This article throws light upon the seven major factors influencing capital structure. The factors are: 1. EBIT – EPS Analysis 2. Cost of Capital 3. Cash Flow Analysis 4. Control 5. Timing and Flexibility 6. Nature and Size of the Firm 7. Industry Standard.

Factors Influencing Capital Structure:

- EBIT – EPS Analysis

- Cost of Capital

- Cash Flow Analysis

- Control

- Timing and Flexibility

- Nature and Size of the Firm

- Industry Standard

Factor # 1. EBIT – EPS Analysis:

It is needless to say that if we want to examine the effect of leverage, we are to analyse the relationship between the EBIT (Earnings before interest and Tax) and EPS (earnings per share). Practically, it requires the comparison of various alternative methods of financing under various alternative assumptions relating to Earning Before Interest and Taxes.

Financial leverage or trading on equity arises when fixed assets are financed from debt capital, (including preference shares). When the same gives a return which is greater than the cost of debt capital, the excess will increase the EPS (Earnings per share) and the same is also applicable in case of preference share capital.

ADVERTISEMENTS:

But the former has some edges over the later due to the following:

(a) Interest on debt capital is an allowable deduction as per Income -Tax rule while calculating profit,

(b) Usually the cost of preference share is more costly than the cost of debt.

However, while planning capital structure of a firm, the effect of leverage, EPS are to be given due consideration. In order to increase the shareholders’ fund, a firm can effectively use its high level of EBIT against the high degree of leverage. It is already stated above that this effect of leverage can be examined if we analyse the relationship between the EBIT and the EPS.

ADVERTISEMENTS:

The above principle can be illustrated with the help of the following illustration:

Illustration:

Let us suppose, firm- X has a capital structure consisting of equity capital only. It has 50,000 equity shares of Rs. 10 each. Now the firm wants to raise a fund for Rs. 1, 25,000 for its various investment purpose after considering the following three alternative methods of financing:

1. If it issues 12,500 equity shares of Rs. 10 each;

ADVERTISEMENTS:

2. If it borrows a debt of Rs. 1,25,000 at 8% interest; and

3. If it issues 1250 8% Preference Shares of Rs. 100 each.

Show the effect of EPS under various methods of financing if EBIT (after additional investment) are Rs. 1, 56,250 and rate of taxation is @ 50%.

Solution:

Thus, from the above table it becomes quite clear that the EPS is maximum when the firm uses debt-financing although the rate of preference dividend and the rate of debt financing is the same. This is so happened due to the most significant role played by Income-Tax as preference dividend is not a deductible item from taxation while the interest on debt is as deductible item.

It has already been stated above that EPS will increase with a high degree of leverage with the corresponding increase in EBIT. But if the firm fails to earn a rate of return on its assets higher than the rate of debt financing or preference share financing it will have to experience an opposite effect on EPS which can be shown with the help of the following illustration.

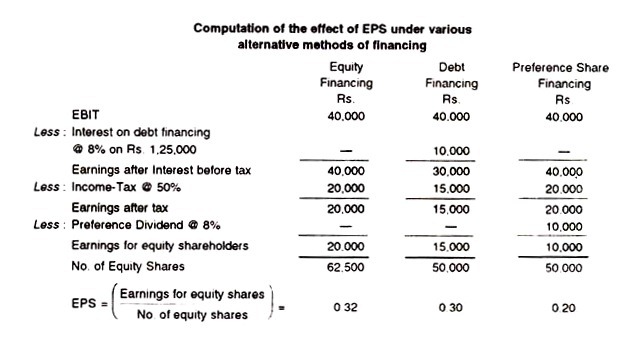

Let us suppose, the EBIT is Rs. 40,000 instead of Rs. 1, 56,250.

The EPS under various methods of financing is shown below:

Thus, it is found from the above table that if the rate of debt financing is more than the rate of earning before tax, the EPS will come down with the corresponding degree of leverage that directly affect the EPS.

Whether the debt financing should be taken into consideration by a firm or not, the financial manager must analyse the EBIT – EPS relationship which has a direct bearing on the capital structure position of a firm Before taking any decision the financial manager must see the subsequent changes in EBIT and must scrutinize the impact of EPS under various alternative financing plans in his hands.

Consequently, if he finds that the cost of debt is less or EBIT is more than that he can suggest to take a large amount of debt capital in order to increase the EPS in the total capital structure of a firm which has a favourable effect on the market value of each equity share.

In the opposite case, however, i.e., when EBIT is less or cost of debt capital is more than the rate of earnings, a firm must not go for debt financing. Thus, if there is a higher level of EBIT and less possibility of fluctuation, a firm can effectively use debt as a method of financing mix in its total capital structure position

Factor # 2. Cost of Capital:

ADVERTISEMENTS:

While explaining cost of capital we have mentioned that usually cost of equity (K ) is greater than the cost of debt (Kd) due to the most significant advantages of income-tax among others. Actually, financing decision should be based on overall cost of capital (i.e., after considering both equity and debt).

In other words, their combination will be in such a way so that, either it minimizes the overall cost of capital or maximises the market value of the firm.

If debt financing is increased there will be a corresponding reduction in the overall cost of capital till the rate of return exceeds the explicit cost of financing. But if debt financing is continuously increased, the same will increase the cost of equity and debt capital as well which invites more financial risk and consequently increases the weighted average cost of capital up to a certain level of debt-equity mix.

Thus, it can be stated that optimum capital structure may not always be attained by the financing decision which is based on financial leverage by allowing due importance to the cost of capital.

ADVERTISEMENTS:

It can further be stated that if debt-financing is continuously taken by a firm to minimise the overall cost of capital, the debt after attaining a certain limit, will become costly as well as risky sources of finance.

Thus, if the degree of leverage increases, the creditors desires a high rate of interest for increased risk and if the debt reaches at a particular point, they will not provide any loan further Moreover, the position of the shareholders becomes risky due to such excessive debt for which cost of equity is increased gradually.

So, combination of debt and equity will be in such a manner so that the market value per share increases and minimizes the average cost of capital of a firm. In real world situation, however, a range of debt-equity ratio exists where cost of capital is minimum although this range varies from firms to firms according to their nature, types and sizes.

We know that cost of equity capital includes cost of fresh issue of shares and cost of retained earnings as well. We also know that cost of debt is cheaper than cost of equity as also cost of retained earnings.

Again, in between retained earnings and cost of equity (new issues), the former is cheaper as the personal taxes are paid by the shareholders on their dividend income but retained earnings is a tax-free source and it also does not require any floatation cost. Thus, retained earnings are preferred between the two sources of equity funds.

Factor # 3. Cash Flow Analysis:

In order to meet the service fixed charge of a firm, analysis of cash flow is very important It indicates the ability of the firm to meet its various commitments including the service fixed charges which includes fixed operating charges and interest on debt capital.

ADVERTISEMENTS:

Thus, the analysis of the cash flow ability of the firm to service fixed charges is no doubt an important tool while analysing financial risk in addition to EBIT-EPS analysis in capital structure planning.

It has already been mentioned earlier that if the amount of debt capital increases, there is a corresponding increase in the amount of uncertainty which a firm must have to face to meet its obligation in the form of fixed charges.

Because, if a firm borrows more than its capacity and if it fails to meet its maturing, obligation at a future date, the creditors will acquire the assets of the firm for their unsatisfied claim which brings financial insolvency.

So, before taking any additional debt capital, analysis of expected future cash flows must carefully be considered as the fixed interest charges are paid out of cash and that is why analysis of cash flow presents a very significant information in this regard.

Needless to say here that if there is greater and stable expected future cash flow; a firm should go for a higher degree of debt which can be used as a source of finance. Similarly, if the expected future cash flows are unstable and smaller, a firm should avoid any fixed-charge securities which will be considered a very risky proposition.

Moreover, analysis of cash flow presents the following significant advantages which helps to prepare the debt-equity mix in the total capital structure of a firm:

(i) Cash flow analysis highlights on the solvency and liquidity position of a firm at the time of adverse condition;

(ii) It records the various change made in Balance Sheet and other cash flow which do not exhibit in Profit and Loss Account;

(iii) It takes the financial trouble in a dynamic context over a number of years.

In order to judge the liquidity and solvency position through cash flow analysis, the following measures can be taken into consideration:

(i) The most effective measure is the ratio affixed charges to net cash inflows as suggested by Van Home. This ratio measures the relationship between fixed financial charges and the net cash inflow of a firm, i.e., it reveals that the number of times the fixed financial charges are covered by the net cash flows of a firm. The higher the ratio, the higher amount of debt can be used by the firm.

(ii) The other measure is the preparation of Cash Budge, that is, whether the expected cash flows are quite sufficient to meet the fixed-charge requirements or not. It is prepared to ascertain the possible deviation between the expected cash flows and the actual cash flow of the firm.

The information so received from such budget will help us to know the ability of the firm to pay its fixed-charge obligation through the application of budget which should be prepared for a range of possible cash inflows along with their respective probability.

It is interesting to note that as we know the possible probability of cash flow trend, a firm can easily decide its debt policy to cover fixed charges and work, within the insolvency limit tolerable to management. Donaldson has suggested that a firm can meet its fixed obligation relating to fixed charges (interest on debt capital) together with the principle.

A firm cannot meet the said obligation only during the adverse circumstances and is then considered as the risk of bankruptcy. He termed it recession condition’. The said recession condition can be challenged by preparing a net cash flow for such period and evaluate the result which will no doubt, help to find out the alternative debt policy on the risk of bankruptcy.

Factor # 4. Control:

We know .that the equity shareholders being the owner of the firm can exercise control over the affairs of the firm. They have also the voting right. On the contrary, debenture- holders and preference shareholders do not posses such voting rights except under certain conditions for the preference shareholders only. Practically, lenders have no direct ‘say’ in the management of a company.

Till their interest (i.e., regarding payment of interest and dividend) is not affected legally, they can do a very little against the company as they have no direct control i.e., regarding policy matter or decision making, they have nothing to do.

They do not have any voting rights for the appointment of board of directors as well, other lenders and creditors also, like debenture holders and preference shareholders, do not have any ‘say’ in the management of the company i.e., they cannot actually take part in the management as the entire body is being controlled by the equity holders or the owners of the company.

Thus, if the primary objective of the company is to control efficiently, more weight must be given to debt capital for additional requirement of capital in the total capital structure of a firm as, in that case, management does not have to make any sacrifice regarding the control of the firm.

Needless to say here that if the firm borrows more than its repayment capacity, they (lenders and creditors) may seize the asset of the company against their claims for interest/dividend as well as for principal.

In the circumstances the management loses all control over the affairs of the company. Naturally, it is better on the part of the management to sacrifice a part of their control by issuing additional equity shares rather than taking the risk of losing all control to the outsiders viz. lenders and creditors taking too much debt for the requirements of additional funds.

Thus from the standpoint of control, issuing equity share may be treated as better source of financing in the hand of the company. Yet, it may also be stated that if the firm can maintain its liquidity and solvency position by earning higher profitability ratio, and the existing management prefers to keep control in its own hand, then it may encourage borrowings rather than issuing fresh equity shares as in the case of later there is the possibility of losing control over the company affairs.

Thus, the firm should select an appropriate debt-equity mix after considering its overall profitability

Factor # 5. Timing and Flexibility:

After determining an appropriate capital structure, a firm has to face this problem relating to timing of security issues. For procuring additional funds, a firm has to face the question of appropriate mix of debt and equity and what should be the timing of issuing such securities in order to maintain strict proportion of debt and equity, although it is not an easy task.

At the same time, which one will be issued at first i.e., whether debt at first and equity at last or vice-versa, that also should be decided.

The answer lies in the evaluation of alternative methods of financing according to general state of economy and the firm’s expectation about it. Needless to say, if the existing rate of interest on debt capital is high and there is the possibility of coming down the rate of such interest, the management will go for issuing equity shares now and will postpone debt issue.

On the contrary, if the market for company’s equity issues are depressed but that is chance is near future to improve for the same, naturally, the management must go for debt issues now and will postpone the equity issues. The same may be issued at a later date when there will be a favourable conditions for the company, i.e., the market for company’s equity shares will go up.

It is needless to mention again that if the alternative stated above, is chosen, a certain amount of flexibility must be sacrificed.

When the amount of debt capital will be quite substantial and things take a turn for the worse, the company may be forced to issue equity in future even in an unfavourable terms. In order to preserve its flexibility in tapping the capital markets, it may be better for a firm to issue equity shares now so as to have unused debt capacity for future needs.

If the company’s requirements of funds are unpredictable and sudden, it is better for it to preserve unused debt capacity which, in turn presents the company financial by leaving the option open for it. It is interesting to note that this flexibility could also be attained by maintaining excess liquidity position by avoiding the opportunity cost, if any.

However, for a developing firm, the above criterion has a snag in itself. By issuing stock now so as to have unused debt capacity, the company will properly have to issue more shares than it would if it postponed the stock issue. Consequently, there is more dilution to existing shareholders over time.

The trade-off is between preserving financial flexibility and dilution in earnings per share. If the price of the stock is high, however, and expected to fall, the firm can achieve both the flexibility and minimum dilution by issuing stock now.

Debt financing can be quite substantial for financing equity shares, even though the benefits of good timings are limited for debt financing. Because, the value of a share can vary significantly on the effect of general state of economy and expectations for the firm as well. Thus, it is the duty of the existing management of the company to sell the shares among the existing shareholders at a favourable price.

Similarly, they should consider debt capital also at a favourable rate of interest. Although both the debt and equity financing have substantial role to play is a financing mix, the timing of issuing share is very important aspect which should be given a due consideration.

Factor # 6. Nature and Size of the Firm:

The nature and size of the firm have a significant role while procuring funds from various sources. For example, it is very difficult for a small firm to raise funds from long term sources even if its credit status is good. The same is available for it at a comparatively high rate of interest with inconvenient repayment terms as well.

For this purpose, the management of such firms cannot operate their functions normally due to various interference and as such, their capital structure becomes very inflexible.

That is why, they are to depend 011 their own source of finance for long-term funds viz, equity shares, retained earnings/ ploughing back of profits etc. Moreover, in case of small firms, the cost of issuing equity shares is comparatively high than that of a big firm.

Besides, if equity shares are issued at a frequent interval for procuring long-term funds, there may be a possibility of losing control over the affairs of the company as a whole which may not arise in case of a big firm. But a small firm has a distinct edge over the big one.

That is the shares of a small company are not scattered widely throughout the country and as such the dissident shareholders, if any, can be controlled and organised easily in an efficient manner while the same is not possible in the case of a big company as the shares are widely issued throughout the country. So it is difficult to control them.

Thus, a small firm instead of growing fast by issuing more shares prefers to restrict the business and use their retained earnings as a source of long-term funds. But a big company has got more flexibility while deserving its capital structure. For raising funds for long-term purpose, it can take loan on easy terms which are available, issue debentures and preference shares to the public for such long-term funds.

Moreover, the cost of issuing shares are comparatively low than a small firm. So, what should be the appropriate capital structure, depends on the nature and size of the firm.

Factor # 7. Industry Standard:

Evaluation of capital structure of other similar risk-class firm is absolutely needed when designing the capital structure of a firm and also the industrial position. Because if a firm follows a different capital structure than that of the similar firm in the same industry, it may have to face a lot of problems e.g., investors may not accept.

It is needless to say that lenders and creditors together with the investment analysts evaluate always the firm according to the industry standard.

So, if a firm goes out of the line, it must have to prove its justifiability in the capital market along with other firms who are in the same line. Moreover, there are certain common factors which are to be considered while designing capital structure e.g., general state of economy, nature, type and size of the firm etc.

Besides the above, the nature and size of the firm may have a direct effect on the capital structure composition, for instance, public utility concerns (e.g., electricity) where day-to-day transactions are done primarily on cash basis. As such, those firms may undertake more risks and they may go for more debt as the liquidity and solvency and profitability position will not adversely be affected.

On the contrary, a firm who has to make a heavy investment in fixed assets and having a high operating leverage will naturally prefer less financial risk and design the capital structure in a different manner than the public utility concern.

Moreover, general state of economy affects the composition of debt and equity in the capital structure. It has been stated above that a firm having stable sales and better prospects for development may use more debt capital in its capital structure than those firms who has unstable sales and no prospect for growth. Besides the above, one point should also be considered i .e conditions of capital market.

For example, reputed concerns enjoy certain favourable response from the public whereas new or less known established concerns find some difficulty. In our capital market, the position of preference shares and debentures are not popularly accepted with the exception of convertible debentures due to their conversion facility, i.e., from debentures to equity shares.

These are other long-term institutional loans which are sanctioned after fulfilling certain terms and conditions (e.g. debt equity ratio should be 2: 1). Thus, while desiring capital structure all the above stated factors should carefully be considered.