Financial statements are basic and formal means through which corporate management make public communication of financial information along with select quantitative details. These are structured financial representation of financial position and performance of an enterprise.

A company is managed by its Board of Directors who is responsible for reporting to the various interest groups of the company about its financial performance and state of affairs. The purpose of financial reporting is to help the various interest groups in their decision making relating to investment in the company and/or dealing with the companies in various manner.

A complete set of financial statements in India are:

I. Profit and Loss Account including Earning Per Share data;

ADVERTISEMENTS:

II. Balance Sheet

III. Cash Flow Statement which is applicable for companies listed in a recognized Stock Exchanges in India, and

IV. Consolidated Financial Statements applicable for a companies listed in a recognized Stock Exchanges in India and having subsidiaries.

Profit and Loss Account presents financial performance of a company. Balance Sheet reflects its state of affairs. Cash Flow Statement explains the cash earnings and expenditure of a company. A holding company which is listed in a stock exchange is required to prepare and present a set of consolidated profit and loss account, balance sheet and cash flow statement of the company and all its subsidiaries that helps to understand performance, state of affairs and cash earnings and expenditure of the corporate group as a whole.

ADVERTISEMENTS:

See the Table below for various components of financial statements to be prepared by Indian companies.

Legal Requirements:

Section 210 of the Companies Act, 1956 requires the Board of Directors of every company to lay at every annual general meeting held under section 166:

ADVERTISEMENTS:

(i) A balance sheet as at the end of the accounting period, and

(ii) A profit and loss account for that period. The accounting period is legally termed as “financial year”. The financial year may be less or more than the calendar year, but its maximum duration is fifteen months. On obtaining a special permission from the Registrar of Companies, it is possible to extend the duration of a financial year up to eighteen months.

In case of first annual general meeting, the financial year should not end more than nine months preceding the date of meeting. For any subsequent annual general meeting, financial year should begin with the immediately next day of the earlier financial year and should not end more than six months preceding the date of meeting. In other words, the first annual general meeting should be held within nine months from the end of the financial year chosen for the preparation of the financial statements. Any subsequent annual general meeting should be held within six months from the end of the financial year.

True and Fair View:

ADVERTISEMENTS:

Sub-sections (1) and (2) of section 211 of the Companies Act, 1956 state the fundamental characteristics of financial statements. As per this section every Balance Sheet should give a true and fair view of the statement of affairs of the company at the end of the financial year, and every Profit and Loss Account should give a true and fair view of the profit or loss of the company for the financial year.

Although the Companies Act requires the financial statements to disclose “true and fair” view, it does not explain what exactly mean by the term. In the accounting parlance the term “true and fair” is now well understood.

The term “true and fair” means that accounts have been prepared:

i. In accordance with the requirements of the Companies Act and other applicable legislations; and

ADVERTISEMENTS:

ii. In accordance with generally accepted accounting principles and policies.

In India, generally accepted accounting principles and policies are available in the accounting standards and various other documents issued by the Institute of Chartered Accountants of India (ICAI) and accounting policies specified other statutes like the Companies Act, 1956.

Schedule VI to the Companies Act includes certain disclosure requirements for the preparation and presentation of financial statements. These instructions do not exhaustively cover the accounting principles and policies to be adopted on various accounting issues and the disclosure requirements for corporate financial reporting in transparent manner. Accordingly, it becomes necessary to follow accounting standards or other pronouncements of the ICAI.

However, accounting standards and other pronouncements of the ICAI are significantly different on many counts with the international accounting standards and accordingly, even if the accounts are prepared following Indian accounting standards and other GAAPs (Generally Accepted Accounting Principles), it is unlikely to be considered as true and fair in many developed countries including the USA, and the UK.

ADVERTISEMENTS:

In Indian national context, the financial statements shall reflect true and fair view if the following conditions are fulfilled:

i. Balance Sheet is drawn up as per the requirements of Schedule VI and in the form given in Part I of the said Schedule;

ii. Profit and Loss Account is drawn up as per the requirements of the Part n of Schedule VI;

iii. Proper books of account are maintained as required in section 209(1); i.e. proper books of account are maintained with respect to

ADVERTISEMENTS:

a. All sums of money received in respect of receipts and all sums of money paid in respect of expenditure,

b. All sales and purchases of goods by the company,

c. Assets and liabilities of the company, and

d. Cost records relating to utilisation of material or labour or to other items of costs in case of companies engaged in the production, processing, manufacturing or mining activities, if required by the Central Government;

Proper books of account are to be maintained following double entry system of book keeping and accrual basis of accounting;

a. Balance Sheet and profit and loss account are prepared following generally accepted accounting principles and policies; i.e.

ADVERTISEMENTS:

(i) Accounting policies adopted by the company are consistent with generally accepted accounting principles and policies,

(ii) Financial statements reflect substance of the transactions and events that took place during the financial year, and

(iii) Disclosures are consistent with the accounting standards and other relevant pronouncements of the ICAI.

Section 211(3 A) of the Companies Act, 1956 as amended by the Companies Amendment Act, 1999 requires that every profit and loss account and balance sheet shall comply with the accounting standards.

Users of the Financial Statements:

1. Present and Potential Investors:

They need information primarily to aid their decisions of buying, selling or holding shares of the reporting entity. Of course, the shareholders, who hold relatively larger block of shares sufficient to influence composition of the board of directors, also need information to assess effective stewardship by the existing management. In other words, a large shareholder needs information to take decision whether to continue with the existing management.

2. Employees:

Employees and their representative bodies are interested in the financial statements to ascertain ability of the reporting entity to maintain the existing staff and service them through appropriate remuneration, promotion and retirement benefits. Sometimes the employees may have the dual roles as shareholders as well as employees.

3. Lenders:

Lenders may have interest in the reporting entity either in the short run or in the long run depending on the nature of their credits. In general, lenders look into debt servicing capability of the enterprise both in terms of timely repayment of principal and interest. Long term lenders are more concerned with solvency of the reporting entity, whereas short term lenders are primarily interested in liquidity, current profitability and operational cash flow.

4. Suppliers and Other Creditors:

Suppliers and other creditors are generally interested in the reporting entity in the short run, and their interest is normally restricted to the ability of the reporting entity to maintain payment cycle which is determined by liquidity and operating cash flow position. In case the suppliers and other creditors have developed long term supply relationship with the reporting entity, then they become concerned about solvency also.

5. Customers:

Likewise suppliers and other creditors, customers may also have either short term or long term interest in their reporting entity. In case of short term interest, a customer may simply be satisfied with the information relating to liquidity, current profitability and operational cash flow. If a customer has long term interest in the reporting entity, he would rather prefer to analyse solvency and its ability to continue as a going concern.

6. Government and its Agencies:

They have multiple purposes to look into the corporate financial statements:

1. To observe compliance with laws and regulations;

2. To collect revenue by way of taxes;

3. To grant subsidy;

4. To review employment opportunities, resource allocation, fiscal policies and other macro-level decisions.

7. Public:

The public at large are interested in continuance of the reporting entity for its contribution in the local economy through protection of the present level of employment, creation of new employment opportunities, promoting ancillaries, facilitating various development programmes, etc. Researchers, financial analysts and market survey agencies are also interested in the corporate financial statements with a special and limited purpose concerning their area of research, analysis or survey.

Accordingly, financial statements are only formal documents through which the company management communicate financial position, performance and change in cash flow to the large defined but unidentified user-groups. An important responsibility of the corporate management is to make financial statements transparent so as to sub serve information needs of the various user-groups to the maximum. A piece of information that cannot be covered in the financial statements but is considered relevant for the users decision making should be covered in the directors report.

Action taken by one of the users group may affect the interest of the other group.

For example,

(i) If the company increases corporate tax rate, shareholders’ wealth will decrease.

(ii) If the managerial remuneration is increased not necessarily it will increase shareholders’ value.

(iii) A merger of one company with another company in which the promoter group is having majority stake may not improve the shareholders’ value of the acquirer.

Balance Sheet, profit and loss account and cash flow statement provide minimum statutorily required financial information. The purpose of financial statement analysis is to evaluate such information in the light of non-accounting and market related data and interpret the information contained therein for improving the decision making by various users group.

Generally, companies release summary financial information about their quarterly and annual performance and state of affairs. Full state of financial statements are made available at the time of annual general meeting of the company. Most often this time lag reduces the decision value of the financial statements information from the point of view of the prospective shareholders.

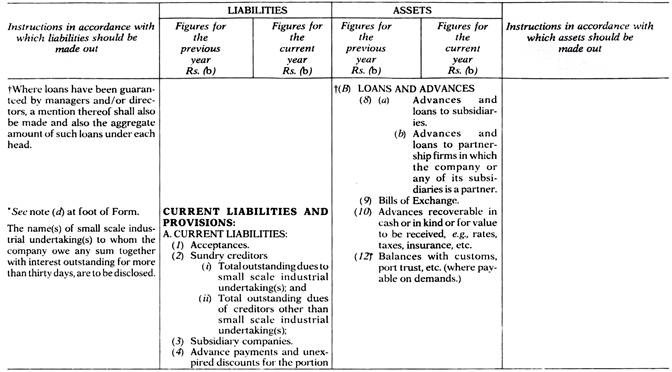

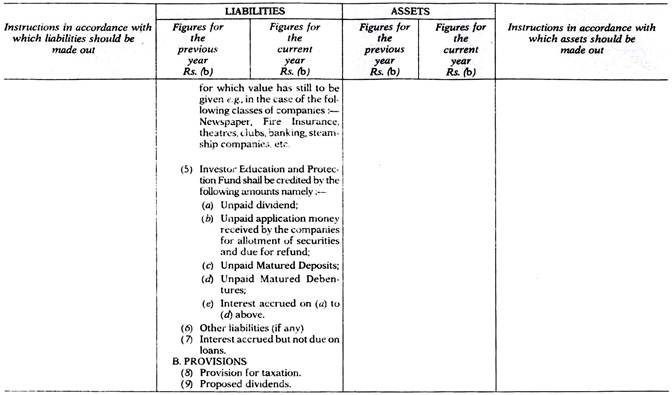

Schedule VI to the Companies Act:

Balance Sheet should be prepared in the form given in Part I of the Schedule VI or as near thereto and the instruction attached in the Notes to Part I should be followed while preparing a balance sheet. In the Part II of the Schedule VI certain disclosure requirements have been specified. No form of profit and loss account has been prescribed in the Companies Act. Accordingly, a company can design its profit and loss account suitably provided it satisfies the disclosure requirements specified in Part II of the Schedule VI.

Central Government may exempt any class of companies from compliance with any requirements of Schedule VI in the public interest. Also the Central Government may modify the requirements of Schedule VI on an application made by the Board of Directors or with the consent of the Board of Directors.

It is necessary to prepare profit and loss account and balance sheet even if the company is under construction and no commercial activity have been undertaken. However, the Department of Company Affairs has clarified that it has no objection if a company prepare an account under the name Development Account or Expenditure during Construction Account or under any other suitable name; but it has to comply with the requirements of Schedule VI.

Directors Responsibility Statements:

Corporate management is responsible for the preparation of financial statements. Section 210 of the Companies Act, 1956 requires the board of directors to lay before the annual general meeting the balance sheet and the profit and loss account. Often a wrong notion is carried that it is responsibility of the auditors to finalise the accounts. The International Standards on Auditing (ISA) “Objective and Basic Principles Governing Audit” issued by the International Auditing Practices Committee (IAPC) categorically states that –

“While the auditor is responsible for forming his opinion on the financial statements, the responsibilities for the preparation of financial statements is that of management of the entity Management ‘s responsibilities include the maintenance of accounting records and internal controls, the selection and application of accounting policies and safeguarding the assets of entity. The audit of financial statements does not relieve management of its responsibilities.”

Section 217(2AA) of the Companies Act, 1956 requires that the report of the board of directors should include Directors’ Responsibility Statement.

This Statement should Specify:

i. That accounting standards had been followed in the preparation of annual accounts and or explanation for material departures from accounting standards;

ii. Accounting policies are selected and applied consistently, and judgments and estimates are made that are reasonable and prudent so as to give a true and fair view of state affairs at the end of the financial year and profit or loss of the company during the year.

iii. Directors have taken proper and sufficient care for:

(i) Maintenance of accounting records as per law,

(ii) Safeguarding assets of the company, and

(iii) Preventing and detecting fraud and other irregularities.

iv. Directors have prepared the accounts on a going concern basis.

Focus of the Newly Inserted Sub-Section (2 AA) of Section 217 is to Impose Responsibility of:

i. maintenance of adequate internal control and protective measures to safeguard assets of the company;

ii. pursuance of going concern assumptions in the preparation of financial statements;

iii. selection of accounting policies with prudence and its consistent application with an objective of reflecting true and fair view of the financial statements; and

iv. pursuance of accounting standards with an explanation if there is any departure.

Management may not prepare financial statements on going concern basis in case there exists significant doubt about the going concern status of the enterprise. This point has not been taken care of in section 217(2AA).

In India, preparation and presentation of corporate financial statements are governed by accounting policies stated in the Companies Act and any other statutes that govern the reporting entity, accounting standards and other documents stating accounting policies, measurement and disclosure issued by the Institute of Chartered Accountants of India (the apex accountancy body of the Government of India) or other regulatory authorities like the Securities and Exchange Board of India, the Reserve Bank of India, the Insurance Regulatory and Development Authority of India, etc. They together form Indian GAAP. In fact while preparing financial statements it is necessary to follow Indian GAAP.

Director’s Report:

Section 217 of the Companies Act, 1956 requires that a report by the board directors should be attached to the balance sheet, which is laid before a company in general meeting.

Contents of the Directors’ report include:

a) State of affairs of the company;

b) Transfer to reserve;

c) Recommendation of dividend;

d) Material changes affecting financial position of the company between the balance date and date of the directors’ report;

e) Conservation of energy, technology absorption, foreign exchange earnings and outgoings in the prescribed format;

f) Disclosure of the nature of business carried on by the company and its subsidiaries to the extent it is not harmful to the company and its subsidiaries;

g) Statement of employees, who were employed throughout the financial year, enjoying remuneration of not less than rupees twelve lacs p.a. or and employees, who were employed during the part of the financial year, enjoying remuneration of not less than rupees one lac p.a.;

h) Statement of employee shareholders employed throughout the financial year or part thereof, who along with spouse and dependant children hold not less two person of the equity shares, enjoying remuneration more than managing director, whole time director or manager;

i) Directors’ Responsibility Statement;

j) Reasons for failure to complete buy back of securities within specified time as per section 77A;

k) Explanation to information falling under section 222;

l) Clarifications on every reservations, qualifications and adverse comments contained in the auditors’ report;

Although Directors’ Report is not part of financial statements, it provides extremely important information about the present position and future prospect of the business of the company.

Comparative Information:

In India, financial statements are required to provide current period’s information along with previous period’s comparative data.

Clause (n) of General Instructions for Preparation of Balance Sheet included in Part I of Schedule VI to the Companies Act requires that:

“Except in the case of the first balance sheet laid: before the company after the commencement of the Act, the corresponding amounts for the immediately preceding financial year for all items shown in the balance sheet shall also be given in the balance sheet. The requirement in this behalf shall, in the case of companies preparing quarterly or half-yearly accounts, etc. relate to the balance sheet for the corresponding date in the previous year.”

Also Clause (6) of Part EE of the Schedule VI to the Companies Act requires that:

“Except in the case of the first profit and loss account laid before the company after the commencement of the Act, the corresponding amounts for the immediately preceding financial year for all items shown in the profit and loss account shall abo be given in the profit and loss account.”

Comparative information should be included in the narrative and descriptive information when it is relevant for understanding of the current period’s financial statements. When the presentation or classification of items in the financial statements is amended, comparative statements should be reclassified unless it is impossible to do so. This facilitates comparison of financial statements items.