Amerco does not enter into a hedge of its export sale until it actually makes the sale. Assume now that on December 1, 2009, Amerco receives and accepts an order from a German customer to deliver goods on March 1, 2010, at a price of 1 million euros.

Assume further that under the terms of the sales agreement, Amerco will ship the goods to the German customer on March 1, 2010, and will receive immediate payment on delivery. In other words, Amerco will not allow the German customer time to pay. Although Amerco will not make the sale until March 1, 2010, it has a firm commitment to make the sale and receive 1 million euros in three months. This creates a euro asset exposure to foreign exchange risk as of December 1, 2009. On that date, Amerco wants to hedge against an adverse change in the value of the euro over the next three months. This is known as a hedge of a foreign currency firm commitment.

Although SFAS 133 indicated that only fair value hedge accounting is appropriate for hedges of foreign currency firm commitments, the FASB’s Derivatives Implementation Group subsequently concluded that cash flow hedge accounting also could be used. However, because the results of fair value hedge accounting are intuitively more appealing, we do not cover cash flow hedge accounting for firm commitments.

Under fair value hedge accounting- (1) the gain or loss on the hedging instrument is recognized currently in net income and (2) the gain or loss (that is, the change in fair value) on the firm commitment attributable to the hedged risk is also recognized currently in net income. This accounting treatment requires- (1) measuring the fair value of the firm commitment, (2) recognizing the change in fair value in net income, and (3) reporting the firm commitment on the balance sheet as an asset or liability.

ADVERTISEMENTS:

This raises the conceptual question of how to measure the fair value of the firm commitment. Two possibilities are- (1) through reference to changes in the spot exchange rate or (2) through reference to changes in the forward rate. The examples that follow demonstrate these two approaches.

Forward Contract used as Fair Value Hedge of a Firm Commitment:

To hedge its firm commitment exposure to a decline in the U.S. dollar value of the euro, Amerco decides to enter into a forward contract on December 1, 2009. Assume that on that date, the three-month forward rate for euros is $1.305 and Amerco signs a contract with New Manhattan Bank to deliver 1 million euros in three months in exchange for $1,305,000. No cash changes hands on December 1, 2009.

Amerco elects to measure the fair value of the firm commitment through changes in the forward rate. Because the fair value of the forward contract is also measured using changes in the forward rate, the gains and losses on the firm commitment and forward contract exactly offset.

The fair value of the forward contract and firm commitment are determined as follows:

Amerco pays nothing to enter into the forward contract at December 1, 2009. Both the forward contract and the firm commitment have a fair value of zero on that date. At December 31, 2009, the forward rate for a contract to deliver euros on March 1, 2010, is $ 1.316. A forward contract could be entered into on December 31, 2009, to sell 1 million euros for $1,316,000 on March 1, 2010.

Because Amerco is committed to sell 1 million euros for $1,305,000, the value of the forward contract is $(11,000); present value is $(10,783), a liability. The fair value of the firm commitment is also measured through reference to changes in the forward rate. As a result, the fair value of the firm commitment is equal in amount but of opposite sign to the fair value of the forward contract. At December 31, 2009, the firm commitment is an asset of $10,783.

On March 1, 2010, the forward rate to sell euros on that date is the spot rate, $1.30. At that rate, Amerco could sell 1 million euros for $1,300,000. Because Amerco has a contract to sell euros for $1,305,000, the fair value of the forward contract on March 1, 2010, is $5,000 (an asset). The firm commitment has a value of $(5,000), a liability.

The journal entries to account for the forward contract fair value hedge of a foreign currency firm commitment are as follows:

Consistent with the objective of hedge accounting, the gain on the firm commitment offsets the loss on the forward contract, and the impact on 2009 net income is zero. Amerco reports the forward contract as a liability and reports the firm commitment as an asset on the December 31, 2009, balance sheet. This achieves the FASB’s objective of making sure that derivatives are reported on the balance sheet and ensures that there is no impact on net income.

Once again, the gain on forward contract and the loss on firm commitment offset. As a result of the last entry, the export sale increases 2010 net income by $1,305,000 ($1,300,000 in sales plus a $5,000 adjustment to net income). This exactly equals the amount of cash received. In practice, companies use a variety of account titles for the adjustment to net income that results from closing the firm commitment account.

The net gain on forward contract of $5,000 ($10,783 loss in 2009 plus $15,783 gain in 2010) measures the net benefit to the company from hedging its firm commitment. Without the forward contract, Amerco would have sold the 1 million euros received on March 1, 2010, at the spot rate of $1.30 generating cash flow of $1,300,000. Through the forward contract, Amerco is able to sell the euros for $1,305,000, a net gain of $5,000.

Option used as Fair Value Hedge of Firm Commitment:

ADVERTISEMENTS:

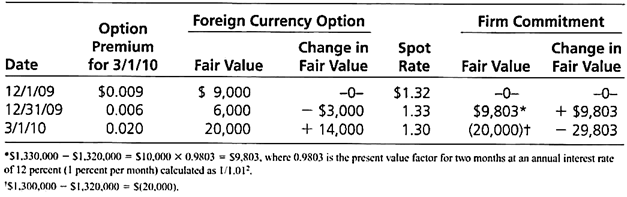

Now assume that to hedge its exposure to a decline in the U.S. dollar value of the euro, Amerco purchases a put option to sell 1 million euros on March 1, 2010, at a strike price of $1.32. The premium for such an option on December 1, 2009, is $0,009 per euro. With this option, Amerco is guaranteed a minimum cash flow from the export sale of $1,311,000 ($1,320,000 from option exercise less $9,000 cost of the option).

Amerco elects to measure the fair value of the firm commitment by referring to changes in the U.S. dollar-euro spot rate. In this case, Amerco must discount the fair value of the firm commitment to its present value.

The fair value and changes in fair value for the firm commitment and foreign currency option are summarized here:

At December 1, 2009, given the spot rate of $1.32, the firm commitment to receive 1 million euros in three months would generate a cash flow of $1,320,000. At December 31, 2009, the cash flow that the firm commitment could generate increases by $10,000 to $1,330,000. The fair value of the firm commitment at December 31, 2009, is the present value of $10,000 discounted at 1 percent per month for two months. Amerco determines the fair value of the firm commitment on March 1, 2010, by referring to the change in the spot rate from December 1, 2009, to March 1, 2010. Because the spot rate declines by $0.02 over that period, the firm commitment to receive 1 million euros has a fair value of $(20,000) on March 1, 2010.

ADVERTISEMENTS:

The journal entries to account for the foreign currency option and related foreign currency firm commitment are discussed next:

There is no entry to record the sales agreement because it is an executory contract. Amerco prepares a memorandum to designate the option as a hedge of the risk of changes in the fair value of the firm commitment resulting from changes in the spot exchange rate.

The net increase in net income over the two accounting periods is $1,311,000 ($6,803 in 2009 plus $1,304,197 in 2010), which exactly equals the net cash flow realized on the export sale ($1,320,000 from exercising the option less $9,000 to purchase the option). The net gain on the option of $11,000 (loss of $3,000 in 2009 plus gain of $14,000 in 2010) reflects the net benefit from having entered into the hedge. Without the option, Amerco would have sold the 1 million euros received on March 1, 2010, at the spot rate of $1.30 for $1,300,000.