Here is a compilation of top four accounting problems on redemption of preference shares with its relevant solutions.

Problem 1 (Redemption out of profit at premium):

The following are the balance appearing in the books of Puri Cycles Ltd. as on 31st Dec.

Share Capital

ADVERTISEMENTS:

Equity share capital 18, 00,000

Preference shares (fully paid) 9, 00,000

Security premium 1, 00,000

General reserve 6, 00,000

ADVERTISEMENTS:

Profit & loss account (Cr. balance) 4, 00,000

The company decided to redeem the preference share @ a premium of 10% out of profit and general reserve. Give journal entries relating to redemption of preference shares.

ADVERTISEMENTS:

Problem 2 (Redemption partly out of fresh issue):

Following is the balance sheet of Banbaxy Ltd. as on March 31, 2006.

The preference shares were to be redeemed at a premium of 10%.

For the purpose of Redemption following has been decided by the company:

(i) To sell investments for Rs. 1, 90,000

(ii) A minimum balance in the bank shall be required for Rs. 20,000 for meeting working requirements.

ADVERTISEMENTS:

(iii) To issue sufficient equity shares at a premium of Rs. 2.50 per share to raise balance of fund. Show Journal Entries and the balance sheet after redemption.

Problem 3 (Redemption partly out of profit and partly out of fresh issue):

ADVERTISEMENTS:

The following is the balance sheet of Punjab Wools Ltd. as on March 31, 2005

Company decided to redeem both the classes of preference shares on 31st March 2006 at 5% premium. The company issued for cash so many equity shares of Rs. 10 each as were necessary to provide for redemption of both classes of preference shares which could not otherwise be redeemed. The issue was fully subscribed.

Pass journal entries and prepare balance sheet after redemption.

ADVERTISEMENTS:

Solution:

Problem 4 (Where minimum number of equity shares is to be issued for redemption):

ADVERTISEMENTS:

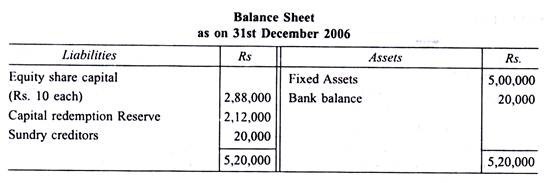

The summarised Balance Sheet of a Company is given below:

The Redeemable Preference shares are to be redeemed at a premium of 10%. The Directors wish that only the minimum number of fresh equity shares of Rs 10 each at a premium of 5% be issued to provide for redemption of such preference shares as could not otherwise be redeemed.

You are required to give the journal entries and also prepare the Balance Sheet after redemption.

Solution: