The term ‘gearing in a financial context refers to the amount of debt finance a company uses relative to its equity finance. A company with high level of debt component in its capital structure is said to be ‘highly geared and vice versa. The gearing of a company can be calculated with the help of financial ratios like debt-equity ratio (long-term debt / shareholders’ funds), capital gearing ratio (long-term debt/capital employed).

The problems associated with a high level of gearing are as follows:

(a) The profitability and earnings are more sensitive due to changes in interest rates of different debt components.

(b) Highly geared company is subject to higher financial risk.

ADVERTISEMENTS:

(c) There is an increased possibility of bankruptcy risk with high levels of debt in capital structure.

(d) The stock market prices of equity shares of a company will be quoted less if it is highly geared due to high levels of financial and bankruptcy risk.

(e) The long-term planning will be sidelined due to increased pressure of raising cashflow for meeting the interest and principal amounts repayment.

The optimum level of gearing depends upon the requirements of the industry in which a particular company is operating. The interest cover is considered as ratio to ascertain the level of income gearing. While calculation of capital gearing ratio, market values of debt and equity are considered to be more appropriate than book values.

ADVERTISEMENTS:

The firm with low business risk can be able to carry high levels of gearing, since its stability can enable the firm to withstand to high levels of financial risk. In the initial stages of financing with lower levels of debt, the firm’s distributable profits are reduced by the interest payments. Due to tax shield, the net interest payments (i.e., Interest on debt minus tax saving due to interest charge against profits) will enable the firm to trade on equity.

In other words, the earning of return on investment over fixed interest on debt less tax savings, will add up to the profits available to equity holders. The volatility in operating profits will increase financial risk due to firm’s obligation to pay interest and repayment of debt in time.

Therefore, higher levels of gearing cause higher levels of financial risk. If the level of gearing increases, the expected return of equity shareholders will also increase, along with the increase in financial risk and bankruptcy risk due to higher levels of debt component in total capital and the expectation will be more to compensate for taking higher levels of financial and bankruptcy risk.

ADVERTISEMENTS:

Gearing and Cost of Capital:

Empirical evidence shows that over a wide range gearing, the proportion of debt has relatively little impact on the cost of capital.

This is explained in the following illustration: (%)

The above data is represented in figure 28.3. So long as the existing gearing of the company is within the optimum range say 30% to 60%, the proportion of debt in a company’s capital structure has little effect on a company’s cost of capital. A company can operate within this range to maintain the unaffected cost of capital.

Gearing and EPS:

In capital structure decisions, the impact of gearing ratio is viewed on earnings per share. The amount of gearing has considerable effect on the earnings attributable to the equity shareholders. A highly geared firm must earn enough profits to cover the interest on debt before any profits available for distribution to the equity holders.

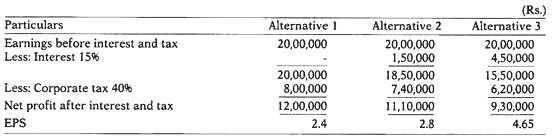

ABC Ltd. is setting a project with a cost of Rs. 50,00,000. It is considering the following three alternatives for financing the project: (Rs.)

ADVERTISEMENTS:

Illustration:

The company’s estimated earnings per year Rs. 20,00,000. The corporate tax is 40%. Calculate the earnings per share in three different alternatives.

Solution:

ADVERTISEMENTS:

Analysis:

We can observe from the above illustration that high levels of gearing leads to an increase in EPS for equity shareholders. But the debt in the capital structure increases the risk of equity shareholders. The increase in debt increases the earnings per share provided that the company must earn profits more than the interest payable on the debt.