After reading this article you will learn about Funds Flow Statement :- 1. Introduction to Funds Flow Statement 2. Concept of Funds Flow Statement 3. Funds Flow Statement 5. Object of Preparing a Fund Flow Statement 6. Parties Interested 7. How to Prepare 8. Funds Flow Statement and Income Statement 9. Funds Flow Statement and Indian Position Thereto 10. Some Practical Hints for Funds Flow Statement.

Contents:

- Introduction to Funds Flow Statement

- Concept of Funds Flow Statement

- Funds Flow Statement

- Object of Preparing a Fund Flow Statement

- Parties Interested of Fund Flow Statement

- How to Prepare Fund Flow Statement

- Funds Flow Statement and Income Statement

- Funds Flow Statement and Indian Position Thereto

- Some Practical Hints for Funds Flow Statement

1. Introduction to Funds Flow Statement:

We all know that the objects of preparing financial statement with the help of Income statement or, Profit and Loss Account and Balance Sheet is to supply the financial information to the users of financial statements as far as possible No doubt, in order to serve such basic objectives, the Income Statement and the Balance Sheet serve very well.

ADVERTISEMENTS:

The Balance Sheet exhibits the financial position at the end of the period through the assets (which show the development of resources in various types of properties) and liabilities (which present how these resources were taken).

The Income Statement, on the other hand, measures the results of the operation at the end of the period, i.e., the change in the owner’s equity as a result of the productive and commercial activities for the period.

Thus, the above two statements are very useful although there are other significant relationship between the two Balance Sheets (opening and closing accounting periods) on which the conventional above two statements cannot throw any light further.

For this purpose, it becomes necessary to know what funds are available during the period and application of such funds along with the profit that has been earned as a result of the business activities. So, in order to know such changes in the financial position, it is necessary to prepare a statement known as Funds Flow Statement which will exhibit such financial information to the users of financial statement.

ADVERTISEMENTS:

2. Concept of Funds Flow Statement:

ADVERTISEMENTS:

In order to understand the Funds Flow Statement the meaning of ‘fund’ must be known although the ‘fund’ has got different meaning and interpretation Different accountants/ authors have used the term in different sense, e.g. Cash Fund, Capital Fund, Working Capital Fund etc.

In other words, they have been interpreted in various ways, viz.:

(a) Cash Fund:

ADVERTISEMENTS:

Some use the expression ‘the amount of Cash’ in a conservative or narrow sense, as it is synonymous with Cash (i.e., un-deposited cash plus demand deposits at bank). Fund statement is a statement where various types of cash transactions are to be evaluated in the form of ‘Cash Flow Statement’ Some others are of opinion that marketable securities should also be added with cash.

(b) Net Monetary Asset Fund:

There are some other accountants who are of opinion that with the amount of cash. Bank and marketable securities, short-term receivables and secondary cash reserves should also be included with such cash fund.

(c) Capital Fund:

ADVERTISEMENTS:

Others use the term ‘Fund’ in a broader sense to mean the total amount of resources employed in the business. It is considered as purchasing or spending power or as all financial resources, arising, as several writers have pointed out, from external rather than internal transactions of the firm. In short, this fund includes the financial resources which affects other than working capital.

(d) Working Capital Fund:

Still others are of the view that the amount of Net Working Capital or the excess of current assets over current liabilities, should be considered as ‘Fund’, particularly for the purpose of preparing Funds Flow Statement. The primary argument against this view is that Stock, Debtors, Short-term investments are considered as equivalent to cash.

And that is why at the time of preparing Funds Flow Statement consolidated changes of different items constituting the Fund are taken into consideration instead of incorporating the changes of each individual item. There is no effect of those transactions which are limited to working capital only in this statement.

ADVERTISEMENTS:

Now, we are to see which transactions affect working capital and which do not. Transactions which affect Working Capital

The following items that will cause a change in Working Capital:

A. Increase in Working Capital:

i. Issue of Shares and Debentures;

ADVERTISEMENTS:

ii. Sale of Fixed Assets or Non-Current Assets;

iii. Income from different sources.

B. Decrease in Working Capital:

(i) Redemption of Preference Shares or Debentures;

ADVERTISEMENTS:

(ii) Purchase of Fixed Assets or Non-Current Assets;

(iii) Payment of Miscellaneous Expenses;

(iv) Payment of Dividend etc.

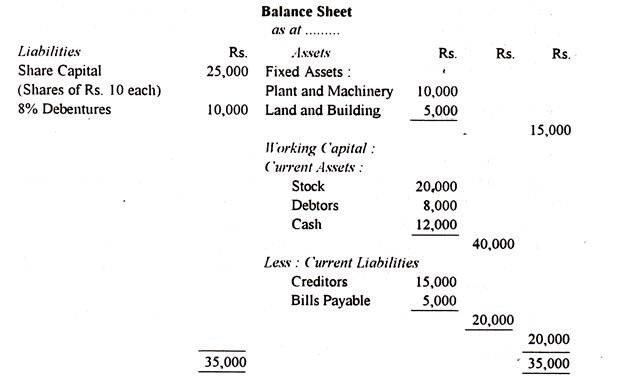

The above increase or decrease in working capital can be represented with the help of the following example:

In the above example, Working Capital becomes Rs. 20,000. Now, suppose. Land and Building is sold for Rs. 8,000 and if the money thus realised is not invested in fixed or non- current assets, the amount of working capital will be increased to the extent of that amount since it will increase the stock of cash — a component of current assets.

ADVERTISEMENTS:

Therefore, the total current assets will increase to Rs. 48,000 without, however, causing any change in the total amount of current liabilities. In other words, working capital becomes Rs. 28,000. In short, if there is a shift from fixed or non-current assets to current assets, there will be an inflow or increase of funds for working capital.

Similarly, as the above illustration shows, if the entire amount of stock is sold for Rs. 20,000 in cash, i.e., at par, and the money is invested for acquiring a non-current asset, say. Land and Building, working capital will be reduced by Rs. 20,000 and in that case working capital will be nil (Rs. 20,000 – Rs. 20,000).

That is, in short, a shift from current assets to fixed assets or non-current assets, will involve an application or decrease of funds for working capital.

Again, as it is clear from the above example, if Debentures are redeemed at par, working capital will be reduced by the amount of Rs. 10,000. This means there will be an application of funds for working capital since there will be a decrease of stock of cash.

So, if a fixed or long-term liability is paid off out of the stock of current assets, i.e., cash, there will be an application of funds for working capital or, the consequent decrease in working capital.

On the identical plane, if fresh equity shares are issued for Rs. 10,000 and the proceeds are not utilised either in non-current assets or fixed assets, there will obviously, be an increase in working capital since the total amount of current assets will be increased in the form of cash without, however, any change being caused in total current liabilities.

Working capital in that case will be Rs. 30,000. That is, if the stock of current assets is increased by the proceeds from any fixed or non-current liability, there will be an inflow or increase of funds for working capital.

Transactions which do not affect working capital:

The following items do not bring about any change in Working Capital:

(i) A shift from one current asset to another current asset by an equal amount or from one current liability to another current liability by an equal amount,

(ii) An increase in current assets by a corresponding equal increase in current liabilities;

(iii) A decrease in current assets by a corresponding equal decrease in current liabilities;

(iv) An increase in non-current assets by a corresponding equal increase in non-current liability or fixed liability;

(v) A decrease in non-current liability by a corresponding equal increase in non- current liability.

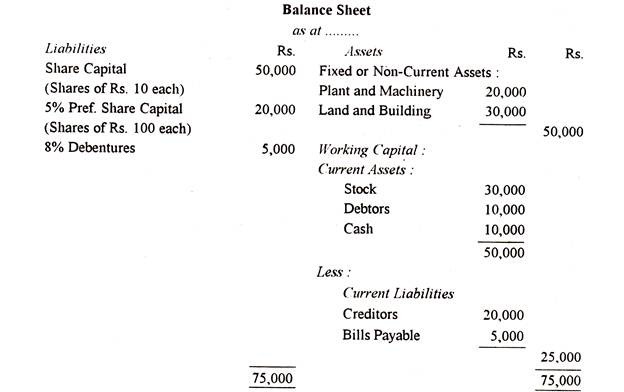

The following example reveals the above facts:

In the above example, working capital is found to be Rs. 25,000.

The above items may be considered one by one with reference to their respective examples as follows:

(i) Cash received from Debtors amounted to Rs. 5,000;

(ii) Purchased goods on credit for Rs. 10,000;

(iii) Creditors are paid for Rs. 6,000;

(iv) Equity shares are to be issued for Rs. 20,000 for acquiring Plant and Machinery,

(v) 8% Debentures are to be converted into 5% Preference shares to the extent of Rs. 4,000.

Thus, the position of the Balance Sheet vis-a-vis Working Capital will be:

The above list does not include the items of current assets and current liabilities. Therefore, current assets exceed current liabilities or in other words, if net current assets increase, there will be increase of funds (i.e., increase in working capital). Similarly, if current liabilities exceed current assets or if net current assets decrease, there will be decrease of funds (i.e., decrease in working capital).

In short, increase in working capital is considered as an increase in net current assets or an application of funds whereas decrease in working capital is considered as an increase in current liability or a source of funds. The increase or decrease is to be reconciled with the changes in working capital statement.

Depreciation as a Source:

Depreciation becomes an expense as expired cost Like other business expenses depreciation is charged against gross revenue of the period in which cost for fixed assets degenerates into expenses as expired cost Nevertheless, an altogether different situation is believed to arise from charging depreciation to gross revenue as expense as against the effect of charging other business expenses to the asset.

This difference may be ascribed to the fact that whereas other business expenses are cash consuming, depreciation, as business expense, is a non-cash variety. There is no outflow of cash or other liquid assets in respect of imputed expenses of depreciation.

As a result, whereas charging of other business expenses to gross revenue goes to compensate the loss of cash that are spent in total by way of incurring these expenses but apparently it is not so in case of non-cash consuming expense as involved in charging depreciation to gross revenue.

Here, the supposed loss of a portion of fixed assets, although not caused by any physical transfer of the same, is attained to be compensated or replaced by holding back an equivalent quantity of liquid resources out of gross revenue.

As a result, there is an increase of fund although the so called cost of fixed assets actually stands exactly what it did in the past This difference in consequence, as a result of charging depreciation to gross revenue on one hand and other business expenses in believed to be the process by which depreciation may serve as a source of working capital.

Concept of Flow:

When economic values are transferred from one asset to another or from one equity to another or from an asset to an equity or from equity to asset or a combination of any of them, the same is referred to the ‘Flow’ of funds.

When ‘Working Capital Fund’ is considered, this ‘flow’ of funds indicates this movement of funds which are expressed as ‘/low in’ or ‘/low out’. It happens particularly when changes are made from non-current assets account (i.e., fixed asset etc.) to current assets account or vice-versa e.g., when a plant is purchased against cash or preference shares are redeemed etc.

However, the flow of funds is a continuous process i.e., as soon as the funds are used, there must be an off-setting source. It may also be stated that the liabilities and net worth represent net source whereas the assets of a firm represent net use of funds.

3. Funds Flow Statement:

It is a statement which discloses the analytical information about the different sources of a fund and the application of the same in an accounting cycle It deals with the transactions which change either the amount of current assets and current liabilities (in the form of decrease or increase in working capital) or fixed assets, long-term loans including ownership fund.

It gives a clear picture about the movement of funds between the opening and closing dates of the Balance Sheet It is also called the Statement of Sources and Applications of Funds: Movement of Funds Statement: where got where gone statement; Inflow and Outflow of Fund Statement etc.

No doubt. Funds Flow Statement is an important indicator of financial analysis and control. It is a valuable aid to the financial manager and also to a creditor for assessing the uses of funds and also helps to determine how the funds are financed. The financial analyst can evaluate the future flows of a firm on the basis of past data.

This statement supplies an efficient method for the financial manager in order to assess the:

(a) Growth of the firm,

(b) Its resulting financial needs and

(c) To determine the best way to finance those needs.

In particular, funds flow statements are very useful in planning intermediate and long-term financing.

4. Object of Preparing a Fund Flow Statement:

The main purpose of preparing a Fund Flow Statement is that it reveals clearly the important items relating to sources and applications of funds of fixed assets, long-term loans including capital. It also informs how far the assets derived from normal activities of business are being utilised properly with adequate consideration.

Secondly, it also reveals how much out of the total funds is being collected by disposing of fixed assets, how much from issuing shares or debentures, how much from long-term or short-term loans and how much from normal operational activities of the business

Thirdly, it also provides the information about the specific utilisation of such funds, i.e., how much has been applied for acquiring fixed assets, how much for repayment of long-term or short-term loans as well as for payment of tax and dividend etc.

Lastly, it helps the management to prepare budgets and formulate the policies that will be adopted for future operational activities.

5. Parties Interested in Funds Flow Statement:

The following parties are interested:

(a) Share-Holders:

They are interested in knowing how much is available for the payment of dividend and the position of their investment in the company.

(b) Short-Term Creditors (including bankers):

They are interested in having an idea of the risk which may be involved in granting credit to the company.

(c) Management:

Management is interested in knowing the trend of different forms of financing and their utilisation so that they can prepare budgets and estimates. They are also interested in knowing whether the working capital has been properly utilised.

(d) Investors:

They are interested in knowing whether any investment can be made in the company and if so, what should be the expected rate of return.

6. How to Prepare a Fund Flow Statement:

The Following steps are to be followed carefully while preparing a ‘Fund Flow Statement’:

First Step:

Ascertain the amount of Working Capital for the two consecutive years from the respective Balance Sheets and determine the schedule of changes in Working Capital which will result in either a decrease or an increase in Working Capital.

The proforma of the ‘Schedule Of changes in Working Capital’ is given below:

Second Step:

Open all other non-current assets and non-current liabilities accounts by taking their respective opening and closing balances

Third Step:

Consider the adjustment given in the problem (by Double Entry Principle) one by one.

Fourth Step:

Close the accounts one by one which may result either in an item of Sources of Funds or an item of Applications of Funds or close the remaining accounts by transferring to Adjusted Profit and Loss Account.

The proforma of Funds Flow Statement is given below:

7. Funds Flow Statement and Income Statement:

The difference between the Funds Flow Statement and the Income Statement (i.e., Profit and Loss Account) are enumerated below:

(a) An Income Statement reveals the results of the operation for a particular period in the form of profit or loss i.e., how much has been earned by a firm and how the same has been incurred. Funds Flow Statement, on the other hand, expresses the requirement of financial resources in order to operate the business activities i.e., what are the possible sources from which funds can be raised and the application for the same.

(b) While preparing an Income Statement, only revenue items i.e., revenue receipts and revenue expenditures are taken into consideration for the purpose of ascertaining the results of the operation whereas for preparing Funds Flow Statement both transactions, whether capital or revenue, are taken into consideration.

(c) In a Funds Flow Statement, both the sides viz, sources of Funds and application of Funds must be equal. But in an Income Statement there is always a difference which is known as profit (if credit side exceeds debit side) or loss (if debit side exceeds credit side).

(d) Funds Flow Statement can predict the financial health of an enterprise very well in an efficient manner since it incorporates all the items, whereas an income statement even fails to predict the true financial position since non-fund items (viz depreciation, write off item etc.) are included here.

Thus, we are to consider them from different angles since both of them present different functions. They are rather complementary to each other and not a substitute for the other.

8. Funds Flow Statement and Indian Position Thereto:

Although it is not compulsory for an Indian enterprise to prepare a Fund Flow Statement in its published annual report, many firms from public and private sectors have been introducing funds flow statement in their published financial statement at present

However, the Council of the Institute of Chartered Accountants of India has issued Accounting Standard No. 3, Changes in Financial Position (AS – 3) in June, 1981. The standard deals with the financial statement which summarizes for a given period the sources and applications of funds of an enterprise.

In the initial years, this accounting standard was recommendatory in character. During that period, this Standard was recommended for use by companies listed on a recognised stock exchange and other large commercial, industrial and business enterprise in the public and private sectors.

9. Some Practical Hints for Funds Flow Statement:

The following matters (adjustments) require special attention while preparing a Funds Flow Statement:

(I) Provision for Taxation:

Provision for taxation may be treated in the following two ways:

(a) Treated as an appropriation profit:

Under this treatment, the amount of tax, which should be provided out of profit, is to be debited to Profit and Loss Account, whereas the actual amount of tax which is to be paid is to be shown as an application in the ‘Statement of Sources and Applications of Funds’

(b) Treated as a charge against profit:

Under this treatment, provision for taxation is to be treated simply as a current liability, and. therefore, no adjustment is necessary either in Profit and Loss Account or m the ‘Statement of Sources and Applications of Funds’ as an application.

To sum up, the same should be treated in the following manner:

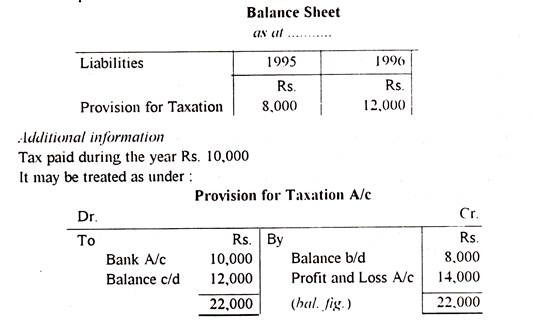

(1) When the amount of Provision for Taxation is given only in the liabilities side of the Balance Sheet For example:

It may be treated in the two following ways:

(a) Either:

It can be treated as Current liabilities and as such, they will be deducted from the total current assets while computing ‘Changes in Working Capital’

(b) Or:

The amount for the year 1995 (i.e. 1st year) is to be shown as an ‘Application of Funds’ and the amount for the year 1996 (i.e., 2nd year) is to recorded in the debit side of the Profit and Loss Account.

(c) When the amount of Provision for Taxation is given both in the liabilities side of the Balance Sheet and also in the adjustment by way of additional information.

For example:

i.e., Rs 10,000 will be shown as an Application of Fund’ and Rs. 14,000 will be recorded in the debit side of Profit and Loss Account

If provision of tax is given in the problem, in that case, the amount to be paid, will the balancing figure.

Same principle is to be applied for ‘Proposed Dividend’.

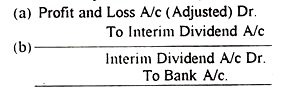

(2) Interim Dividend:

In case of Interim Dividend, however, the same should always be adjusted against Profit and Loss A/c (Adjusted).

The entry being:

In other words, Interim Dividend should appear in the debit side of P & L (Adjusted) A/ c and the same will be shown as Application of Funds’ since it is an item of appropriation of profit

(3) Write offs:

The following items should be written off against Profit and Loss Account (Adjusted):

Goodwill, Preliminary Expenses, Discount on Issues of Shares and Debentures, Advertisement Expenses A/c etc.

(4) Provision for Depreciation:

It may be treated in the following two ways:

(i) Either it may be considered as a source of fund.

(ii) or, it may be adjusted against Profit and Loss (Adjusted) A/c in order to find out the adjusted trading profit, (the latter method is followed in this volume).

Consider the following cases one by one:

It is quite interesting to note that if the Provision for Depreciation account is not given in the liabilities side of the Balance Sheet or the same, if not, is deducted from the fixed asset from the assets side of the Balance Sheet, i.e., if it is given in the adjustment, the treatment will, however, be changed. Because, fixed asset are given at written down value.

Consider the following case:

Case II:

In this case, Provision for Depreciation on Land and Building account and the Land and Building Account will be represented as under:

Since, the W. D. V of Land and Building Account is given, in order to find out the book value accumulated depreciation of the opening and closing balances are to be added with the respective opening and closing balances of the Land and Building Account. And the actual amount of depreciation for the year is adjusted against Provision for Depreciation on Land and Building Account.

(5) Purchase and Sale of fixed assets and profit or loss on sale thereon:

When any fixed asset (i.e.. Plant and Machinery, Land and Building, Furniture and Fittings etc.) is acquired or purchased, the same is treated as an ‘Application of Funds’. Similarly, when the same is sold, it is an item of ‘Source of Fund’. But, usually the asset is sold either at a profit or at a loss (i.e., profit, when selling price is more than the W D. V. of the asset and loss in the opposite case.)

The profit or loss on sale so made, is to be adjusted against Profit and Loss (Adjusted) Account for ascertaining Trading profit The amount of depreciation for this purpose should also be taken into consideration

When there is no provision for depreciation, the amount of depreciation will be adjusted in the usual manner, i.e.. Profit and Loss Account will be debited and the corresponding Asset Account should be credited. Consider the following cases.

Additional Information:

(i) A plant and machinery costing Rs. 20,000 (W.D.V. Rs. 12,000) was sold for Rs 5,000)

Additional Information:

(1) A plant costing Rs. 20,000 (W. D. V. Rs. 12,000) was sold for Rs. 10,000. In this case, the Plant and Machinery Account, Provision for Depreciation on Plant and Machinery Account and also the Plant and Machinery Disposal A/c /Plant and Machinery Sale Account will be shown as under:

Thus, sale of Plant and Machinery is to be shown as a ‘Source of Fund’ and loss on sale of Plant and Machinery will be adjusted against Profit and Loss (Adjusted) Account, and the depreciation on the plant sold is to be adjusted against Provision for Depreciation on Plant and Machinery Account.

(6) Provision against Current Asset:

Sometimes provisions are to be made against the anticipated losses on current assets, e.g.. Provision for Bad and Doubtful debts. Provision for loss on stock or allowance for inventory loss etc.

They can be treated in the following three ways:

(i) Either, the amount of such provision (say. provision for bad debt) may directly be deducted from the asset concerned, (here, from Sundry Debtors) while calculating the schedule of changes in working capital i.e., net amount is to be shown in the statement.

(ii) Or, The current assets should be shown at its gross amount and the amount of such provision may be added with the current liabilities and thereafter the same will be deducted from the total current assets while computing the schedule of changes in working capital.

Whatever method we follow, the amount of increase or decrease in working capital will be the same.

(iii) Provision may also be treated as an internal reserve or surplus. Thus, the amount of such provision will not appear in the schedule of changes in working capital, while finding out the increase or decrease in working capital.

The current asset may be shown at its gross value. A separate Provision for Bad Debt Account will be opened and the balancing figure will either be transferred to the debit side of Profit and Loss (Adjusted) Account or added back to Net Profit for the current year after debiting the provision in order to determine the funds from operation.

(7) Trading Profit (i.e., Funds from operation):

It is the most regular and significant source of fund. It is the largest source of fund in the long run. The payment of dividends, repayment of loan, purchase of fixed asset etc. must depend upon this source. We know that sales are the result of inflow of funds in the form of cash or accounts receivables but cost of goods sold along with the other operating expenses cause outflow of funds at the same time by reducing cash and bank balance.

So, the net effect of operation will be a source of fund (or inflow of funds) when sales revenue exceeds the cost of goods sold and operating expenses (outflow of funds) during the period and vice versa in the opposite case.

Trading profit can be ascertained under the following two methods:

(a) Add. Back Method; and

(b) Direct Method.

(a) Add-Back Method:

Most of the annual reports follow this method and compute the ‘finds from operation’ simply by adjusting the figures relating to earnings for the items which do not affect the funds although they are included in Profit and Loss Account.

The same is outlined below:

(b) Direct Method:

(b) Direct Method:

This is nothing but takes the form of final accounts of a company. It takes into consideration the each items of revenue incomes and revenue expenditure individually which affect funds from operation i.e., the items which affect funds. So, items like depreciation, provision for bad debts, write offs etc. wilt not at all appear here. The outline of such a Profit and Loss Account can be depicted as under:

But while preparing ‘Funds Flow Statement’ the most significant aspect is the preparation of Profit and Loss Account (Adjusted) which will help us to ascertain the Trading Profit which is considered as a source of fund.

The outline of such an account is presented as under: *")