In this article we will discuss about the accounting provisions regarding revaluation of assets and liabilities in the consolidated balance sheet, explained with the help of a suitable illustration.

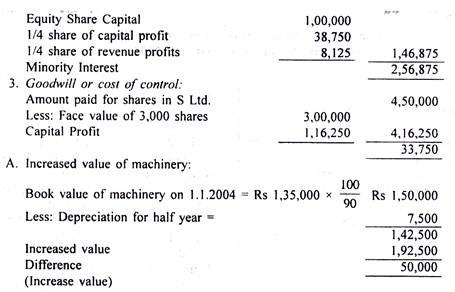

At the time of acquiring shares in a subsidiary company, it is usual for the holding company to revalue the assets and liabilities of the former in order to arrive at a fair price to be paid for its share. Any profit or loss on such revaluation is a capital profit or loss. Sometimes revaluation of assets and liabilities is not given effect immediately. In such cases the past profits of the subsidiary company may have to be corrected on account of change in the amount of depreciation.

Holding company’s share of such capital profit is transferred to capital reserve or deducted from cost of control or goodwill and vice versa if there is loss on revaluation. Share of profit of minority shareholders is added to the minority interest and deduction is made from the minority interest if there is a loss on revaluation.

ADVERTISEMENTS:

Illustration:

H Ltd. acquired 3,000 Equity Shares in S Ltd. on 1st July 2004. As on the date of acquisition, H Ltd. found that the value of land and buildings and machinery of S Ltd. should be Rs 1, 50,000 and Rs 1, 92,500 respectively.

ADVERTISEMENTS:

Prepare the consolidated Balance Sheet of H Ltd. and its subsidiary S Ltd. as on 31st Dec. 2004 taking into consideration the fact that assets are to be taken at their proper values.