore the debenture-holders appointed a Receiver and this was followed by a resolution for members’ voluntary winding up.

The Receiver for the Debenture-holders brought the Land and Buildings to auction and realised Rs. 1,50,000. He also took charge of Sundry assets of the value of Rs. 2,40,000 and, realised Rs 2,00,000 The Liquidator realised Rs. 1,00,000 on the sale of the balance of sundry current assets.

The Bank Overdraft was secured by a personal guarantee of two of the Directors of the Company and on the Bank raising a demand, the Directors paid off the dues from their personal resources. Costs incurred by the Receiver were Rs. 2,000 and by the Liquidator Rs. 2,800.

The Receiver was not entitled to any remuneration but the liquidator was to receive 3% fee on the value of assets realised by him. Preference shareholders had not been paid dividend of period after 30th September 1991 and interest for the last half-year was due to the debenture-holders.

Prepare the accounts to be submitted by the Receiver and the Liquidator.

Solution:

Before preparing the Liquidator’s Final Statement of Accounts, we are to prepare a Receiver’s Receipts and Payments Account as under: