Target costing is a structural approach to determine the cost at which a proposed product with specified function and quality must be produced, to generate a desired level of profitability at its anticipated selling price.

In other words, Target Costing is a cost management tool for producing overall cost of product over its entire life cycle with the help of the function engineering and research and development. Target cost is called estimated cost of the product that helps a manufacturing unit to remain.It competes in the market in the long run.

Contents

- Introduction to Target Costing

- Meaning and Definitions of Target Costing

- Origin of Target Costing

- Concept of Target Costing

- Objectives of a Target Costing System

- Features of Target Costing

- Characteristics of Target Costing

- Steps Involved in Target Costing

- Stages in the Process of Target Costing

- Steps for the Installation of a Target Costing Approach

- Process Involved in Target Costing

- Phases of Target Costing

- Approaches of Target Costing

- Comparison between Traditional Cost Management Approach and Target Costing Approach

- Difference between Target Costing and Standard Costs

- Techniques of Target Costing

- Benefits of Target Costing

- Advantages of Target Costing

- Limitations of Target Costing

What is Target Costing? – Introduction, Meaning, Origin, Concept, Objectives, Features, Steps, Process, Phases, Techniques, Advantages, Disadvantages, Limitations, Process and Example

Target Costing – Introduction

Target costing is a cost management technique. Target cost is the difference between target sales minus target margin. It is, thus, the difference between estimated selling price of a proposed product with specified functionality and quality and the target margin.

ADVERTISEMENTS:

The technique aims to produce and sell products that will ensure the target margin. While designing the product, the company needs to understand what value target customers assign to different attributes and different aspects of quality of the product.

Intensive marketing research is a must to know preference of the customers and the value assigned by them to different attributes and quality parameters. The organisation works within the limits set by maximum attributes and quality which it can offer and the minimum acceptable to target customers.

In other words, target costing can be defined as a cost management tool for reducing the overall cost of a product over its product life cycle. This pricing technique is utilised to meet the demands of customers on one hand and organisation’s profit goals on the other. Under traditional costing, cost is determined on the basis of product design, then, a profit figure is added to it to establish a price.

However, under target costing, the selling price is set first and then target profit is subtracted from it to finally reach a target cost. The cost figure obtained traditionally is implemented and if found higher, reworking of production processes takes place and costs are tried to be adjusted accordingly. In contrast, costing information is utilised under target costing and the focus is on best possible price upfront.

ADVERTISEMENTS:

The decision-making process involves a cross-functional team consisting of employees from various departments who are entrusted with the task of determining an acceptable market price and corresponding return on sales as well as feasible cost in which a given item may be manufactured.

For reducing costs, the team members concentrate on elimination of non-value added costs of processes, improvement of product design and modification of methods of processes.

The emphasis of target costing is on cost reduction during planning and design stage of the product life cycle as most of the product cost is determined at this stage. The allocation of total cost is more to the development stage under target costing and costs are reduced simultaneously during the process of production.

Cost-engineering techniques are applied in the process of cost reduction. Just-in-time approach, total quality control, value analysis also termed as value engineering etc. are some of the important methods used.

ADVERTISEMENTS:

Cooper defines target costing as “a disciplined process for determining and realising a total cost at which a proposed product with specified functionality must be produced to generate the desired profitability at its anticipated selling price in the future”.

Target costing is a disciplined process in the sense that it uses data in a logical series of steps to determine and achieve a target cost for the product.

Moreover the price and the cost both are for a specified product functionality, which is determined by understanding customers’ needs and willingness to pay for each function. There is an inherent recognition that there are sufficient variables in the process essentially beyond the control of organisation – marketplace decides the selling price, meaning thereby the global customers, competitors and general economic conditions.

Another variable also, is the profit desired which is again beyond the control of the organisation. It is influenced by stakeholders’ expectations and financial markets, competition within the industry etc.

ADVERTISEMENTS:

The external variables are required to be balanced to develop a product at a cost which is within the given constraints.

Target Costing – Meaning and Definitions

Target costing is a pricing method used by firms. It is defined as “a cost management tool for reducing the overall cost of a product over its entire life-cycle with the help of production, engineering, research and design”.

A target cost is the maximum amount of cost that can be incurred on a product and with it the firm can still earn the required profit margin from that product at a particular selling price. Target costing involves a particular selling price. It involves setting a target cost by subtracting a desired profit margin from a competitive market price.

Target costing is known as product costing also. It is a new approach and Accountants in business concerns today are shifting from traditional cost approach to product costing approach, which considers initial design and engineering costs as well as manufacturing cost, cost of distribution, and cost of sales and services. This concept is widely used in Japan.

ADVERTISEMENTS:

CIMA – “Target cost is a product cost estimate derived from a competitive market price”.

“Target costing is a structural approach to determine the cost at which a proposed product with specified function and quality must be produced, to generate a desired level of profitability at its anticipated selling price.”

Target costing is a cost management technique which is very much helpful to any organisation in an increasingly competitive situation. It is helpful in reducing the product life cycle cost also.

In the context of pricing in competitive world, it is always used to reduce cost through its continuous improvements and replacement of technologies and processes. Generally cost of any product is calculated on the analysis of the best structure of the leading competitor in the country.

ADVERTISEMENTS:

On the basis of market price, the basis of target cost are fixed. A target price is the estimated price of a product, which shall be payable by a potential customer. This estimate is based on the understanding of customer. Target price can be found out by deducting target income per unit from its target price.

Thus, Target cost per unit = Target Price – Target operating income per unit.

Target income is that income which a company aims to earn. Target cost per unit is the estimated long run cost of a product and the company tries to achieve its target income, when the product is sold out on target price. In target cost calculations, all future fixed and variable cost are included, because in long run, the company must cover all its costs.

Target price are determined by adding profit to the cost. Efforts are made to strike towards the target cost. For this purpose cost accounts Department, Product Development and Engineering Department work together.

ADVERTISEMENTS:

If target cost cannot be attained, then efforts are made to reduce the cost by redesigning and simplifying the product and by changing the methods of production. In this connection, non-essential products are estimated. It is a technique, on the basis of which cost reduction and profit planning can be made.

Computer aided manufacturing international (CAM) defined, ‘a market based cost that is calculated using sales price necessary to capture a pre-determined market price” (is known as target costing).

Kenneth Crow, President of DRM Associates, has mentioned in his article ‘Target Costing’, ‘Until recently, engineers have focused on satisfying consumer’s requirements. Most development personnel have viewed a product’s cost as a dependent variable that is the result of the decisions made about a product’s functions, features and performance capabilities. Because a products costs are not often not assessed until later in the development cycle.’

From the above definition it is clear that a target cost is the maximum manufacturing cost for a product which is arrived at by subtracting its required margin on sales from the expected market price. So target costing is market driven design methodology.

Thus target costing is a tool for cost management which helps in reducing the cost of product over its entire life cycle.

Target Costing – Origin

It emerged in Japan in 1960s as the response to difficult market conditions. A proliferation of consumer and industrial products of western firms were overcrowding the market in an Asia, Japanese companies were also experiencing shortage of resources and skills needed for the development of new concepts, tools and techniques, which were required to achieve parity with the toughest western competitors in-terms of quality, cost and productivity.

ADVERTISEMENTS:

In Japan, target costing is widely practiced in more than 80% of the companies in the assembly industries and more than 60% of companies in processing industries.

Target Costing – Concept

Generally, in traditional method, price decisions were based on standard. Competitors are emerging and the business for competition inflows other areas as cycle time, quality, reliability. The traditional method standard costing is not effective in longer period for cost reduction. In order to remove the drawback of traditional method, the New Method of Costing is introduced.

In the modern days, fast growing industries use target costing approach moves the decision perspective from book keepers office to the market. So growing companies are turning equation around and setting cost id prices.

Target costing has been derived from a Japanese term “Gena Kikaku.” Concept of target costing was developed in Japan around 1970.

Determination of the price at which they can sell the new product or service and then design a product or service which can be produced a low to provide an adequate profit is called target costing.

In other words, Target Costing is a cost management tool for producing overall cost of product over its entire life cycle with the help of the function engineering and research and development. Target cost is called estimated cost of the product that helps a manufacturing unit to remain.It competes in the market in the long run.

In competitive industries, a unit selling price is set independent of the initial of the product. If target is lower than the initial forecast of product cost, manufacturer derives the unit cost to come down over a definite period that it should compete.

Target Cost is ascertained by deducting desired fit from pre-determined sales price as shown below –

Target cost = Sales price – Desired profit

In this case sales price is one which is appropriate for a targeted Market share. Desired profit is the contribution that the product makes towards the enterprise’s business sustaining costs. The residual cost is target cost.

Target costing is based on marketing factor (i.e. sales price at which customers would buy the product is to be set first and then costs would be adjusted) which has led to market driven approach to cost accounting.

Target costing is influenced by a number of external market factors. A target market price is determined by marketing managers, before designing and introducing a new product in the market.

In short, in target costing, the cost of product is first estimated and then designed the product to meet that cost. It is used to motivate and encourage all the departments engaged in design and production, so that they find less expensive ways of achieving better product and features.

Top 3 Objectives of a Target Costing System

Broadly speaking, a target costing system has three objectives:

1. To lower the costs of new products so that the required profit level can be ensured.

2. The new products meet the levels of quality, delivery timing and price required by the market.

3. To motivate all company employees to achieve the target profit during new product development by making target costing a company wide profit management activity.

Top 5 Features of Target Costing

The features of target costing are as follows:

1. It is viewed as an integral part of the design and introduction of new products.

2. A target selling price is determined using various sales forecasting techniques.

3. The target selling price is the establishment of target production volumes, given the relationship between price and volume.

4. Target costing process is to determine, cost reduction targets.

5. A fair degree of judgement is needed where the allowable cost and the target cost differ.

5 Main Characteristics of Target Costing

The main characteristics of target costing system are as under:

Characteristic # (1) Identification of Opportunities –

With the help of value engineering and value analysis, opportunities, for cost reduction can be identified easily. Value engineering involves searching the opportunities to modify the design for reducing the cost without reducing the quality of the product.

Similarly, value analysis involves rejecting non-value adding activities which may minimise the cost without reducing quality of the product. Thus current cost is reduced to the level of target cost. It is presumed that when production commences, the total cost will meet the target and profit also.

Characteristic # (2) Target Cost –

Target cost is decided by deducting target income from the target price.

Characteristic # (3) Integral Part of Design –

Target costing is known as an integral part of the design and introduction of new products.

Characteristic # (4) Target Price –

It is the estimated market price of the product. It is a target price which is determined by using various sales forecasting techniques in which consideration is made for design specifications of the product and competitive market conditions.

Characteristic # (5) Cost Reduction Target –

Cost reduction target is fixed, which requires estimation of current cost of the new product. It is based on existing technologies and its various components. The excess of current cost over target cost indicates the cost reduction.

Main Steps Involved in Target Costing

The following are the main steps involved in target costing:

1) Identify customer’s needs in a way what customer seeks.

2) Determine the target price which customer will be prepared to pay for the product. Deduct the target profit margin from the target price to determine the target cost.

i) Estimate the actual cost of the product.

ii) If the estimated actual cost exceeds the target cost, investigate the ways of reducing the actual cost to the level of the target cost.

iii) Interacting the product design eliminating or reducing unnecessary attributes with costs that cannot be recovered in higher prices until the cost target is met.

iv) Revalidating the validity of the market price of redesigned product.

3) Establishing a cross functional team which is involved in the implementation process from the earliest design stages.

i) Using tools such as value engineering in the design process.

ii) Pushing cost reduction using “Kaizen Costing” once the production started.

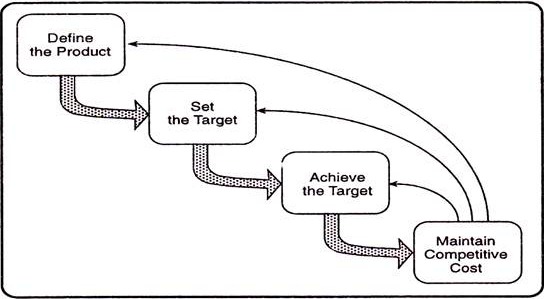

Basic Stages in the Process of Target Costing

The basic stages in the process of Target Costing, which are market-driven, are as under:

Stage # (i) Define the Product –

The questions to be answered are ‘What are you selling and to whom?’ “What do they want it to do?”

Stage # (ii) Set the Target –

The issues to be addressed are “What will they pay for it” and “what should it cost to produce?”

Stage # (iii) Achieve the Target –

It means “how can we get there?” “Are we getting there?”

Stage # (iv) Maintain Competitive Cost –

The focus is on ‘how can we stay ahead’?

The crux of the entire matter is that target cost is the dependent variable. To repeat, market-based price is determined in the first place followed by desired profitability and target cost is simply arrived at by deducting profit from the price.

Steps for the Installation of a Target Costing Approach

Following steps must be taken to install target costing approach to bring in the desired results:

Step # 1. Establishment of Market-Driven Price:

The target price is determined on the basis of market factors, e.g., company’s status in the market, marketing strategy, competitive price structure, anticipated market share as per demand forecasting etc. Customer’s willingness to pay is of utmost significance.

Step # 2. Determination of Target Cost:

After establishing the target price, target cost is worked out by deducting standard profit margin from the price – The target cost is allocated down to lower levels in a manner consistent with the structure of teams or individual responsibilities.

Step # 3. Balancing of Target Cost with Product Requirements:

Before finalising the target cost, product requirements are also required to be considered. Product requirements or specifications must be set by thorough analysis of customers’ choices and preferences, use of conjoint analysis to understand the value customers put for the product and application of other techniques to match product requirements with target cost.

Step # 4. Setting up of Target Costing Process:

A well-defined process which integrates activities to support target costing needs to be set up. Early and proactive consideration of target costing is required and for it various tools and techniques are used.

Step # 5. Establishment of Coherent Organisational Structure:

An organisational structure which integrates cross-functional disciplines, e.g., marketing, production, engineering, purchasing, finance etc. is desired to be established in which there is a clear demarcation of authorities and responsibilities in order to have coherence and complete coordination.

Step # 6. Re-Orientation of Culture and Altitudes:

Mindsets of people are also very important to be reoriented so that they don’t resist to an approach in which reverse methodology of cost determination is applied and the entire team is asked to work accordingly to reduce cost on one hand and improve quality on the other – which appears, prime facie, to be self-contradictory.

Step # 7. Analysis of Alternatives:

Once voluntary support to the approach is developed within the organisation, different alternatives automatically crop up in the minds of those involved in the process. Various alternatives can be chalked out, properly evaluated and then decisions taken to achieve the goal. For evaluation and decision making, a number of quantitative tools are also available now which will yield fruitful results.

Step # 8. Methodologies:

Methodologies for implementation of target costing system include guidelines, databases, training, procedures and supporting analytic tools. Different tools and methodologies may be used to design for manufacturability, design for testing and inspection, standardisation of products etc.

Step # 9. Reduction of Overhead Costs:

Since overhead cost forms a substantial part of the total cost, it also needs to be focused upon by examining them, re-engineering the processes and minimising non- value added costs. Activity-based costing may also be used for allocation of indirect costs which is more rational than traditional costing system.

Step # 10. Measurement of Results:

Current estimated costs must be compared with the target costs – the comparison should be on a continuous basis and at each and every stage of production. Review of costs may also be required at times.

Similarly actual costs are also required to be put against target cost and causes of variations explored to take suitable corrective action. This way, the concepts of standard costing and budgetary control need to be applied though target cost is different than the standard cost and the budgeted cost.

Process Involved in Target Costing

The process of target costing involves:

1. Establishing the target price in the context of market needs and competition;

2. Establishing the target profit margin;

3. Determining the allowable cost that must be achieved;

4. Calculating the probable cost of current products and process;

5. Establishing the target amount by which current costs must be reduced.

Target Costing Phases – Planning, Development and Production

Target costing is a market driven methodology.

There are the three phases of this methodology as under:

(i) Planning –

The products of all competitors are to be analysed with regard to price, sales, quality, technology, and service etc., and after that target cost is to be determined and then market share of one product is to be finalised.

(ii) Development –

Cost structure of the organisation is to be finalised after examining and studying various cost reductions measures and Activity based costing and then a suitable design has to be developed.

(iii) Production –

Production target are fixed and efforts are made to achieve it at the lowest cost without affecting the quality, technology design and its production techniques etc.

Target Costing – Approaches (With Equations)

Target costing system has customer orientation. Under the target costing approach, before a firm launches a product (or a family of products), it determines the ideal selling price, establishes the feasibility of meeting that price, and then control costs to ensure that the price is met.

The target costing approach is radically different from the conventional approach for price fixation and cost management.

1. Conventional Approach:

The conventional approach is cost plus pricing. The approach is to design a product so that it can be produced at the lowest cost, and then a desired margin is added to the estimated cost to determine the selling price of the new product.

We may present this approach in an equation form as follows:

S = C + P

If the firm feels that the price is too high, it modifies the design to reduce the cost and consequently the required selling price. If the firm could not establish the expected selling price, the product is launched at the originally estimated selling price based on the original design.

The other conventional approach is to design a product so that it can be produced at the lowest cost, and then match the cost to the anticipated selling price.

The profit margin is determined as presented in the following equation:

P = S-C

If the profit margin is below an acceptable level, the product is redesigned, if possible, to reduce the cost until the desired profit margin is achieved.

In both the conventional approaches, the focus is on cost reduction and not on cost management. The cost reduction efforts start after the development stage. Both the approaches induce production efficiencies to apply after the product design stage. Therefore, the potential for cost reduction is limited.

A study estimated that at most 10% cost reduction is attainable. Conventional approaches do not compel managers to estimate how much the customer will pay for each element of functionality and quality. Each product used to be conceived as a package of functionality and quality without much scope for modification.

2. Target Costing Approach:

Under the target costing approach, firms work backward from customers’ need and willingness to pay. Target costing takes cost as the dependent variable, while conventional approaches take selling price or profit as the dependent variable.

The relationship between the variables can be presented as follows:

C = S-P

The target costing approach recognizes that there is a trade-off between price, cost, functionality, and quality. Managers examine this trade-off at the development stage of the product, and optimize on the product functionality and quality within the parameters of estimated selling price, target cost, target volume and target launch date.

Structured Product Development Discipline:

Target costing is a highly structured product development discipline, which involves understanding customers’ needs, industry pricing dynamics, product complexity and life cycle analysis, and supplier relations.

Target costing system requires mapping of different customer segments, and the cost and revenue analysis provides information to identify the most attractive segment in terms of margin. The product development and design team determines the best bundle (in terms of margin and pre-determined target cost) of functionality and design, which will be successful in a particular segment.

An example of the application of the target costing approach is Tata ‘Rs 0.1-million car’. Business Week has named Rs 0.1 million car as one of the trendsetters of 2007, while Ratan Tata has been listed among the world’s ‘Most Important People’ of the year. The car will be unveiled on 10 January 2008.

Comparison between Traditional Cost Management Approach and Target Costing Approach

Under Traditional Cost Management Approach, cost of a product is treated as a dependent variable resulting from the decisions made about functions, features and performance capabilities of the product. The costs are generally higher than desired since the assessment of cost is quite late in the development cycle.

On the other hand, target costing approach is quite different.

Three pillars on which pyramid of target costing is built are –

(i) product orientation towards customer affordability in other words, market- driven pricing

(ii) treatment of product cost as an independent variable and

(iii) Efforts made for achieving target cost during the development phase of the process at the initial stage itself.

Difference between Target Costing and Standard Costs

The difference between target costing and standard costs are as follows:

One should not get confused with target costing and standard costs as one and same. There is the difference between the two terms.

Standard costs are predetermined costs setup on the basis of internal analysis of normal conditions by industrial engineers or cost accountants.

On the other hand, target costs are based on external analysis of markets and playing competitors.

Target Costing – Top 7 Techniques Discussed

Target Costing takes help of various quantitative techniques in a large measure, though non-quantitative methods are also used.

These have been discussed below:

1. Value Analysis:

Concept of Value:

It may not be out of place here to understand the meaning of the term ‘value’. As a matter of fact, the term ‘value’ has different meanings for different persons. For example, for a designer the “value” means the quality of the product, for a salesman the term ‘value’ means the price which he can fetch for the product in the market, and for the top management the term ‘value’ means return on capital employed.

However, an industrial product may have the following concepts of value:

(i) Use Value:

This refers to the characteristics which the products should possess to provide a useful service for which it is intended. For instance, a watch is meant for indicating time. In case it gives fairly correct time, it is giving its full use value.

The use value is measured in terms of quality of performance. In order to decide whether a product is giving value for the money spent on it, it will be appropriate to divide its worth for the concerned person by the price paid for it.

A product may perform several functions.

Accordingly, its use value can be divided into three categories:

(a) Primary use value;

(b) Secondary use value; and

(c) Auxiliary use value.

For instance, paint has different use values. It has primary use value when it is applied to protect some surface. It has a secondary use value when it is used for marking lines on the road for crossing by pedestrians.

It has an auxiliary use value when it pleases aesthetic sense. Such a functional classification would help one in identifying which paint one should use keeping in mind the objective. If this is not done, perhaps one may use costly enamel paint where use of ordinary paint would have been prudent.

(ii) Cost Value:

The value is measured in terms of cost in case the product is manufactured in the organisation. It refers to the cost of production. In case a product is procured from outside, it refers to cost of its purchase.

(iii) Exchange Value:

It refers to sales value which a product would fetch. It is important for the sales department since the profit is excess of the selling price (i.e., exchange value) over the cost of the product.

Hence, the sales department must ascertain what value the product has for the customers as compared to competitive products available in the market. It will help in advising the management in fixing the selling price of the product.

(iv) Esteem Value:

This may also be referred to as the prestige value. Certain products or articles have value simply because of their attractiveness or esteemed features. A watch made of gold has an esteemed value for its owner, though its utility is not more than that of an ordinary watch. For some people, purchase of a gold watch may be a waste. However, it commands a value for the person who wishes to impress upon others and thus have a personal satisfaction.

Also termed as value engineering, the approach focuses upon improvement in value by resulting in a careful and in-depth study of products at the stage of their designing. The different components can be redesigned or standardised. Less costly manufacturing processes or methods may also be used.

Such a study reveals the fields which involve avoidable costs and after locating these areas, steps can be taken to eliminate or if not possible reduce such unwanted costs, of course, without in any way compromising on quality.

Following points deserve consideration before embarking upon value analysis in order to critically examine each and every product and its part:

(a) Exact function of the item must be identified and its significance evaluated.

(b) Cost-benefit analysis of the item must be carried out.

(c) The aspect of standardisation should be seriously looked into.

(d) The requirement of redesigning should be assessed in order to have durability.

(e) Economics of labour etc. should also be measured.

(f) Redesigning may be adopted if it results in lower costs.

(g) Combination of activities, items or segregation should also be considered to reduce costs of incentives etc.

2. Total Quality Control:

It is a Japanese process developed as a method of quality control. Total quality control also incorporates inspection activities regarding quality throughout the organisation, rather than within specific departments.

3. Just in-Time Material Requirement Planning and Economic Order Quality Analysis:

In contrast to the traditional method of keeping certain inventories on hand, firms started using techniques of cost minimisation-Just in-time approach, material requirement planning and determination of economic order quantity are some of such techniques which are helpful in reducing the costs of material and thus the product.

4. Analysis Methods for Defining Product:

Some of these are market analysis, competitor analysis and mapping the product to the market. Market feature table can be prepared for the purpose.

The purpose of drawing the above table is to map the features desired by different market segments at one place. It helps in concentrating on really material features or functionalities at a high level market for the potential product is divided into “natural” market segments – which may be as per geographical areas, customers’ types of business, customers’ affluence etc.

The features desired by each market segment are classified into three categories:

(i) Basic –

These are desired by all customers in the segment, that they are all willing to pay for.

(ii) Step-up –

These are additional or optional features desired by a few customers in the segment who are willing to pay a higher price for them.

(iii) Premium –

Further additional features are demanded by a very few high class customers who are ready to pay even a premium price.

The market size in each category has also been mentioned in the chart by way of number of potential units that can be sold or by potential revenues. The real life examples of such goods are passenger cars, writing pens and a number of other consumer durables. Specific market share can be captured by catering to the needs of the customers identified in such cases, since the target price shall be higher, higher target cost does not matter. However, by and large, the basic product meant for a chunk of consumers will have to be sold at a lower price, thereby target costing assumes greater significance for the general market segments.

5. Methods for Establishing Market Price – Experience Curves or Learning Curves:

Under this approach, historical market price of the product is plotted as a function of the industry’s cumulative sales of that product. If there is a straight line, it is a very reliable predictor of prices in the short run.

In ‘More than curve’, if product is cellular telephone network equipment, the price of the equipment divided by number of subscribers that it can serve shall be plotted vis-a-vis the cumulative number of cell-phone subscribers in the world.

6. Activity-Based Costing to Determine the Cost:

After determining the overall target cost, cost targets for each of the components, subsystems and elements that go into making up the set of total costs to be included are found out. For the same, value engineering can be applied here. A matrix is created which relates different product features to the various elements making up the product.

ABC analysis of material control can be applied to know which elements require greater attention to be paid in the efforts to reduce costs.

7. Brainstorming Techniques:

Think tanks and think banks can be developed to generate fresh ideas and out of the box solutions to the vexed problems. The team of genius people from different fields, which may include even workforce, suppliers, outside experts etc., can have brainstorming sessions to ponder over the problem areas and propound new ideas for cost reduction.

There is a need for continuous product improvement and constant cost reduction. Once the product is introduced and accepted in the market, prices automatically tend to decline. The profitability increases as a result of stepped-up sales, even at lower profit margin levels.

Thus target costing is an effective method for ensuring that the organisation has profitable products well matched to its customers’ requirements. The entire process is quite simple, logical and easy to implement. The key issues are to be focused upon – it helps bringing different parts of the organisation in one beard.

Benefits of Target Costing

1. It helps to reduce the development cycle of a product.

2. It helps to eliminate waste, reduce non-value added activities.

3. It helps to increase the profitability of the new products.

4. It helps to control costs.

5. It helps to reduce the cost of products.

6. It encourages in team work among all internal organisations.

7. It helps to ascertain detail information about the costs involved in.

8. Manufacturing of new product.

Target Costing – Advantages

The main advantages of target costing are as under:

(1) Positive Impact on Profitability –

Target costing has positive impact on profitability of the organisation, throughout the life cycle of every product.

(2) Company Competitive Future –

This costing helps to create the competitive future of any company as the product is designed and manufactured as per requirements of the market.

(3) Top to Bottom Commitment –

It reinforces top to bottom commitment to process and product innovation and is aimed at identifying issues.

(4) Valuable Edition to Life Cycle –

This costing can be used as a valuable addition to the life cycle products.

(5) Management Control System –

It uses management control system to support manufacturing strategies and to identify market opportunities, which may be converted into real savings to achieve the best value.

Some of the other advantages are:

1. It helps in assuring that products are better matched to their customer’s needs.

2. It assists in aligning costs of features with customer’s willingness to pay for them. In the process quality stands improved.

3. It supports reduction of development cycle of the product.

4. It is useful for reduction of costs of products substantially

5. It inculcates better team-spirit among all internal organisations associated with conceiving, marketing, planning, developing, manufacturing, selling and distributing a product.

6. It helps in engaging customers and suppliers to design the right product and to more effectively integrate the entire supply chain.

7. It adds value to the production process by eliminating non-value added activities, paving the way to pass on the benefit of decreased cost to the consumers.

Target Costing – 3 Major Limitations

The major limitations of target costing are as under:

(1) Lack of Consensus –

It is very difficult to reach to a consensus on the proper design of the product, because the opinion of the design team members may vary.

(2) Lengthy and Time Consuming –

This system is lengthy and time consuming process. This delay may lead to serious cost over runs.

(3) Cost Cutting –

A large amount of mandatory cost cutting may result in finger printing in many parts of the company. It may bring savings in one part, while there may be cost reduction in some other parts.

Target Costing: Origin, Definition, Steps, Objectives, Process, Advantages and Problems

1. Origin of Target Costing:

In Japan, target costing is has gained importance and widely practiced in more than 80% of the companies in the assembly industries and more than 60% of the companies in processing industries. It emerged in Japan in 1960s as a consequence of difficult market conditions. A proliferation of consumer and industrial products of western firms were overcrowding the markets in Asia.

Japanese companies were also experiencing shortages of resources and skills needed for the development of new concepts, tools and techniques, which were required to achieve parity with the toughest western competitors in terms of quality, cost and productivity.

Many Japanese companies considered modified cross-functional activities, as used by western firms for manufacturing. They believed that good results can be achieved by combining employees from strategy, planning, marketing, engineering, finance and production into expert teams.

These teams were able to examine new methods and techniques for the design and development of new products and aimed at increasing the degree of integration between upstream and downstream activities of a firm’s operations. Target costing thus emerged from this background.

A range of specialized tools, including functional analysis, value engineering, value analysis and concurrent engineering were introduced to support the target costing. This made Japanese companies particularly effective in the area of product design and development.

They were able to identify all relevant elements to formulate a holistic management approach in order to achieve performance levels to meet the firm’s objective.

2. Definition of Target Costing:

Target costing can be defined as “a structured approach for determining the cost at which a proposed product with specified functionality and quality must be produced to generate a desired level of profitability at its anticipated selling price”. A critical aspect of this definition is that it lays emphasis on the fact that target costing is much more than a management accounting technique.

Rather, it is an important part of a comprehensive management process aimed at helping a firm to survive in an increasingly competitive environment. Target costing is a management technique aimed at reducing a product’s life-cycle costs. A general concept of target costing is discussed here.

Target Costing is a disciplined process for determining and realizing a total cost at which a proposed product with specified functionality must be produced to generate the desired profitability at its anticipated selling price in the future. CIMA defines target cost as “a product cost estimate derived from a competitive market price”

Target Costing is a disciplined process that uses data and information in a logical series of steps to determine and achieve a target cost for the product. In addition, the price and cost are for specified product functionality, which is determined from understanding the needs of the customer and the willingness of the customer to pay for each function.

Target costing is a formal process that attempts to match a proposed product’s features (benefits) with a viable market price that achieves the company’s profitability goals by:

(a) Determining a price point (or range of prices) for an approximate combination of features and benefits.

(b) Subtracting a desired profit from the market price to determine the maximum bearable level of costs.

(c) Iterating the product design—eliminating or reducing unnecessary attributes with costs that can’t be recovered in higher prices—until the cost target is met.

(d) Revising the market price for the redesigned product in view of changed market conditions.

3. Steps in Target Costing:

Following are the main steps (or stages) involved in target costing:

(i) To conduct market research in order to see what products are in the market place, what new products the competitors are trying to bring in the market, to ascertain customers’ requirement and the price they can afford for the product.

(ii) Determining the price, margin and cost feasibility. Target price is determined on the basis of market survey, at which the product can be sold. On the selling price a standard margin is determined to finally come to the cost figure (Target Price − Target Profit = Target Cost).

(iii) To meet margin target by design improvement. If the product designed cannot be produced in the cost range decided, value engineering is used to drive down the product cost to a level, at which target price and margin can be attained.

(iv) To implement continuous improvement. This is needed to ensure that targeted cost levels are maintained subsequent to design phase. Value engineering technique is applied for reduction of waste, misuse, etc. and for elimination of non-value added costs and processes, etc.

4. Objectives of Target Costing:

The fundamental objective of target costing is to enable management to use proactive cost planning, cost management and cost reduction practices whereby, costs are planned and managed out of a product and business, early in the design and development cycle, rather to an during the later stages of product development and production.

It obviously applies to new products, but car also be applied to product modifications or succeeding generations of products. It might also be used for existing products, but costs are more difficult to reduce once a product is developed and designed.

Target costing is primarily used and most effective in the product development and design stage. The costs most typically emphasized in the target costing process are such things as: material and purchased parts, conversion costs (such as labour and identifiable overhead expenses), tooling costs, development expenses and depreciation.

However, all costs and assets that may be affected by early product planning decisions should be considered. This would include more indirect overhead expenses through the production stage, and beyond, such as service costs, and assets like inventory. Target costing is intended to get managers thinking ahead and comprehensively about the cost and other implications of the decisions they make.

Target costing is as much a significant business philosophy as it is a process to plan, manage and reduce costs.

It emphasizes understanding the markets and competition; it focuses on customer requirements in terms of quality, functions and delivery, as well as price; it recognizes the necessity to balance the tradeoffs across the organization, and establishes teams to address them early in the development cycle; and it has, at its core, the fundamental objective to make money, to be able to reinvest, grow and increase value.

Broadly speaking, a target costing system has three objectives:

a. To lower the costs of new products so that the required profit level can be ensured.

b. The new products meet the levels of quality, delivery timing and price required by the market.

c. To motivate all company employees to achieve the target profit during new product development by making target costing a companywide profit management activity.

For any system to be effective in supporting decision making in an organization, the staff from the relevant departments must come together in order to tap their creativity so as to achieve goals. In other words, the company requires a non-conflicting and rational system for consensus building and decision-making.

5. Target Costing Process:

Just as there is no single definition of target costing, there is no single target costing process.

Nevertheless, all companies share a series of general steps:

a. Establishing the target price in the context of market needs and competition;

b. Establishing the target profit margin;

c. Determining the allowable cost that must be achieved; this cost should motivate all personnel to achieve;

d. Calculating the probable cost of current products and processes; and finally,

e. Establishing the target amount by which current costs must be reduced.

Once the target cost has been calculated, companies take the following steps to achieve it:

a. Establishing a cross functional team, which is involved in the implementation process from the earliest design stages,

b. Using tools such as value engineering in the design process; and

c. Pursuing cost reductions using “kaizen costing” once production has started.

A number of techniques and tools facilitate an effective and efficient costing process. Three externally oriented analyses market assessment tools, industry and competitive analysis and reverse engineering provide a firm with a foundation for defining the proposed new product and establishing its price.

The determination of the target profit margin relies heavily on the comprehensive and detailed financial planning and statement analysis. Every firm has relationship between prices, volumes and revenues; costs and investments, in the aggregate and for specific product lines and individual products. The management team should explore other tools like value engineering and quality function deployment.

6. Advantages of Target Costing:

Main advantages of target costing are:

a. It reinforces top to bottom commitment to process and product innovation to achieve some competitive advantages.

b. It helps to create a company’s market-driven management for designing and manufacturing products that meet the price required for the market success.

c. It uses management control system to support and reinforce manufacturing strategies, and to identify market opportunities that can be converted into real saving to achieve the best value for money rather than simply achieving the lowest cost.

d. Assures that products are better matched to their customers’ needs.

e. Aligns the costs of features with customers’ willingness to pay for them.

f. Reduces the development cycle of a product.

g. Reduces the costs of products significantly.

h. Increases the teamwork among all internal organizations associated with conceiving, marketing, planning, developing, manufacturing, selling, distributing and installing a product.

i. Engages customers and suppliers to design the right product and to more effectively integrate the entire supply chain.

7. Reasons for the Late Development of Target Costing:

Although target costing emerged more than 30 years ago, yet only in 1990’s this system came into notice. Main reasons for late popularity of target costing could possibly be that target costing focuses heavily on new product development and Japanese companies which practice the system most are very secretive about their new products/activities.

Also, popularity of Japanese Just-in-time inventory system had dominated the attention of industry in 1980’s and, therefore, target costing got the second seat.

8. Problems with Target Costing:

Talk with customers about a new product concept, find out which features they like and don’t like, and find out how much they would pay. Subtract an acceptable profit margin, and you’re left with the target cost of the product. Now all you have to do is get everyone inside and outside the company to adhere to this number. It sounds simple enough.

It is easier said than done. Yet, target costing-a cost-management process imported from Japan—is helping a few dozen companies in the United States gain an edge by having them listen harder to customers to gauge the right product or service price.

Boeing, Eastman Kodak, and Honda of America, for example, as well as pioneers Daimler Chrysler and Caterpillar, have implemented the strategy, reversing the way they traditionally design, price, and sell new products.

Companies that have implemented the cost-management strategy insist they have boosted profitability. But, although virtually the entire Japanese manufacturing sector has gone the target-costing route since its inception in the 1970s, it hasn’t exactly taken root here in India.

Target Costing has a few problems that one should be aware of and guard against. These problems are as follows:

a. The development of the process can be lengthened to a considerable extent since the design team may require a number of design iterations before it can devise low cost product that meets the target cost and margin criteria. This occurrence is most common when the project manager is unwilling to discontinue a design project that cannot meet its costing goals within a reasonable time frame.

Usually, If there is no evidence, it is better to either drop a project or at least shelve it for a short time and then try again, on the belief that new cost reduction methods or less expensive materials will be available in the near future that will make the target cost an achievable one.

b. A large amount of mandatory cost cutting can result in finger pointing in various parts of the company; especially if employees in one area feel they are being called on to provide a disproportionately large part of the saving.

For example the industrial staff will not be happy if it is required to completely alter the production layout in order to generate cost saving, while the purchase staff is not required to make any cost reductions through supplier negotiations. Avoiding this problem requires strong interpersonal and negotiation skills on the part of the project manager.

c. A design team having representatives from the number of departments can sometimes make it more difficult to reach a consensus on the proper design because there are too many opinions regarding design issues.

For every problem area outlined above the proper solution is retaining strong control over the design team, which calls for a good team leader. This person must have a very good knowledge of the design process, good interpersonal skills, and a commitment to staying within both time and cost budgets for a design project.