The need for reconstruction arises when a company has accumulated losses or when a company finds itself overcapitalized which means either that the value placed on assets is too much as compared to their earning capacity or that the profits as a whole are insufficient to pay a proper dividend.

In the previous section, the legal position and entries in respect of reduction of capital (which in other words means internal reconstruction) have been seen. The present section seeks to discuss how and on what basis, schemes should be formulated.

Apart from clarity, wide acceptance and justice, the reconstruction scheme must take into account the following:—

The fundamental basis of any proposals is the earning power of the company. Even the interest to debenture-holders cannot be paid unless the company’s activities are profitable. A very careful estimate should, therefore, be made of the profits expected by the company in the future.

ADVERTISEMENTS:

Unless the profits are sufficient to meet all expenses including adequate depreciation, interest to debenture-holders and other creditors, preference dividend, and a reasonable return to the equity shareholders, it would be useless to proceed with any reconstruction scheme because, otherwise the need for reconstruction will soon arise again.

Assuming that adequate profits can be expected, the reconstruction scheme should not adversely affect the rights of preference shareholders (not to speak of creditors and debenture-holders) unless it is absolutely necessary.

Suppose, the profits are such that after paying dividends to preference shareholders little remains for equity shareholders; the preference shareholders may be persuaded to accept a sacrifice either by reduction of capital or by reduction in the rate of dividend or both because the alternative to such acceptance of sacrifice may be the liquidation of the company (in which case, due to forced sale, the assets may not realize much and the preference shareholders may not be able to get back what they have invested).

If the company is in a very bad position, even the debenture-holders may be prevailed upon to accept a reduction of their claims. But, so far as is possible, contractual and legal rights and priorities should be maintained. The equity shareholders will naturally have to bear the brunt of the losses and sacrifice.

ADVERTISEMENTS:

This is not as bad as it sounds because:

(a) The equity shareholders realise from the very beginning that if losses occur they have to bear them before anybody else can be called upon to do so, and

(b) They must have already known that the value of their holding is small due to absence of dividends.

The market price of shares is related to dividend and not to the face or nominal value of the shares. It really does not matter, therefore, whether the nominal value of an equity share in Re. 1 or Rs 100 or Rs 1,000 as long as it is not 0. (This does matter in case of preference shareholders and debenture-holders whose earnings depend on the nominal value).

ADVERTISEMENTS:

In fact, a reconstruction scheme may be beneficial to the equity shareholders by enabling the payment of a dividend on such shares. On this ground, it would be unjust to ask the preference shareholders to accept a sacrifice when the equity shareholders improve their position.

There is, however, one important right which the equity shareholders enjoy. This is control over the affairs of the company. The equity shareholders will not easily give up this right, and hence the reconstruction scheme should keep this in mind.

The equity shareholders may not agree to the conversion of preference shares or debentures into equity shares even if the holders of preference shares or debentures are willing to accept lower security for their holdings.

The equity shareholders may agree to this only if there is a threat of the company being would up (in which case they will lose almost all). It should also be noted that, without the consent of the parties concerned, their liability cannot be increased. For instance, fully paid shares cannot be converted into partly paid shares without the consent of the shareholders.

ADVERTISEMENTS:

The requirements of working capital must not be overlooked. Cash may be required to pay off certain dissenting creditors or even to pay arrears of preference dividend. Generally, therefore, a company under reconstruction will have to raise funds to enable it to pay off such dissenters and to carry on its work smoothly.

Which of the various parties are willing to subscribe more shares will have to be seen. The equity shareholders may like to consolidate their position by buying more shares. Sometimes, outsiders are willing to subscribe to the shares but they will generally prefer to do so if they are given a controlling share.

Step:

(1) First of all the total amount to be written off should be ascertained. This would mean totalling up the debit balance of the profit and loss account, all fictitious assets like goodwill, preliminary expenses, discount or commission on shares or debentures, any fall in the value of assets, any increase in liabilities and arrears of dividends on cumulative preference shares.

ADVERTISEMENTS:

If the value of any asset can be legitimately increased, the amount of the loss would then be reduced accordingly.

The other way to get at the same figure would be to add up the present value, as a going concern, of all the assets and deduct therefrom the amount of liabilities and also the arrears of dividends on cumulative preference shares. What is left is “net assets”. The share capital compared with net assets will show how much amount is to be written off.

(2) The question now arises as to who is to bear the loss. If the net assets are more than the preference share capital, it is obvious the whole of the loss will have to be borne by the equity shareholders—the nominal value of the equity shares should be reduced by a sufficient margin to cover the loss.

If the net assets are not sufficient to cover the preference share capital (or if the net assets are just sufficient), the preference shareholders will have to accept a sacrifice, although their sacrifice will be smaller than that of the equity shareholders (Equity shares must not be completely wiped off).

ADVERTISEMENTS:

If the future earning power of the company permits, the dividend rate should be increased so that, in terms of rupees, the dividend remains unchanged. Thus if 10.5% preference shares of Rs 100 are converted into preference shares of Rs 75 each, the rate of dividend should be raised to 14%, if possible. In both cases then, the dividend will be Rs 10.5 per share.

(3) Payment of arrears of dividend (question arises only in case of cumulative preference shares) in cash immediately may present difficulties. In such a case, a good method is to issue deposit certificates.

This is preferable to issuing shares because (a) it will not upset the voting power and (b) the certificates can be redeemed as soon as opportunity arises. The rate of interest need not be heavy; but, of course, it will depend on the future earning capacity of the company.

(4) Debenture-holders and other creditors are affected by the reconstruction scheme only if the total assets of the company are insufficient to cover even the liabilities (although their consent will be necessary to any scheme that may be formulated).

ADVERTISEMENTS:

In such an eventuality, the creditors (including debenture-holders) will have to accept sacrifice unless they think that by sending the company into liquidation they will be able to realise substantial portion of then- claims.

The shareholders, both preference and equity, will have to accept a heavy reduction in the value of shares but they cannot be expected to agree to a complete wiping off of the shares, in which case they will have no interest in keeping the company going.

Generally, the sacrifice to be borne by the creditors will be as follows:—

Preferential Creditors Nil

(according to law)

Secured Creditors -Depending upon the value of the security

ADVERTISEMENTS:

Unsecured Creditors – Heaviest.

In short, the whole scheme should broadly depend upon the expected earning power and upon the position as is likely to obtain if the company is sent into liquidation.

Internal vs. external reconstruction:

Having decided who is to bear how much sacrifice or loss and having settled the broad details of the scheme, an important question remains to be decided. Will the reconstruction be internal or external? Internal reconstruction means that the scheme will be carried out by means of reduction of capital, i.e., by getting the approval of the Court.

External reconstruction means that the scheme will be carried out by liquidating the existing company and incorporating immediately another company (with the name only slightly changed such as A B (2009) Ltd. instead of A B Ltd. to take over the business of the outgoing company. There are advantages in both, but generally internal reconstruction is preferred.

The advantages in its favour are:—

(a) Creditors, specially bank overdraft and debenture-holders, may continue whereas they may not if the company is formally liquidated which will involve payment of claims to outsiders. If they do not continue, the company may suffer from want of financial assistance. This is, however, only academic since no reconstruction scheme, even internal, will be really formulated without the consent of the bank, debenture-holders, etc.

(b) The company will be able to set off its past losses against future profits for income-tax purposes. This will materially reduce the income-tax liability depending on the losses suffered during the preceding eight years. Losses can be carried forward for eight years provided the business is carried on.

The business will technically end where the company is liquidated. Hence, in case of external reconstruction, losses cannot be carried forward for income-tax purposes.

The arguments in favour of external reconstruction are as under:—

(a) External reconstruction may be the only way to bring about speedy reconstruction because sometimes a few people hold up the scheme by delaying tactics by means of legal objections.

(b) It may help in raising more finance by issuing to the existing shareholders partly paid shares in the new company. It should be remembered that in internal reconstruction fully paid up shares cannot be converted into partly paid up shares unless every shareholder gives his assent in writing.

This may prove cumbersome. However, it shareholders are willing to accept partly paid shares in the new company, there is not much reason why they should refuse to buy new shares under a scheme of internal reconstruction.

Legal position as regards external reconstruction:

Section 494 of the Companies Act permits the liquidator of a company to transfer the whole or any part of the company’s business or property to another company and receive from the transferee company (by way of compensation or part compensation) shares etc. in the transferor company for distribution among the shareholders of the company under liquidation.

The liquidator must obtain the sanction of the company by a special resolution. Any sale arrangement it pursuance of this section is binding on the members of the transferor company.

But a shareholder who has not voted for the special resolution may, within seven days of the resolution, serve a notice on the liquidator expressing his dissent and requiring the liquidator either, (a) to abstain from carrying the resolution into effect, or (b) to purchase his interest at a price to be determined by agreement or by arbitration.

Illustration 1: (40)

United Industries Ltd., which has suffered heavy losses in the past considers that the worst is over and that, on a sound re-organisation, it will be able to carry on business successfully, profits in future being expected to be between Rs. 2,25,000 and Rs. 2,70,000 (before providing for interest but after charging adequate depreciation).

The Board of Directors of the company ask you (i) to draft a scheme of internal reconstruction which would be equitable to all the parties, (ii) to detail the journal entries to be made after all the formalities have been complied with, and (iii) to reframe the Balance Sheet.

The following particulars are supplied to you:—

Against these assets the liabilities amount to Rs 36,80,000. If the company goes into liquidation, the tax liability will be payable in full leaving Rs 19,00,000 for debenture holders who have a floating charge, the debenture holders will suffer a loss of Rs 8,60,000. Trade payables and the shareholders, both preference and equity, will get nothing. The loss suffered by the debenture holders may even be greater because, due to forced sale, the value of their security may be much less.

The debenture holders should agree to accept a substantial sacrifice in view of the loss that they will surely suffer if the company goes into liquidation. In view of expected profits in future, the rate of interest should be raised as a consideration for reduction in their claim.

Trade payables who stand to get nothing, if the company goes into liquidation, should accept a heavy reduction in their claims. The heaviest sacrifices will have to be made by the shareholders.

The total amount to be written off is as follows:—

To this, two years’ dividend on Cumulative Preference Shares should have been added but in view of the heavy sacrifice that the preference shareholders have to make, they should agree to waive payment of arrears of dividend. It is recommended that the following reductions should be made:

The rate of interest on debentures should be raised to 12% and the dividend on preference shares to 14%, This will partly compensate the sacrifices made by them. If the scheme is accepted, the future distribution of profit on the basis of the minimum profits of Rs 2,25,000 will be as follows;

This would enable a dividend of 28.2% to be paid on equity shares. This seems rather unreasonable for the trade payable who have made a sacrifice of 80% of their claims (equal to the preference shareholders).

They are the worst sufferers, since other parties have slightly improved their position in respect of yields. It is recommended that for five years at least a sum equal to the equity dividend should be set aside out of profits to restore the claims of sundry creditors partially.

Income-tax has been ignored, since, for at least a few years, the company will be able to avoid payment of tax due to past losses. Later, the company may be able to improve its earning power. There is also no need to take any steps to augment the working capital.

The cash and bank balances of Rs. 1,20,000 should be sufficient. An internal scheme should be adopted in order to take advantage of past losses for income-tax purposes.

The entries, if the scheme is accepted, will be as follows:

Illustration 2: (41)

The Balance Sheet of that a Ltd. as on 31st March, 2012 as follows:

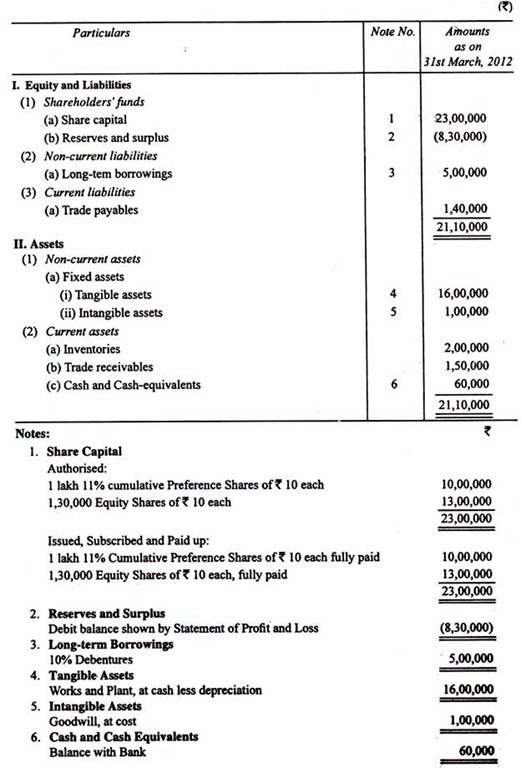

(Preference dividends are in arrear for two years and are payable on liquidation automatically). It is believed that net profits in future will average 10% of the capital employed (after taxation). The Works and Plant is worth Rs 15,00,000 (Rs 10,00,000 if it has to be sold). Inventories are worth their stated value but among the trade receivables there are doubtful debts to the extent of Rs 30,000 (expected to realise 33.33%).

A recapitalisation being desired, you are requested to frame an external scheme of reconstruction.

The assets cover the debentures and creditors amply and hence there is no question of their accepting any sacrifice. After paying the debentures and creditors, a surplus of Rs 12,50,000 would remain which would cover the preference shareholders—but not if the company is forced into liquidation.

Hence, the preference shareholders should agree to a reduction of their capital by 20% or Rs 2,00,000 in all. They should accept preference shares of the total value of Rs 8,00,000 in the new company.

(b) The total loss to be written off is Rs 12,70,000 made up as follows;

As suggested above, the preference shareholders should agree to a sacrifice of Rs 2,00,000. The remainder of the loss, viz., Rs 10,70,000, i.e., 12,70,000 – 2,00,000, will have to be borne by the equity shareholders. If the shares are reduced to Rs 1.50 each, the equity share capital will be Rs 1,95,000 and a sum of Rs 11,05,000 will become available. After wiping off the various losses, a sum of Rs 35,000 can then be placed to Capital Reserve.

The preference shareholders should be compensated by the rate of dividend being raised to 14%. It will mean yearly dividend Rs 1,12,000, a little more than the existing yearly dividend of Rs 1,10,000. The arrears of preference dividend, Rs 1,20,000, will have to paid. Since Theta Ltd. does not have sufficient funds the liability will have to be taken over by the new company and then paid by it.

2. The Scheme.

(a) A new company. New Theta Ltd., should be floated with an authorised capital of 75,000 Equity Shares of Rs 10 each and I Lakh 14% Preference Shares of Rs 10 each.

The company should take over the following assets of Theta Ltd. at the values stated;

It should assume the liability to Trade payables and the liability to preference shareholders in respect of arrears of dividend, and issue the following:—

(i) 10% Debentures, Rs, 5,00,000 (in debentures of Rs 100 each) for distribution amongst Debenture-holders of Theta Ltd.

(ii) 14% Preference Shares, of Rs 8,00,000 (in shares of Rs 10 each) for distribution amongst preference shareholders of Theta Ltd.

(iii) 19,500 Equity Shares of Rs 10 each, fully paid for distribution amongst equity shareholders of Theta Ltd. This will leave a capital reserve of Rs 35,000.

(b) The company will require additional cash as follows: